MichealKnight

Full time employment: Posting here.

- Joined

- May 2, 2019

- Messages

- 520

I have posted here in the past as my Early Retirement seemed on the way - part my choice, part - my relatively successful business career sort of telling me to eat poop for the past few years....and I am now Early Retired. (I'm 45). I plan to write more later but for now...

I never ever believed in, nor "invested" in the stock market. I felt it was funny-money, and every 8-10 years, certain entities who control it come, take their money, and the masses shake their head, brag to each other about "I took a tax loss!" and "I dollar cost averaged!" - -it just never clicked with me - and most of my adult life I was making more money than I ever deserved quite frankly.

But now I look back - jeepers - had I invested ....I'd be way ahead right now so being early-Retired, I am about 45% in stocks.......long term template is probably between 50-60% depending on events and my mood") Anyhow... as I keep penciling and planning .....I read about that "lost decade" of 1999-2009. Geez...I couldn't take 10 years of -2%.

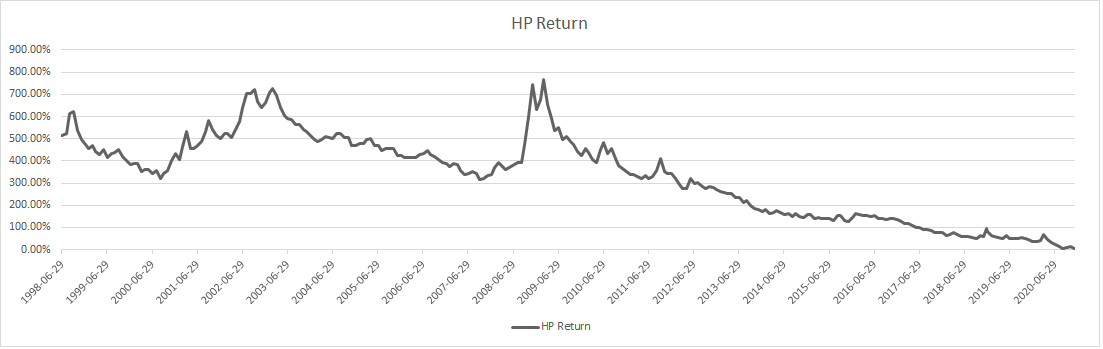

Anyhow... as I keep penciling and planning .....I read about that "lost decade" of 1999-2009. Geez...I couldn't take 10 years of -2%.

I looked up year-by-year VWINX (Wellsley) performance for that time period.

I'm showing an annualized......+6.7% annualized return over that decade.

The flippant me feels like saying "if 6.7% is a lost decade, please---lose as many decades as you can sir"

(I need 4.8% annualized nominal to make it. If I get 5.75-6 then it's just sublime)

But the cautious me says it can't be that easy.

Still - -a fund that isn't "timid" but is hardly too aggressive did 6.7% in the lost decade.

I guess I'm asking opinions...... just how "lost" was that decade because to me....6.7% I'd kiss anyone's ring to get annually.

Thanks

I never ever believed in, nor "invested" in the stock market. I felt it was funny-money, and every 8-10 years, certain entities who control it come, take their money, and the masses shake their head, brag to each other about "I took a tax loss!" and "I dollar cost averaged!" - -it just never clicked with me - and most of my adult life I was making more money than I ever deserved quite frankly.

But now I look back - jeepers - had I invested ....I'd be way ahead right now so being early-Retired, I am about 45% in stocks.......long term template is probably between 50-60% depending on events and my mood

Anyhow... as I keep penciling and planning .....I read about that "lost decade" of 1999-2009. Geez...I couldn't take 10 years of -2%. I looked up year-by-year VWINX (Wellsley) performance for that time period.

I'm showing an annualized......+6.7% annualized return over that decade.

The flippant me feels like saying "if 6.7% is a lost decade, please---lose as many decades as you can sir"

(I need 4.8% annualized nominal to make it. If I get 5.75-6 then it's just sublime)

But the cautious me says it can't be that easy.

Still - -a fund that isn't "timid" but is hardly too aggressive did 6.7% in the lost decade.

I guess I'm asking opinions...... just how "lost" was that decade because to me....6.7% I'd kiss anyone's ring to get annually.

Thanks