- Joined

- Nov 17, 2015

- Messages

- 14,152

I think the "they rebuilt on a bad risk to begin with" is a small number of the problem claims. They do make the rounds though.

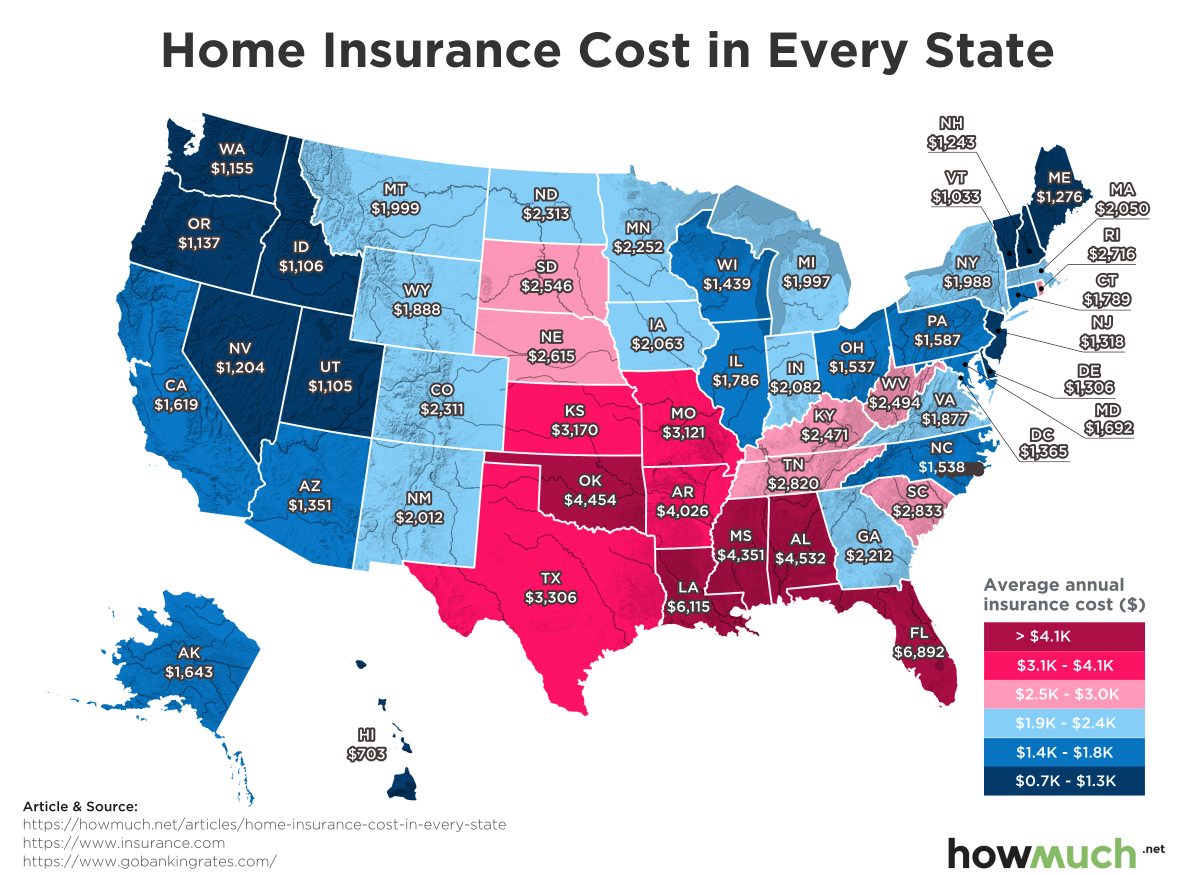

What do you do with 22M+ people in Florida? Ok, not all of them are homeowners, but still you're talking millions of policies at present.

The whole state is a hurricane risk. Sure, no storm surge worries further inland, but over half of us live within 20 miles of the coast. And many of us haven't been hit despite the spaghetti models that said we coulda shoulda every few years. And I would bet the insurance companies absolutely do not care if your cozy little florida town hasn't actually had a event in 20+ years, past performance, future results...etc.

Hurricanes can and do go cut across the state or go all the way up. Any roof in that cone is at risk. Now, in most cases, most homes won't be destroyed. But many in the eye path will have $30k-$100k damage claims (not counting flooding). I consider us lucky with no claim since 2005 (Wilma took enough of our roofing off to expose wood, and tore away our screen/cage).

If everyone in Florida woke up on Jan1 without insurance, or with annual policies over $10k, it would be absolute chaos here.

What do you do with 22M+ people in Florida? Ok, not all of them are homeowners, but still you're talking millions of policies at present.

The whole state is a hurricane risk. Sure, no storm surge worries further inland, but over half of us live within 20 miles of the coast. And many of us haven't been hit despite the spaghetti models that said we coulda shoulda every few years. And I would bet the insurance companies absolutely do not care if your cozy little florida town hasn't actually had a event in 20+ years, past performance, future results...etc.

Hurricanes can and do go cut across the state or go all the way up. Any roof in that cone is at risk. Now, in most cases, most homes won't be destroyed. But many in the eye path will have $30k-$100k damage claims (not counting flooding). I consider us lucky with no claim since 2005 (Wilma took enough of our roofing off to expose wood, and tore away our screen/cage).

If everyone in Florida woke up on Jan1 without insurance, or with annual policies over $10k, it would be absolute chaos here.