Dawg52

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Damn, 80 lbs on med's. Guess I'm going to have to do more hiking with the mutt.

Welcome back.

Welcome back.

Welcome back! I've missed the debates you used to have with CT.

I've always loved that warm, sentimental streak you have.Welcome back, fartblossom...

Eh, I'll just work it out with their mommies while the kids are in school. Somebody did say I needed more hobbies

If that doesn't work, I have two video cameras inside the house that record everything. Which by the way, ends all of those "he said/she said" arguments in the game room.

That could get you into trouble.

I've always loved that warm, sentimental streak you have.

Nice to hear from you, CFB. You sound less sure of yourself than you used to be (that's a good thing). You'll come out of it just fine, maybe better than the original version.

CT pops up now and then over at Bogleheads - heh heh heh. Still have my 30 yr mortgage but I enjoyed Bacon and Bunnies with stuff on their head much more.

Now retiring from ER after a say 20 yr career and commiting some sinful deed like returning to w*#k!

heh heh heh - seems like you have a 'full time' schedule now anyway.

my son is already complaining when I kiss him goodbye at school.

Retirement wise, a lot of people ask if you can go too early and I always said "HELL NO!", but I found as I approached 50 I wished I'd done more, but I've been out of work for nearly 12 years now and I think I'd have a hell of a time getting myself employed right now. Not that I could do it with pets that need regular attention, cant be left home alone for 10 hours, and a kid that needs school drop off and pickup. Maybe after the dogs and cats pass on and Gabe is a little older, I'll try something out. Not sure if i'd try to go back to my old job or try something completely different.

About the only other really interesting thing is that I've been investing in the Lending Club with very good success. Its hard to deploy a lot of cash there quickly without taking on a lot of questionable notes, but I've been chugging away at it for six months and have about $70k in there. They gave me $1000 to start, I've got about 1900 notes, my NAR is 17.58% but with eventual defaults I expect that to drop to around 12%. I have 16 notes late >30 days and 3 in the 16-30 day. Total at risk right now is less than the grand they gave me, and as an oddity I've had 40 people pay the money back within a couple of months and half that many that are late. The LC guys find that very amusing for some reason. My interest take is about $3500 and my notes in lateness are ~$900. If that ratio holds, I'll continue to deploy cash. My very last 7 year penfed 6.25% cd's are maturing next year...

.I also have been questioning did I retire too early (CFB beat me by a year damn him!) cause after 13 years I have no illusions about my ability to find an interesting J*B that pay well, certainly in this horrid economy.

If had a do over I definitely would have gotten out of Silicon Valley when I did my timing late 99/early 2000 was pretty much perfect. But I wish I would have found a second act, and while volunteering has its rewards it just isn't the same as psychological rewards as a job and not mention the pay is way better than volunteering

It finally hit me that my best weeks months were more interesting than best months being retired. On the other hand my worse month being retired is way better than my worse month working. I just needed to find a mythical job that had no bad months.

CFB did you ever try Prosper.com? It soured me on the whole P2P lending business but I have been hearing positive things about lending tree. I am going to wait on this particular opportunity.

Do you still have rental properties? In the last year I have gone a bit nuts buying real estate in Vegas baby, A 4 plex, condo, 2 single family homes, and looking next year for more.

We were all like that. I remember when I was a kid I had the flu once and the first day back to school it was raining. My mom walked me all the way to the front door with an umbrella over my head, totally humiliating me. I know she was just doing what she thought was best.......but damn, I still remember that day some 50+ years later.

I love sneaking up on him on the playground and laying one on him. MrMoneyMustache put up an interesting post on Lending Club:CFB did you ever try Prosper.com? It soured me on the whole P2P lending business but I have been hearing positive things about lending tree. I am going to wait on this particular opportunity.

MrMoneyMustache put up an interesting post on Lending Club:

The Lending Club Experiment | Mr. Money Mustache

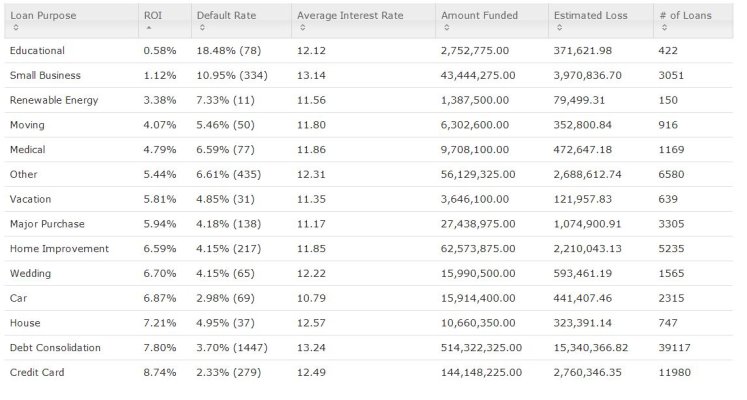

I'd be willing to bet dollars to donuts that isn't actually how Lending Tree does its expected default rate cause I don't think 5 years of data especially with relatively low number of loans funding in 2007 and 2008 by lending club is enough to make good prediction. Rather I imagine that the default rates are calculated based on expected default rate on people with similar credit scores as calculated by the credit reporting agency. In the case of Prosper these assumptions prove to be widely optimistic. I never was quite sure why this was the case, but my underlying assumptions was that is possible that credit card companies knew a wee bit more about making consumer loans than a start up and bunch of wanna-be-banker on the internetI could see that Lending club was automatically calculating the average interest rate of all of my proposed loans, subtracting the expected default rate based on their 5-year history of thousands of other loans with these characteristics,

.So good to hear from you. I'll never forget how much good advice you gave me when my elderly cat was so sick. You also gave me a good shoulder to cry on. Hope I can do the same for you since you're in charge of an aging menagerie.

My dad did shelter work for a few months and it crushed him. I don't think I'd do much better. I'd have 400 cats and dogs hiding out in my house.

You sound like Ralph Kramden.

Without FDIC insurance. And much less liquid.This is not an annual rate which is closer to 3.5% (a bit higher IRR). More or less in line with 3 year CD circa 2009.

Without FDIC insurance. And much less liquid.