What about this Chase offer? Perhaps this was mentioned already.

https://accounts.chase.com/consumer/banking/online/sapphirebanking

so just meet with their banker .. deposit $75k and you get $1k after 90 days ?

What about this Chase offer? Perhaps this was mentioned already.

https://accounts.chase.com/consumer/banking/online/sapphirebanking

so just meet with their banker .. deposit $75k and you get $1k after 90 days ?

You have to leave that $75K there (minimum balance) or there is a $25/month service fee. So probably best to watch the timing and just leave it there the 90 days.

I did ask Chase the question if I could use perhaps my Fidelity Brokerage or Roth account for the source of the direct deposit. The response was no, unfortunately those do not qualify. According to the terms for the direct deposit - needs to be an electronic deposit of your paycheck, pension or government benefits (such as Social Security) from your employer or the government. Oh well. Maybe someone else can benefit.

Haven't looked at this, but does small print have a penalty for closing account before, say, 6 months?

If you are referring to my Chase 1k post, there is nothing in the small print which I can see about length of time the checking account must stay open, except for the ~3.5 months.

Before the 11/9 deadline, I will be visiting a Chase branch near me to confirm there are no unusual gotchas.

If you are referring to my Chase 1k post, there is nothing in the small print which I can see about length of time the checking account must stay open, except for the ~3.5 months.

Before the 11/9 deadline, I will be visiting a Chase branch near me to confirm there are no unusual gotchas.

If you are referring to my Chase 1k post, there is nothing in the small print which I can see about length of time the checking account must stay open, except for the ~3.5 months.

Before the 11/9 deadline, I will be visiting a Chase branch near me to confirm there are no unusual gotchas.

While I'm not interested, I'm just wondering.... would an automated monthly transfer from one you your other accounts qualify as a direct deposit? So I set up and automated transfer of $1,500 on the 1st of each month from one of my other accounts... and then every 6 months get online and reverse it by transferring $9k from the Chase account back to the regular account... rinse and repeat.

I did ask Chase the question if I could use perhaps my Fidelity Brokerage or Roth account for the source of the direct deposit. The response was no, unfortunately those do not qualify. According to the terms for the direct deposit - needs to be an electronic deposit of your paycheck, pension or government benefits (such as Social Security) from your employer or the government. Oh well. Maybe someone else can benefit.

They lied to you. I don’t think they can tell the difference. I just did transfers from my Fido brokerage (non IRA). It qualified.

I use ST bond funds but that is usually discussed in different threads. People seem to prefer to discuss their safest type funds here.This thread is about CD's and MM's. But what about short term bonds? If you hold them through their durations (at least) you are likely to get the SEC yield as I understand it. Plus even if rates go up you then are set to profit from those higher rates.

Some comparisons:

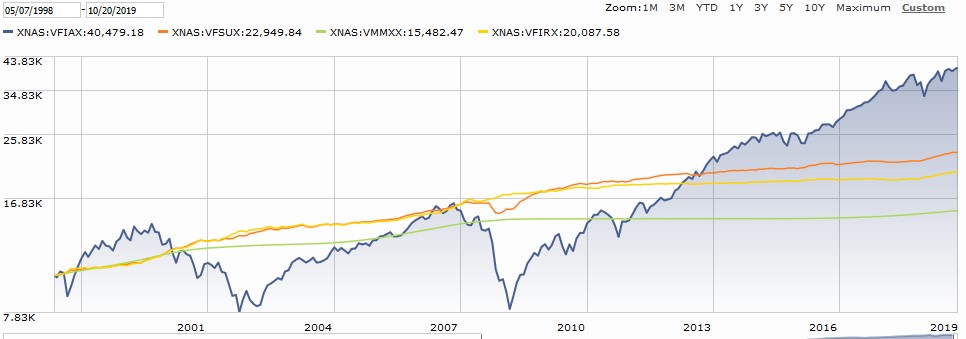

VFSUX Short term investment grade, 2.30% SEC yield, 2.6 yr duration

VSCSX, Short term corporate bond, 2.23% SEC yield, 2.4 yr duration

VMMXX, money market, 1.97% SEC yield

The objection that I can see is that short term IG bonds dropped in the 2008-2009 decline. If you look at the data it was clear that as stocks started to sell off in 2009 it would have been easy (and profitable) to move those IG bonds to short term treasury bonds (like VFIRX). It does take a bit of awareness though.

Here is a chart showing that 2008-2009 period we all remember:

I am mentioning this because of a recent inheritance and hence excess cash now.

Opinions?

I use ST bond funds but that is usually discussed in different threads. People seem to prefer to discuss their safest type funds here.

Not GTE?

Money going to Simple - $250 for $10k or $500 for $20k, money just has to sit there for 10 weeks. Open account now with $0, fund by 11/15.

https://www.simple.com/offer-v2

A better deal than the Chase 1k bonus, or if one has 95k they can do both.

True and that's why I wanted to jump on this one but then I calculated the difference between what VMMXX pays 1.97% currently (fully liquid) vs. this deal's 2.5% and the $100 hardly seems worth the effort. I used to have PenFed's 5% that matured last year but since then I haven't found a good offer like that so I've been keeping it in VMMXX.

How is the calculated difference only $100?

Using 20k, VMMXX will provide ~ $83 for 2.5 months vs. the $500 bonus at Simple.

Thanks!

Thanks!