MooreBonds

Thinks s/he gets paid by the post

I also have a healthy exposure to emerging markets/international. Overall, about 11.3%, including about 5% of portfolio in I-bonds

But you must consider your entire liquid assets, not just a partial selection.

2014 YTD time weighted return including dividends, commissions, and margin interest is 39.5% as of close of market Thursday 24 July.

Big winners are overweight single stock positions in AAPL, APC, PXD, V and CXO.

Let the bull run........

Very good and better then my return so far.I was thinking of posting the entire portfolio, but the way I track the total and change in entire liquid assets includes withdrawals from checking (generally $5k per month). With that, my entire portfolio including checking is 9.1%

Very good and better then my return so far.

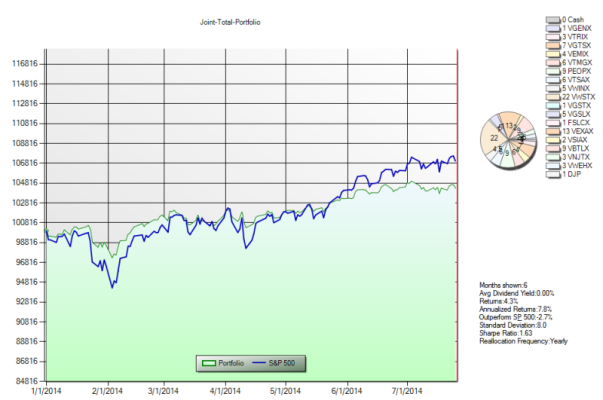

At the mid-year on July 1, ours was:

our portfolio +5.4%

benchmark #1, +5.4% (index only based portfolio)

benchmark #2, +5.7% (Wellington based portfolio)

+1.27 [emoji6]Somehow I suspect we are not all calculating this in the same way.

FYI, after more study of the tax issues, it turns out that I do not have to convert everything to Roth to be tax-free after 70. Income (w/d from t-IRA plus SS can still be at zero taxes below a certain w/d rate). If I die before everything is converted, DW should convert all the balance ASAP for simplicity.

Cheers from Baku

Hi, aj,Hey Ed, can you expand on this plan? For me (70 1/2 now), RMDs and most of SS is taxable, and any amount of IRA funds I convert to ROTH will be taxable?

Hi, aj,

After you both start taking SS, and the MRDs kick in after 70.5, you are permanently in a high tax bracket. And the surviving spouse is even worse off. (This applies to a single person, too.) No way around it.

Sorry to bring bad news.

Glad to have helped--I thinkEd, thanks for the explanation. Getting the IRA to Roth conversions done is the way to go. I didn't do that, but maybe I should have and now it's maybe too late. I need to run some tests on Turbo Tax and see where we can do small conversions and stay just under a 15% tax bracket (if possible). One thing we have done, which is not a favored tactic here, is purchased $250K level term life insurance policies on both of us a while back with us being beneficiaries of each others policy. If one passes within the policy period, the insurance payout funds will cover a lot of taxes and maybe some other expenses. Fortunately, we bought the policies at a good fixed price.

Another problem we have is that I still consult part time (that has to stop soon) and we have no tax deductions.

.We have small term life policies, too. They will help, of course, but I was trying to evaluate the core problem, which is simple in our case. I wanted a best-worst case. Anything besides that will be a welcome improvement.

Somehow I suspect we are not all calculating this in the same way.