I just dont see people giving up a 3 percent mortgage for a 7 plus. I was told by a realtor in Las Vegas that around 35 to 40 percent of homes are owned free and clear. The rest have sub 4 percent mortgages.

There are a lot of reasons people sell and buy. Some people really have no choice as they have to move due to work. When we thought we might move to Las Vegas we visited in the summer of 2022. We went to some open houses in the Providence area. At least a couple of them were Air Force people who obviously had been sent somewhere else. So, they needed to sell. Even non-military folk often have to move due to work. Also, houses often sell when their are divorces. Sometimes people really need a larger house or they want to downsize.

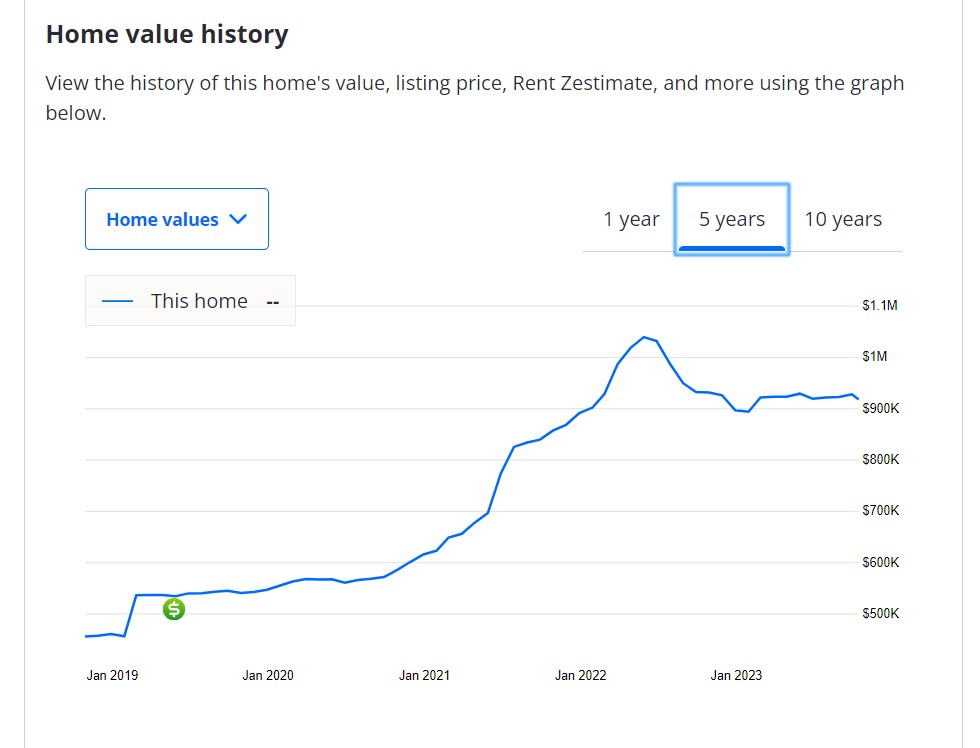

We recently bought a house in Maryland. We gave up a 3.5% mortgage and now have one that is under 7% but not by a huge amount. Of course, I don't like that my mortgage payment went up. It costs me an extra $7600 a year.

But we are still better off financially!

In Texas, our real estate taxes (with the over 65 exemption which froze our school taxes) were about $6700 a year.

In Delaware the taxes on the house we just bought (2000 SF v. 2400 SF in Texas) are about $2200.

In Texas my homeowner's insurance was $6840 (never having had a claim). In Delaware my homeowner's insurance is $1171.

In Texas my HOA was $600 a year. In Delaware my civic association is $25 a year.

Just on those things I am saving about $10740 a year.

So the net is that the saving on taxes and insurance for the house are $10740 a year and the extra mortgage payments are $7600 a year so I still save $3140 a year even with the high mortgage rate.

And, really it is better than that. Delaware has no sales tax. (It has an income tax but since Social Security is not taxed our income taxes will be either nothing or a few hundred dollars.).

This house also doesn't have a pool so I won't have pool maintenance costs. There are a number of areas where the upkeep on this house are less.

The point is that in deciding whether to take a higher mortgage rate you have to look at the totality of the circumstances. In Delaware virtually every house was getting multiple offers.

)

)