atmsmshr

Full time employment: Posting here.

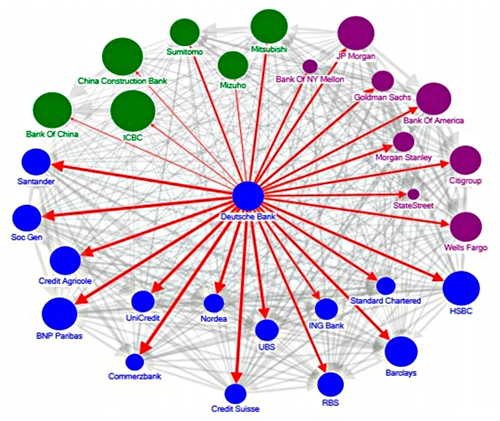

I somewhat understand the stock market, barely grasp the bond market, and remain flummoxed by Banking reserves, overnight lending, repos, and intrabank lending.

US bank liquidity was short this week and overnight repo rates hit 10% last Tuesday. As a result, the Fed bought up abut $50 billion in Treasuries and securitized mortgages so get FMOC rates back in the 2+% range, every day this week since Tuesday!

https://www.cnn.com/2019/09/17/business/overnight-lending-rate-spike-ny-fed/index.html

Any problem with banking liquidity reminds me of Lehman and Bear Stearns, especially when the Fed immediately has to respond with 'putting money in the window' and stating publicly 'keep moving along there no problems here'.

I try to tune out the noise, and don't plan on any portfolio changes since we had already built a SORR bond tent portfolio just prior to retirement this summer. However, credit liquidity concerns me for the health of the economy.

Does anyone care to share insights on what the overnight interbank lending liquidity issue this week means?

US bank liquidity was short this week and overnight repo rates hit 10% last Tuesday. As a result, the Fed bought up abut $50 billion in Treasuries and securitized mortgages so get FMOC rates back in the 2+% range, every day this week since Tuesday!

https://www.cnn.com/2019/09/17/business/overnight-lending-rate-spike-ny-fed/index.html

Any problem with banking liquidity reminds me of Lehman and Bear Stearns, especially when the Fed immediately has to respond with 'putting money in the window' and stating publicly 'keep moving along there no problems here'.

I try to tune out the noise, and don't plan on any portfolio changes since we had already built a SORR bond tent portfolio just prior to retirement this summer. However, credit liquidity concerns me for the health of the economy.

Does anyone care to share insights on what the overnight interbank lending liquidity issue this week means?

Last edited: