bmcgonig

Thinks s/he gets paid by the post

- Joined

- Aug 31, 2009

- Messages

- 1,580

I think he may have meant a money market account and not a money market fund.

Agreed, but he did say it had a ticker symbol. Either Blackrock or Morgan.

I think he may have meant a money market account and not a money market fund.

Treasuries are backed by the USG with no upper limit. ...

Fund Description

The Fund invests primarily in high-quality, short-term money market instruments. Under normal circumstances, at least 80% of the Fund’s assets are invested in securities issued by the U.S. government and its agencies and instrumentalities, including repurchase agreements that are collateralized solely by U.S. government securities or cash. Although these securities are high-quality, some of the securities held by the Fund are neither guaranteed by the U.S. Treasury nor supported by the full faith and credit of the U.S. government. To be considered high quality, a security must be determined by Vanguard to present minimal credit risk based in part on a consideration of maturity, portfolio diversification, portfolio liquidity, and credit quality. The Fund invests more than 25% of its assets in securities issued by companies in the financial services industry, which includes, without limitation, securities issued by certain government-sponsored enterprises. The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less.Government money market funds are required to invest at least 99.5% of their total assets in cash, U.S. government securities, and/or repurchase agreements that are collateralized solely by U.S. government securities or cash (collectively, government securities). The Fund generally invests 100% of its assets in U.S. government securities and therefore will satisfy the 99.5% requirement for designation as a government money market fund. Does this description of Vanguards money market fund contradict its self? It says it’s generally 100% government securities but it also says more than 25% is invested in financial services industry.

Now that's a concern from my POV... I just hope enough of them are not that STUPID to let it happen! Yes the debt is a problem and needs to be fixed but let's not cut off our collective noses to spite our collective faces and default.Unless the Congresscritters lose their frickin' minds and refuse to approve an increase in the debt ceiling!

No, it doesn't contradict itself. The first part... through 120 days or less is for money market funds and the sceond part ... after 120 days or less is for Government money market funds.

Just to be clear all financial institutions (and all bond investors) will have significant amounts of bonds underwater in a rising rate environment.

That by itself is not the issue, it is poor preparation for withdrawals or misunderstanding your deposit base.

But this also is a cautionary tale for the "interim losses are not real because I am holding to maturity" crowd. It is true until life happens.

Life happened to SVB, the losses were real, and it cost them the bank. It may also have sunk some businesses they banked.

Product summary

Vanguard Cash Reserves Federal Money Market Fund’s investment objective is to seek to provide current income while maintaining liquidity and a stable share price of $1. The fund invests at least 99.5% of its total assets in cash, U.S. government securities, and/or repurchase agreements that are collateralized solely by U.S. government securities or cash (collectively, government securities). The fund invests more than 25% of its assets in securities issued by companies in the financial services industry, which includes securities issued by certain government-sponsored enterprises. The fund is considered one of the most conservative investment options offered by Vanguard. Although the fund invests in short-term U.S. government securities, the amount of income that a shareholder may receive will be largely dependent on the current interest rate environment. Investors who have a short-term savings goal and are interested in a fund that invests in securities issued by the U.S. government or its agencies may wish to consider this option. So this is from the Vanguard site. It doesn’t mention 60 or 120 days. It says it’s a federal fund but it also says it holds the securities issued by financial by companies in the financial industry. So does that mean the fund could hold failed bank assets?

(emphasis mine)The Fund invests solely in high-quality, short-term money market instruments whose interest and principal payments are backed by the full faith and credit of the U.S. government. Under normal circumstances, at least 80% of the Fund’s assets will be invested in U.S. Treasury securities and in repurchase agreements fully collateralized by U.S. Treasury securities; the remainder of the assets will also be invested in U.S. Treasury securities and in repurchase agreements fully collateralized by U.S. Treasury securities. The only repurchase agreements that the Fund will invest in are those with the Federal Reserve Bank of New York that are fully collateralized by U.S. Treasury securities. The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less.

Government money market funds are required to invest at least 99.5% of their total assets in cash, U.S. government securities, and/or repurchase agreements that are collateralized solely by U.S. government securities or cash (collectively, government securities). The Fund generally invests 100% of its assets in U.S. Treasury securities and in repurchase agreements fully collateralized by U.S. Treasury securities and therefore satisfies the 99.5% requirement for designation as a government money market fund.

And bonds went up!

It is the name of the Pennsylvania town where the bank is headquartered.With recent fiasco of SVB, how would anybody buy a brokered CD from a Bank named

"Bank of Bird in hand"? There really is a brokered cd being sold on vanguard website with this name.

With recent fiasco of SVB, how would anybody buy a brokered CD from a Bank named

"Bank of Bird in hand"? There really is a brokered cd being sold on vanguard website with this name.

That's just down the road from Paradise.It is the name of the Pennsylvania town where the bank is headquartered.

You may be reading a bit much into the name. They also have a branch in Intercourse.

Still can get 4.80% 5 year non-callable CDs. Anyone interested? Still waiting for higher rates? 10 year treasury plummeting, oil plummeting. Everyone saying the fed will pause now. The pivot crowd is back.

Or are you waiting to see what happens with the CPI report tomorrow?

Hope you all snapped up your 5%+ treasuries while you could.

I guess "the bank formerly known as SVB" put an end to the celebration...

I just searched Fidelity "New Issues" for corporate bonds. Nothing listed.

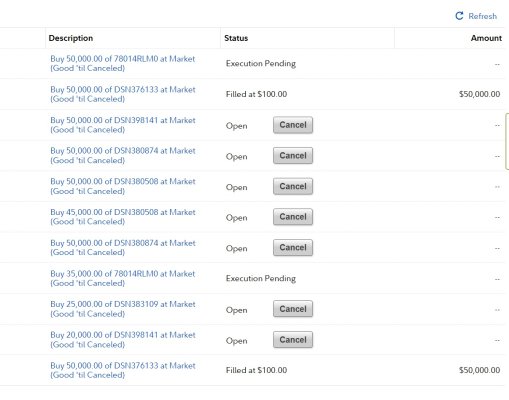

I wonder if the CD orders I placed last Friday will get cancelled.

I wonder if the "Golden Period" has become the "Bronze Period"? or maybe "Brass Period"?