Danmar

Thinks s/he gets paid by the post

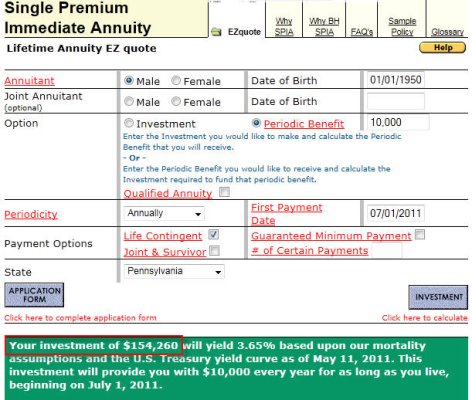

Using actuarial life expectancy and current long term rates, I get a multiplier of about 17. I am surprised Bogle would use such a low multiplier?

"Groupthink" is boringI'm perpetually amazed by this board's ability to disagree on a common definition of any financial concept. It makes GAAP look easy...

...

...Danmar said:Delaware. Thanks. My calcs did not include profit for the insurance co. My x employer is a AAA rated bank so default risk low. If the objective of the valuation exercise is asset allocation or ego stroking no reason to be conservative?

I think the primary objective is to be realistic and accurate as possible though.

Otherwise why not just use a 100x multiplier?

Folks have different opinions (this question came up in the past).This thread raises an interesting conceptual question. If I write a check for $x to an insurance company for a SPIA, have my assets gone down by $x?

OK, thanks.

As for the other 40+ posts, I'm perpetually amazed by this board's ability to disagree on a common definition of any financial concept. It makes GAAP look easy...

Honestly I don't know of any practical application to knowing the net worth of my pension. It's not as if I can borrow against it, or get an advance on it.

I just like to know stuff.

Amethyst

I take the value of my pension to be the replacement cost of buying an annuity with the same attributes as my db pension. This replacement cost varies with the prevailing interest rates and actuarial estimates of lifespan. I also compare this to the cash value that my former employer is willing to give me for the pension.

I take the lower of the two values and include this in my net worth in order to determine my equity/bond/cash mix. I assume the DB plan value is bonds, then I review the total mix and adjust where appropriate.

"Groupthink" is boring

YouTube - Rough cowboys herding cats in the prairieI disagree.

).

This thread raises an interesting conceptual question. If I write a check for $x to an insurance company for a SPIA, have my assets gone down by $x?

In my opinion, the answer to this question is "no".

I don't get why you would've hit a big bump if you had considered it an asset rather than an income stream. If you make the right assumptions and do the math right, it's the same money no matter which way you figure it. Your problem would've been underestimating expenses, not how you accounted for the money. If you had enough with an income stream + other assets, why wouldn't you have enough with the pension "asset" + other assets?I've always viewed a pension as an income stream that I can use to cover real COL expenses.

If a pension is COLAd, great, but there is no guarantee that the annual COLA amount will be non-zero nor that a greater than zero COLA will completely cover current increases in COL expenses.

I am currently receiving a COLAd pension, which has had 2 years of zero COLA. My real COL expenses for the past 2 years are exceeding what I thought would be covered by a non-zero COLA. This is reality (not a complaint so no rotten tomatoes, please

If I had assumed that this pension (times some multipler or as a large principal) was an asset to be added into my net worth, I would have hit a big bump in the road. My other assets (bond fund dividends and cash savings) serve as the backup mechanisms to supplement my pension income for the long haul.

It is a slightly different way of thinking, but it w*rks for me.

Sorry if I wasn't clear...I don't get why you would've hit a big bump if you had considered it an asset rather than an income stream. If you make the right assumptions and do the math right, it's the same money no matter which way you figure it. Your problem would've been underestimating expenses, not how you accounted for the money. If you had enough with an income stream + other assets, why wouldn't you have enough with the pension "asset" + other assets?

Income is not included in a net worth calculation. It is included when you calculate the amount of money you will need in retirement.

Rustic23 said:So if I win a 160 million dollar lottery that pays out over 25 years I don't count the discounted amount of those payments as part of my net worth? I think most people would.