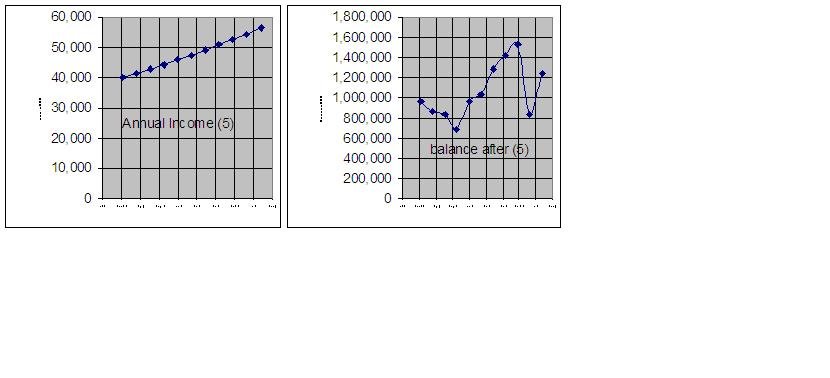

I recently hit my savings goal which was to save enough to support a 3% withdrawal rate at my current budget. Woo Hoo! I will likely continue working for a while because I don't hate it and I'm being well paid.

But, I'm thinking through my plans so that I have the comfort of knowing that I can walk away at any time if I want. I am nearly 47 and my spouse is nearly 45. So, we need to make this money last for 50+ years. We are invested 50/50 stocks/bonds.

Given the 4% "rule," my thinking is that a 3% withdrawal rate is pretty conservative. But, to add a level of conservatism, we are happy with our budget based on the 3% withdrawal rate. As a result, even if the portfolio jumped dramatically, we would probably stick fairly close to our initial budget plus inflation. On the other side of the fence, my math tells me that if the stock market falls 50% sticking with our current budget would have us withdrawing at a 4% rate. And, knowing my spouse and myself, I have no doubt that we'd decrease spending a bit if we suffered a 50% stock loss. Our 3% based budget is generous enough that we could cut a bit without too much pain (keep our cars for another year or two, take one less vacation, etc.). So, the plan would be to start with 3%, go with 3% plus inflation in years with increases and go up to 4% in years with decreases (recognizing that we'd probably cut spending in years with big losses).

My primary question is whether there is a way to analyze this plan using the current withdrawal calculators? I tried with Firecalc, but couldn't figure out how to input exactly what I'm suggesting.

My other question is whether this seems conservative, aggressive or something in between. All thoughts welcome.

But, I'm thinking through my plans so that I have the comfort of knowing that I can walk away at any time if I want. I am nearly 47 and my spouse is nearly 45. So, we need to make this money last for 50+ years. We are invested 50/50 stocks/bonds.

Given the 4% "rule," my thinking is that a 3% withdrawal rate is pretty conservative. But, to add a level of conservatism, we are happy with our budget based on the 3% withdrawal rate. As a result, even if the portfolio jumped dramatically, we would probably stick fairly close to our initial budget plus inflation. On the other side of the fence, my math tells me that if the stock market falls 50% sticking with our current budget would have us withdrawing at a 4% rate. And, knowing my spouse and myself, I have no doubt that we'd decrease spending a bit if we suffered a 50% stock loss. Our 3% based budget is generous enough that we could cut a bit without too much pain (keep our cars for another year or two, take one less vacation, etc.). So, the plan would be to start with 3%, go with 3% plus inflation in years with increases and go up to 4% in years with decreases (recognizing that we'd probably cut spending in years with big losses).

My primary question is whether there is a way to analyze this plan using the current withdrawal calculators? I tried with Firecalc, but couldn't figure out how to input exactly what I'm suggesting.

My other question is whether this seems conservative, aggressive or something in between. All thoughts welcome.

")