Certainly comes as no surprise, but the answers to this credit score question just confirm that most of us regulars here tend to be financially prudent in the way we lead our life when it comes to finances. And it doesn't matter whether you're rich or poor, just wise in your decisions.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

The White Whales - Perfect Credit Scores?

- Thread starter HI Bill

- Start date

jazz4cash

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Unfortunately, the credit scores 'measure' how well you utilize credit. Having a lot of available credit helps the score, as does low utilization (<30% of credit limit per account, every month). The reason I make interim CC payments is to keep my utilization low for my primary cards. They also value a variety of credit classes (mortgage, installment loan, credit card, etc.). It used to drive me crazy that my mom, who was terrible with credit cards (racking up debt and not paying it off in full monthly) had a better credit score than I did. The travesties of the rating systems, IMHO, are that they don't consider payments in full for CCs, just the month-end balances for utilization calculations, and they don't consider one's assets. I laughed when I asked for an increase on one card when I was going on vacation, and they said that they thought I had the correct amount of credit based on my income and credit score.

Yeah, really it’s a scam. An arbitrary made up ‘formula’ to monetize the huge pile of data collected by the credit bureaus. My ability to repay a loan is greatly influenced by my income, my assets, and my payment history (including utilization, etc.). A credit score formula does not take my income or assets into account. If I can “boost” my score as one of the bureaus is promoting, does that mean I am instantly more worthy of a loan?

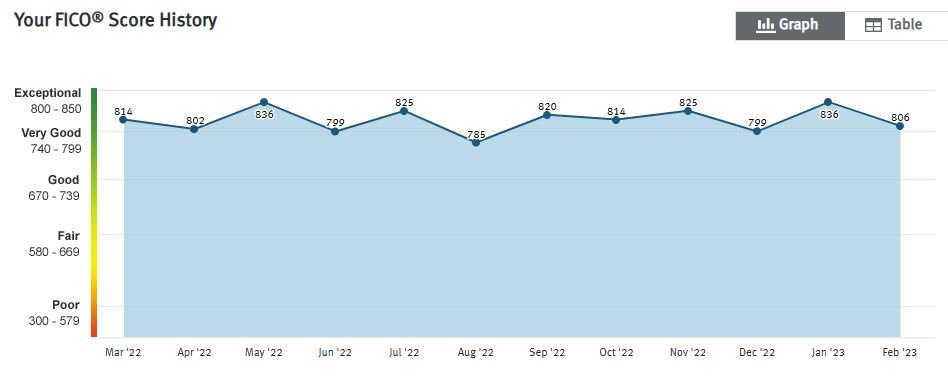

My score had been near or at 850 as reported on my credit card site.

It dropped to 802, after several months it's up to 828

I have one mortgage loan, but the bank moved the loan service to a 3rd party, Than I did a REFI, than the bank got bought by another bank and it's a new name and new account numbers. All in a couple months.

I think it looks like too much loan activity to the credit agencies, I got one loan but the credit report shows the old loan closed, 2 recent short duration closed loans that my debt passed through and the new mortgage loan

It dropped to 802, after several months it's up to 828

I have one mortgage loan, but the bank moved the loan service to a 3rd party, Than I did a REFI, than the bank got bought by another bank and it's a new name and new account numbers. All in a couple months.

I think it looks like too much loan activity to the credit agencies, I got one loan but the credit report shows the old loan closed, 2 recent short duration closed loans that my debt passed through and the new mortgage loan

Last edited:

Lewis Clark

Thinks s/he gets paid by the post

- Joined

- Aug 2, 2018

- Messages

- 1,033

Credit scores are, and have to be, based only on the information available in our credit reports. They have no idea what our assets are, nor should they.

One friend of mine was angry because he did not have a perfect credit score even though he owned assets worth many millions of dollars. But he paid a couple of small bills late because he misplaced them, not because he didn't have the money or didn't want to pay what he owed. His credit score, though still high, was reduced accordingly.

To me, there is a difference between "perfect credit" and a "perfect credit score". Perfect credit is for those folks who pay every bill on time. Perfect credit score is for those folks who earn the maximum evaluation on some arbitrary formula that hurts people who pay bills on time but don't behave in ways that are rewarded by the credit score formulas. Just one of the many problems with the credit reporting system.

Another problem is the difficulty of fixing errors made by the credit reporting agencies. If they want the credit scores they calculate to accurately reflect the credit worthiness of consumers, they should be more interested in fixing their own mistakes.

One friend of mine was angry because he did not have a perfect credit score even though he owned assets worth many millions of dollars. But he paid a couple of small bills late because he misplaced them, not because he didn't have the money or didn't want to pay what he owed. His credit score, though still high, was reduced accordingly.

To me, there is a difference between "perfect credit" and a "perfect credit score". Perfect credit is for those folks who pay every bill on time. Perfect credit score is for those folks who earn the maximum evaluation on some arbitrary formula that hurts people who pay bills on time but don't behave in ways that are rewarded by the credit score formulas. Just one of the many problems with the credit reporting system.

Another problem is the difficulty of fixing errors made by the credit reporting agencies. If they want the credit scores they calculate to accurately reflect the credit worthiness of consumers, they should be more interested in fixing their own mistakes.

Newventurer

Recycles dryer sheets

“Have you achieved a perfect score? I have no real reason to do this, other than striving for the unobtainable goal!”

And then…

“Balance in everything.”

And then…

“Balance in everything.”

target2019

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

You have upside!Well I must be the delinquent in the group. Mine is only 794.

No mortgage for 17 years, no car loans in a long time, no installment loans and card automatically paid each month on the due date.

Not sure why I'm not over 800 but I don't think it matters.

Hah. Yes. Wouldn't want to be at 850 and have nowhere to go but down.You have upside!

TheWizard

Thinks s/he gets paid by the post

.... But he paid a couple of small bills late because he misplaced them, not because he didn't have the money or didn't want to pay what he owed. His credit score, though still high, was reduced accordingly...

People who are disorganized for whatever reason and don't manage their financial affairs properly rightfully have lower credit scores.

You are correct...

Lewis Clark

Thinks s/he gets paid by the post

- Joined

- Aug 2, 2018

- Messages

- 1,033

People who are disorganized for whatever reason and don't manage their financial affairs properly rightfully have lower credit scores.

I agree completely.

retire48in2018

Recycles dryer sheets

- Joined

- Mar 12, 2008

- Messages

- 368

I am an oddball here.

I have no credit score. No debts or any monitored credit agency type account for many, many years.

The impact for us is some rental car companies won’t do business with us - but we know those that do and are prepared accordingly. Also, when we look at changing insurance companies - we can’t do it online with the automatic online tool - we use a broker.

We have special debit account cards and accounts to use with online purchases as a security measure against fraud.

I have no credit score. No debts or any monitored credit agency type account for many, many years.

The impact for us is some rental car companies won’t do business with us - but we know those that do and are prepared accordingly. Also, when we look at changing insurance companies - we can’t do it online with the automatic online tool - we use a broker.

We have special debit account cards and accounts to use with online purchases as a security measure against fraud.

TheWizard

Thinks s/he gets paid by the post

I am an oddball here.

I have no credit score. No debts or any monitored credit agency type account for many, many years.

The impact for us is some rental car companies won’t do business with us - but we know those that do and are prepared accordingly. Also, when we look at changing insurance companies - we can’t do it online with the automatic online tool - we use a broker.

We have special debit account cards and accounts to use with online purchases as a security measure against fraud.

And all this because what? Credit Cards are evil?

- Joined

- Apr 14, 2006

- Messages

- 23,152

Yes. Also orange peeps at Halloween and talking during David Gilmour's "Comfortably Numb" guitar solo.And all this because what? Credit Cards are evil?

scrabbler1

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Nov 20, 2009

- Messages

- 6,705

Mine is currently 822 according to credit karma.

I pay off my credit cards every month and have a mortgage.

Got a nasty gram from Citi Bank saying if I didn’t use my card they would cancel it. I got the card for a specific reason and haven’t used it since. I needed to pay a bill that was automatically billed to my other credit card so I was going to use the Citi bank card to make them happy. Except the card I have is expired. I must have shredded the new card that they sent. [emoji23]

My current back-up card used to be my primary card until I switched to a cashback card nearly 10 years ago. But, to keep my current back-up card active all these years, I left an annual, automatic payment (a small one so I am not forgoing any meaningful cash back) on the card. The bank has a branch walking distance from where I live, and the payment is due in June, so it is a comfortable walk there if I don't stop off there on the way to doing other errands further away.

I laugh at all the junk mail I get from that bank trying to get me transfer balances; low, temporary interest rates, etc.

pacergal

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Ours bounces between 825-845.

I don't put much value on them, but I know lending institutions and insurances do.

Our credit report has inaccurate information on it, I have sent letters of explanation but it hasn't been taken off. (years ago we paid rent on DS apartment for 2 months, somehow, that address became on of ours on their questions)

I finally gave up trying to fix it.

I don't put much value on them, but I know lending institutions and insurances do.

Our credit report has inaccurate information on it, I have sent letters of explanation but it hasn't been taken off. (years ago we paid rent on DS apartment for 2 months, somehow, that address became on of ours on their questions)

I finally gave up trying to fix it.

- Joined

- Nov 27, 2014

- Messages

- 9,280

I can understand why a bank/mortgage/credit card company, etc cares about your credit score but why do insurance companies care?

Anyone "really" know.

They see it as an indicator of your level of responsibility. I guess I see their point, but obviously, one can have a good credit and still be an aggressive driver or not safe around their house and vice versa.

Personally, I think it’s unfair to those going through financial difficulties. Just because you’re have trouble financially doesn’t mean you’re irresponsible but “the man” likes to pile on when someone is down.

athena53

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- May 11, 2014

- Messages

- 7,392

I can understand why a bank/mortgage/credit card company, etc cares about your credit score but why do insurance companies care?

Anyone "really" know.

I was a property-casualty actuary when Progressive started this. There's definitely a correlation. People with higher credit scores (all else equal) have lower expected claims and thus can be charged lower rates. There are many possible reasons why- in this case, there's correlation but no definite causation. Some states forbid use of this variable because it affects poorer groups disproportionately or because there's no definite causal link. You can explain why people who have a lot of traffic violations are more likely to get in an accident. Not as easy to explain credit score as a rating factor.

Last edited:

The Cosmic Avenger

Thinks s/he gets paid by the post

We were ready to pay cash for our last vehicle when they offered us 0% financing. This was 2016-17, when interest rates were paltry, so I actually had to think about it, but the value of the car was a little less than what we had left on our mortgage, so we paid that off instead and wound up with a lower monthly payment for about the same amount of time!Twice I've paid cash for a car and they still ran my credit. Like the story above, the guy gave the line of "I've never seen a credit score this high". (Which I think is a sales smoke blowing line.) The second time was a real pain because my credit was locked and I had to unlock it to buy the car... That triggered me to take them up on a 0% loan. (Which I still paid off early because I don't like debt.)

frayne

Thinks s/he gets paid by the post

I can understand why a bank/mortgage/credit card company, etc cares about your credit score but why do insurance companies care?

Anyone "really" know.

It is all about risk. Having a low credit score could be, but not always an indicator of poor judgement or other risky behaviors. Not saying it is right or fair, just saying.

athena53

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- May 11, 2014

- Messages

- 7,392

I paid “cash” for a car because I was in the midst of a home refi. I specifically asked them not to pull my credit and they agreed. They called my credit union “off the record”. A month later I received the mandatory letter to notify me that they pulled a credit report anyway. I was furious and planned to file a complaint. That’s when I learned that they were entitled to do so without permission because I wrote a personal check. The refi was not affected.

That kind of made sense- I also paid for a new car with a check and they held the paperwork till the check cleared. Fine by me. I know they didn't check my credit because mine is frozen. The fun thing about freezing your credit is that you have to unlock it before anyonecan run a report. I signed all kinds of paperwork to be added to the Garden Club bank account as Treasurer and of course that included my SSN. They said nothing about doing a credit check. I got home and the banker called- they tried to run a credit check and my accounts were frozen. Busted.

He claimed it was just to verify that I was who I said I was- but they'd already taken a picture of my driver's license.

jazz4cash

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

I’ve been looking for some credible report that credit scores really do indicate risk that a borrower will not repay. I’ve never seen anything convincing.

Late pays are weird because missing the due date won’t ding you until you are >30 days late. Many of those disorganized folks are only going to be a few days late. Also I think some issuers like to charge late fees and benefit from higher rates. TG for online autopay.

Late pays are weird because missing the due date won’t ding you until you are >30 days late. Many of those disorganized folks are only going to be a few days late. Also I think some issuers like to charge late fees and benefit from higher rates. TG for online autopay.

mpeirce

Thinks s/he gets paid by the post

I don’t really understand caring about a “perfect” credit score.

I only pay any attention to it because it’s hard to avoid - it’s listed in a number of places I look at for other reasons.

I could see it being a red flag if it sagged for some reason, but beside that I simply don’t care.

I only pay any attention to it because it’s hard to avoid - it’s listed in a number of places I look at for other reasons.

I could see it being a red flag if it sagged for some reason, but beside that I simply don’t care.

retire48in2018

Recycles dryer sheets

- Joined

- Mar 12, 2008

- Messages

- 368

It’s not about cc being “evil”.

It’s a choice we made, to have no debt. It’s more about living with more peace and simplicity- for us.

I know there are those that follow Dave Ramsey that won’t do credit cards - just as those that like Clark Howard - that will always have a couple credit cards.

We listen to multiple viewpoints and decided to have no debt.

It’s a choice we made, to have no debt. It’s more about living with more peace and simplicity- for us.

I know there are those that follow Dave Ramsey that won’t do credit cards - just as those that like Clark Howard - that will always have a couple credit cards.

We listen to multiple viewpoints and decided to have no debt.

I’m only at 750, I have a perfect record but only have a home and 1 credit card that I pay off monthly. Started building credit like 5 years ago so there isn’t much history. I mostly worked on it with a $500 self funded card, whatever they’re called. Got rid of that about a year ago which was most of my credit history when they started charging a yearly fee to hold MY $500 on loans to myself… insane…

Not insane really, when you think about why it is that way and the opportunity it gives you to build (or in my case, repair) a credit rating. My first wife never met a credit card or loan she didn't like but being in my 20's I didn't recognize that for the danger signal that it was. She also thought it was okay to just arbitrarily skip a payment once in a while if it wasn't convenient to make it. We did talk about that one and it wasn't supposed to happen again but... well, you can guess the rest.

Fast forward six years and five years of marriage and I'm newly divorced and with an okay, but not great, credit rating because of the occasional missed and/or late payment history. So when I applied for a credit card with the credit union it was denied even after I explained the circumstances but they did then suggest the same thing that you did, and enter the "secured credit card". I had some money in the savings account there so I agreed to "lock away" $500 of it (this in 1986) and that would be the credit limit on my new Visa card. That way, if I didn't make a payment the credit union would take the money from the $500 and ding my credit rating. So I can have my credit card and their credit risk is zero. If I really needed that $500 I could have it but only after closing the Visa credit card account. Okay, fair enough.

And after a few years of making all my payments on time I reapplied for a credit card and lo and behold, it was issued! Yay! So I closed the secured credit card account and lived happily ever after and have one of those 800+ credit scores. So that's how that works.

Similar threads

- Replies

- 0

- Views

- 195