Selling low, locking in losses when bond funds will be returning healthy dividends for years to come?

Absolutely not.

Selling low, locking in losses when bond funds will be returning healthy dividends for years to come?

Absolutely not.

This all so confusing when considering which way to go.

Selling low, locking in losses when bond funds will be returning healthy dividends for years to come?

Absolutely not.

One thing to be careful about is free advice from anonymous strangers.This all so confusing when considering which way to go.

Good luck with that strategy.Selling low, locking in losses when bond funds will be returning healthy dividends for years to come?

Absolutely not.

You never know except in hindsight but the market appears to be telling us it sees the top in yields.

Hopefully folks have been extending duration for quite some time now.

Right now it looks like a garden variety correction in an ongoing bond bear market. Just last month the 30-year yield dropped 37 basis points in just 4 days before turning around. The past 2 days have seen a drop of 29 basis points. The velocity of the upmove the past 2 days looks like massive short covering by professionals. (Yes, professionals short bonds and bond futures). We'll know better in 8-10 days. I have no idea whether yields have peaked or not. All I know is the current intermediate and long-trend in rates is still up. If the 30 year treasury bond yield breaks 4.68%, I'll have to reconsider.You never know except in hindsight but the market appears to be telling us it sees the top in yields.

Hopefully folks have been extending duration for quite some time now.

As I said, we never know except in hindsight.Right now it looks like a garden variety correction in an ongoing bond bear market. Just last month the 30-year yield dropped 37 basis points in just 4 days before turning around. The past 2 days have seen a drop of 29 basis points. The velocity of the upmove the past 2 days looks like massive short covering by professionals. (Yes, professionals short bonds and bond futures). We'll know better in 8-10 days. I have no idea whether yields have peaked or not. All I know is the current intermediate and long-trend in rates is still up. If the 30 year treasury bond yield breaks 4.68%, I'll have to reconsider.

Wild stuff yesterday and perhaps today too. I own some long duration, high coupon, non callable corporates RBC, HSBC, Wells Fargo and they are all up selling well over par. They had stock market like returns yesterday 3%-4% single day returns. I even had some long duration munis up 1%-2%.

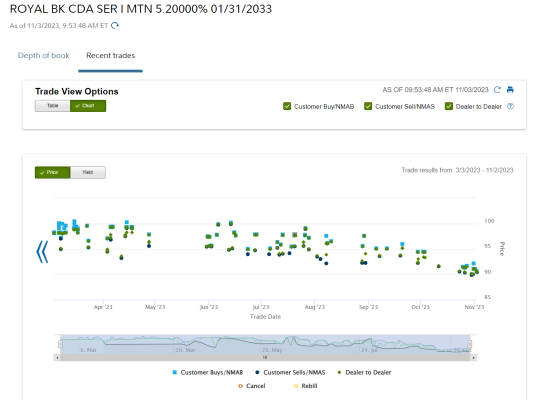

"well over par" is only true if they are recent purchases. For example, here's the RBC 5.2% of 2033 that many here bought as a new issue a while back (after rates had run up). Yes, it has improved over the last few days, but still at 90.6 bid. I'm only using this as an example, the "peak" will only be known in the rear view mirror, and we best be looking forward down the road for the next hill.

You never know except in hindsight but the market appears to be telling us it sees the top in yields.

Hopefully folks have been extending duration for quite some time now.

The market thought the top was in June 22, then top in October 22, top in February 23 and now top in October 23.

Eventually it will be right. If the CPI & PCE come in at or below expectations in the next 3 months I may start believing that was the top. Definitely not until then.

If you use Fidelity, a combination of their fixed income analysis report and the portfolio dividend view would give you all the visibility you’d need.

Tried this, but there are so many issues. I can't get the bond fund ETF's to add, even though it says it supports them. It doesn't take baby bonds. It takes forever to calculate. It doesn't show the ladder by year. It's really not useful for me.

You need to use the Fixed income analysis for individual issues then add in the “dividend view” from your portfolio summary page (it’s a check box at the top of the page) which shows income from ETFs and funds. I use the two to get a complete picture. I find it very useful.

The fixed income analysis shows ladders by year so I am not sure what you are experiencing.

The market is thin in taxable munis. I own a few, but bought them to hold to maturity. You can always ask Fidelity to bid them for you and just see what prices comes back. Then make a decision. If liquidity is important, Treasuries and corporate bonds trade all day long. If you buy in the secondary with an existing bid, there will likely also be a bid when it comes time to sell.Thanks, I see that now. But I still have iBonds (US Govt), baby bonds and other securities that the tool can't handle. Also, since I have investments stretched across multiple brokerages it's just tough to use it. I'm on spreadsheets which works okay, but not great. I wish I had a nice third party spreadsheet tool that was sophisticated enough to handle TIPS, baby bonds, US Govt iBonds, etc.

On another topic, I'm rebalancing my ladder to extend duration more, and would like to trade out some CD's for taxable muni's, but I'm uncomfortable buying individual issues because of the challenge if I had to sell them later. Plus with no bid/ask spread, I don't like the guesswork of setting the buy price. There is only one taxable muni bond ETF, but it isn't a term fund, like the iShares iBonds. Any other angle I'm missing on taxable muni's?