pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

I don't remember how I stumbled across it ... I suspect it was a link in something else that I was reading.

I don't remember how I stumbled across it ... I suspect it was a link in something else that I was reading.

In fact I can’t find any fixed income link within the app. Is it webpage only content?

You guys are a little late to the party. It was announced on the Deposit.com blog in early October. See my post on 10-4.I don't remember how I stumbled across it ... I suspect it was a link in something else that I was reading.

A basic account on Seeking Alpha is free. I was able to see njhowie link in web browser.Thanks Howie! I use SA as much for entertainment as for financial info. It’s not worth 30/mo to me.

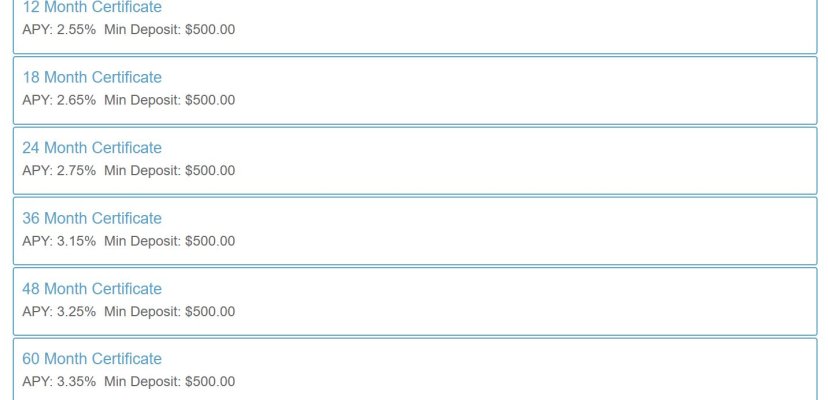

For Forum members in Wa St and some Oregon or Idaho counties at Potlatch Federal Credit Union Rates as high as 3.35 for 60 mon. 24 mon--2.75; 36 mon 3.15%

See attachment for full list

https://app.loanspq.com/xa/xpressAp...f8iDVEp9RWMEhcWBcdu2QySDjVIj3XKSnnrOtKJHUNYWQ

I like the rates, but am a little unnerved by this statement about cd rates:

"RATE INFORMATION: The dividend rate and the annual percentage yield may change every month. We may change the dividend rate for your account as determined by the Credit Union Board of Directors."

Above might be a normal policy, but usually buried in the fine print.

The way I interpreted was the "offer rate" could change but not after a CD is issued unless it is stated as a variable rate. I don't believe any of their CD are variable but you would need to confirm with them.

I do get the impression a credit union isn't able to change existing interest rate unless the rate caused them existential threat.

Well GTE tried it but was defeated.

.... Mainly because we usually exceed the $250k NCUA/FDIC limits.

Huh? No choice, don't get that.

A...

Besides, what do folks with $10 - $20m do to protect their cash?

Did not really have a choice, we do not like multiple institutions for our IRAs and have invested in CDs since 2000. So far fingers crossed, but we always chose highly rated Credit unions.

Why it is an different than putting $3m with one brokerage?

If I have more than $250,000 in a closed bank and I am paid $250,000 by the FDIC, what happens to the amount in excess of $250,000?

If for example, a depositor has only a single account with a balance of $[-]255,000[/-]$3,000,000, he or she would be paid $250,000 through FDIC insurance and would receive a claim against the estate of the closed bank for the remaining $[-]5,000[/-] $2,750,000 which is not insured. The depositor would be given a Receiver's Certificate as proof of this claim and would receive payments as the assets of the bank are liquidated.

SIPC insures brokerage assets up to 500k ($250k cash). Most brokerages add an additional layer of private insurance.Did not really have a choice, we do not like multiple institutions for our IRAs and have invested in CDs since 2000. So far fingers crossed, but we always chose highly rated Credit unions.

Why it is an different than putting $3m with one brokerage?

Besides, what do folks with $10 - $20m do to protect their cash?

For Forum members in Wa St and some Oregon or Idaho counties at Potlatch Federal Credit Union Rates as high as 3.35 for 60 mon. 24 mon--2.75; 36 mon 3.15%

See attachment for full list

https://app.loanspq.com/xa/xpressAp...f8iDVEp9RWMEhcWBcdu2QySDjVIj3XKSnnrOtKJHUNYWQ

GTE is a B+, personally I would not go with any institution with my retirement funds who are less that A and A+. Mainly because we usually exceed the $250k NCUA/FDIC limits.