COcheesehead

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Vanguard Settlement Fund, VMFXX, is at 5.22%

FZDXX now up to 5.15%

Vanguard Settlement Fund, VMFXX, is at 5.22%

I've ran into the same thing. I'm discovering that my credit unions seem to have zero interest in retaining my IRA business. They're offering great Promo CD rates at 5.25% but rate does not apply to IRA CD's. The highest IRA CD rate was less than 1% recently at Frontwave and when I complained about it she offered to have someone contact me who she was sure to get me a better rate and next thing I got an e-mail from their wealth management department. This has happened to me at 2 different credit unions now, so I've been moving my IRA's to Fidelity as they mature.

^^^^^

Looks like we have a rate war going on between the brokers... SWVXX was just bumped to 5.16 this morning, up from 5.12 yesterday.

I've ran into the same thing. I'm discovering that my credit unions seem to have zero interest in retaining my IRA business. They're offering great Promo CD rates at 5.25% but rate does not apply to IRA CD's. The highest IRA CD rate was less than 1% recently at Frontwave and when I complained about it she offered to have someone contact me who she was sure to get me a better rate and next thing I got an e-mail from their wealth management department. This has happened to me at 2 different credit unions now, so I've been moving my IRA's to Fidelity as they mature.

Me too, but it's is making me park more of my maturing CD money there. But I'm ready to re-buy CD's again in a days notice. Still have more invested in CD's than I do in MM as I wait and watch this unfold.Not sure of the value, if there is a war. I am not moving money based on ultra short term yields. Just happy that my short term funds are now making something.

Looks like we have a rate war going on between the brokers... SWVXX was just bumped to 5.16 this morning, up from 5.12 yesterday.

Not sure of the value, if there is a war. I am not moving money based on ultra short term yields. Just happy that my short term funds are now making something.

I read that rates are rising but have not seen much to buy. Yet.

I read that rates are rising but have not seen much to buy. Yet.

Saw that. But the professional traders were already massively short the 10y-most since 2018 when Fed last raised. The shorts were wrong then.Ackman is supposedly shorting the 10yr. Maybe he is right, maybe not.

Ackman is supposedly shorting the 10yr. Maybe he is right, maybe not.

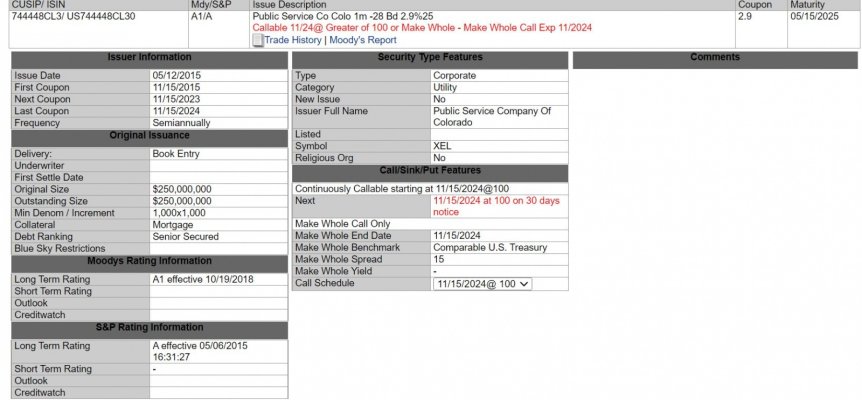

Here's another that I like (with ratings). Always use it before I buy a brokered CD. One of the forum members posted it here a "good while back" and I've found it very useful.Here is a handy link to lookup FDIC insured banks... In the first box on the left, change it to "Bank Name" and in the box below, start typing in the name of the bank. Pick your choice and click "Search".

https://banks.data.fdic.gov/bankfind-suite/bankfind

Then both 10 and 30 yr are being shorted.

Moody's bank downgrade announcement seem to have pushed rates back down. If the CPI is benign as some expect we may not be going much higher anytime soon.

A fed governor announced he thinks we may be done on rate hikes.

It just points up the importance of using mini-swoons to fill out your bond inventory.

Probably will see yields top out this month.

I don't think the Fed will raise rates again in fear of overshooting.

So have we seen the top in yields?

I agree that as headwinds clear on recession/economy fears and that may not be until late next year, we could see the long end tip up and the short end drop down - the normalizing of the curve. The issue is does the long end return to were it was say just last Fall or blow through that?There is an interesting analysis by Bob Carlson in his newsletter that suggests longer term rates will continue to rise. The main reason is that Treasury needs to rebalance their debt - they like to keep a balance between short and long term debt, but have shifted heavily to short term over the past years. They also need to issue a ton more debt to fund spending. At the same time both banks and the Fed have stopped buying additional Treasuries.

So supply of longer-term treasuries is going up and demand going down. The Treasury markets will need to raise rates (cut prices) to balance supply and demand.

Sounds logical, but predicting markets is hard.