What action had to be taken when 2 trillion dollars appeared in the stock market a couple of years ago? I forget...

party hearty? buy overpriced houses? retire early?

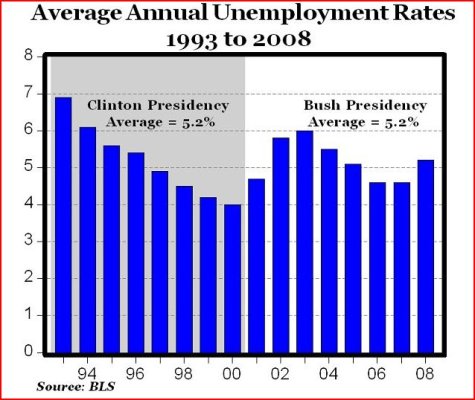

Maybe the worst won't come to pass, but saying the capital markets of the entire world are "just one market segment" seems to be denial. (Were it just technology, or just tulip bulbs, you'd be right, of course.) Unemployment was less of an issue in '93/'96 or '04/'06, IMO, in the first case because housing prices only dropped something like 5% I believe, and in the second because the housing bubble was creating the "wealth" that is now being destroyed.

August unemployment is reported as 6.1%.

It's the link between unemployment and ability to pay off the housing and other loans that underpin the system that makes this different. When Worldcom went bust only a contained circle were involved in that investment.

Everyone is now invested in over-priced housing thanks to the gov. takeover of FNM/FRE and the bailouts of MBS-sustained investment banks. Every tiny percentage of increased unemployment means that much less capacity to pay, which might seem trivial UNLESS you look at the giant inverted debt pyramid of leverage that was constructed on those tiny percentages. It's as if the entire country bought Enron and Worldcom on margin, is what it is, at least as far as I can see...

There are other aspects, too, like what this does to foreign investment and treasury yields and the weakness of the dollar, and reduced tax revenue.. things that affect everyone, not solely sector investors.

--

neither during the Enron debacle did the gov. allow banks to put regular customer deposits at the service of imploding entities:

Breaking Walls

The Fed also granted an exemption on a rule that limits banks' transactions with their brokerage subsidiaries, a move that provides securities dealers with another source of funding if they need it for market making this week.

http://www.bloomberg.com/apps/news?pid=20601068&sid=aQD6.DKvN3yQ&refer=home

Among the most important tools that U.S. bank regulators have to protect the safety and soundness of U.S. banks are the legal restrictions that limit the ability of a bank to lend to affiliates. Section 23A of the Federal Reserve Act provides that a bank may not lend more than 10 percent of its capital to any one affiliate or more than 20 percent of its capital to all affiliates combined. Of equal importance, any loan to an affiliate must be either fully collateralized by cash or U.S. Treasury securities or overcollateralized by other assets in an amount of 10 to 30 percent, depending on the type of asset or instrument used to secure the loan. Section 23A also prohibits the purchase of low-quality assets by a U.S. bank from its affiliates. Section 23B of the Federal Reserve Act requires that all transactions between a bank and its affiliates be conducted only on an arms-length basis. These restrictions are designed to limit the ability of an owner of a bank to exploit the bank for the benefit of the rest of the organization.

http://www.federalreserve.gov/newsevents/testimony/alvarez20080424a.htm

culled from:

http://www.nakedcapitalism.com

just like with the "temporary" TAF.. how long will this exemption/suspension last? Everything we have seen up to now seems to indicate that any loosening of the rules just encourages additional misbehavior and a worsening of the problem.