MissMolly

Thinks s/he gets paid by the post

- Joined

- Jun 9, 2010

- Messages

- 2,140

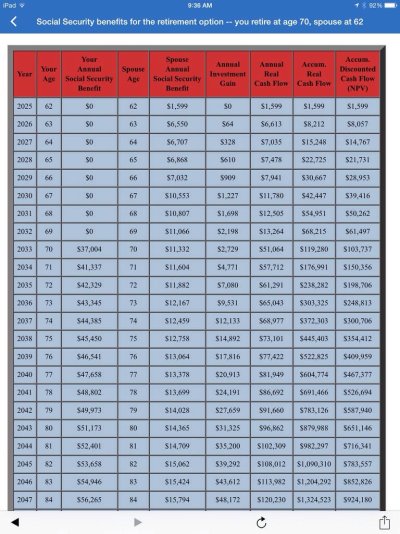

Here is another wrinkle that will apply to DW and me. She is 63 1/2 I am 65.

My FRA benefits are $ 2,358 and hers are $ 1,000.

DW is going to take her benefits earlier - age 64 1/2 when I am FRA at 66.

Her reduced benefits will be appx $ 855.

I will file for spousal benefits which will be 50% of $ 1,000. Since I am FRA I get the full 50% of spousal benefits, I am not penalized for her taking benefits early.

At a later date, hopefully at age 70 I will file for my own benefits. appx $ 3,100.

DW will then apply for spousal benefits which should be 50% of my $ 3,100 x's .85 which represents the "penalty" for her taking her benefits early.

Upon my demise, DW will get survivor benefits of $ 3,100.

If anyone sees an issue with the calculations, let me know, as I am very sure these options are available under the current SS program.

jpjr, I hate to burst your bubble, but I don't think what you are planning can be done. First of all, if a spouse files for their own benefits before they are full retirement age, they cannot come back later and file for spousal. You are only allowed to do that if when you first file for any benefits that you have reached full retirement age. It is only at that point that you have the choice. Also, a spouse can only claim 50% of your amount you would receive at your full retirement age - they do not get 50% of the amount you receive if you wait until you are 70. You are correct that if you wait until you are 66 you can file for your full 50% of your souse's PIA benefits and then file under your own at 70. You can read about it here Benefits for Spouses