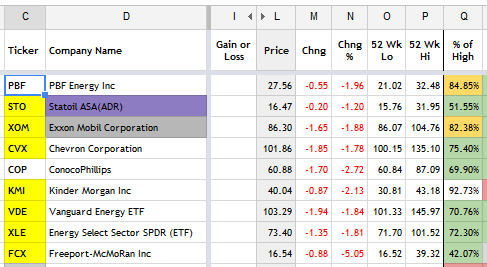

BHP Hilton at a glance:

Go BHP

Go BHP

I'm down a bit (about 7k) but boy was it fun buying low in the last 3 months. I'm a small fish in much larger frying pan.

We shall see what we shall see.

Well BHP is the poster child and a small study of what has occurred worldwide.

It is heavily in the commodities that have been in oversupply, and one of the major players in creating the oversupply. In 2008 it had 8 billion in debt and has borrowed another 22 billion to get to 30 million in long term debt at advantageous rate of 4 percent due to worldwide interest policies.

in 2011 on 72 billion in sales it had 5 billion in annual depreciation costs now with 71 billion in sales and falling it has 9 billion in depreciation.

It has another 12 billion in commitments for another 8 projects it has undertook, main attraction appears to be proposed split of their minerals division from the commodity oil and gas properties. Which will increase total debt to about 40-45 billion dollars, (currently with short term debt BHP's total debt is 35 billion dollars. While it is not costly in low interest rate environments to only pay 1.5 billion in interest on such a large sum of debt, this company has positioned itself for long term bull market in commodities in a time when commodity prices are in a major bear market, yet this stock is only off from 100 when the strategy appeared to be a very smart move.

From it's most recent presentation on 6 month performance review of July - Dec 2015:

Group production increased by 9% during the December 2014 half year with records achieved for eight operations and five commodities. Production guidance remains unchanged and we are on track to deliver Group production growth of 16% over the two years to the end of the 2015 financial year.

Metallurgical coal production increased by 21% to 26 Mt in the December 2014 half year as Queensland Coal and Illawarra Coal both achieved record half year volumes.

Western Australia Iron Ore production increased by 15% to a record of 124 Mt (100% basis) in the December 2014 half year as the ramp-up of Jimblebar continued and we improved the availability, utilisation and rate of our integrated supply chain.

Petroleum production increased by 9% to a record 131 MMboe in the December 2014 half year supported by a 71% increase in Onshore US liquids volumes to 24.4 MMboe.

Copper production(1) decreased by 2% to 813 kt as strong underlying operating performance across the business was offset by lower grades at Antamina.

Record manganese ore and alumina production was underpinned by strong performances at both Hotazel and the Alumar refinery.

From it's review you can see the 131 million barrels of oil realized an average sale price of 85 dollars per barrel, meaning the price decline of oil has not yet hit BHP. However taking that 131 million of production doubled for yearly production, if it sells for $45 per barrel you have a decrease of 11 billion dollars of sales forthcoming in 2015 just from oil (15 per cent of sales), with all of these dollars falling from the bottom line, meaning at 45 dollar oil BHP as a company is not profitable. I do not think this is reflected in the current stock price as investors instead are focused on the 85 realized and the dividends paid from that as opposed to the future with 45 dollar oil.

If you then layer in copper average of $3.00 per lb realized in 4th qtr now at $2.45 I do not see how this company can withstand current prices and maintain it's current stock price. Already they are announcing they are taking 200 million in provisional pricing for copper in the 4th qtr, a 350 million charge for failure of planned asset sale to go through of their Nickel West business and a write down of those assets, a 850 million tax charge for loss of a deferred tax asset in Australia, a 250 million charge for petroleum producing assets in Louisiana and announced while it plans to go forward with it's tar sand oil project it will review to optimize cash flow.

And this is before even discussing their plan to increase Iron Ore production by 30 percent in 2015 even while iron ore prices have dropped even more than oil.

I think this company is a very good proxy for the overall world process in oil and commodities and will be a leading indicator in 2015 of effects of large amounts of low interest debt tied to high production of natural resources.