pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

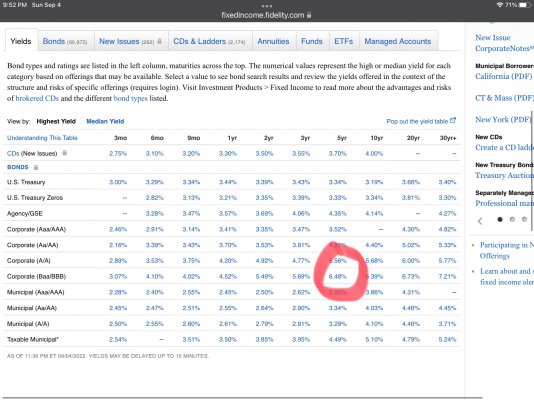

I don't buy stock index funds and would neve even consider buying them. . When you invest in a high yield bond at a large discount, you are speculating that company will continue to maintain their coupon payments to maturity. Your total gain can be projected at any time. To me individual bonds are always lower risk than stocks.

Terrible advice.

Hopefully those who plan to retire early are smart enough to ignore it and instead read one of John Bogle’s excellent books. Doing so could change their life and allow them to achieve financial independence.

While I concede that Billy C's response to Freedom's post was unduly harsh, there is nonetheless an element of truth there. Freedom was saying what he does and he can avoid equities because he has more than most.... nothing wrong with that... he has won the game and is choosing not to play in the equity sandbox.

However, most people need to own equities and have the growth of equities to accumulate an amount sufficient to retire. Equity investments don't necessarily need to be stock index funds or ETFs... they could be a portfolio of individual stocks. Very few forum members have retirements that are so fully funded that they can avoid any equity participation, expecially those still in acumulation mode.

Now that said, I do have concerns about the stock market the last few years with so much money chasing stocks prices have been bid up to a point where they didn't reflect the fundamental economics of many companies and P/E ratios were crazy high... casino mentality. As a result, I backed away from equities and my only current investments in equities are Dec 2023 and Dec 2024 LEAP options on the SPY which dropped my target AA from 60% stocks to ~32% stocks on a notional basis.

") .

.