marko

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Mar 16, 2011

- Messages

- 8,462

I never bother to project out where I might be in the future with my portfolio; that's up to the whims of the market. I figure there's no reason to fret over not hitting the projection or celebrate beating the projection since it was based on some arbitrary time span and mr. market's arbitrary mood at the time.

It's more of an idle curiosity for me. More like: "if the trend continues, I'll be at $X". I don't plan, expect or fret anything until 12/31.

Never count the money till the money's in the bank.

It's more of a carryover from my work days when I was doing probability studies for forecasting sales.

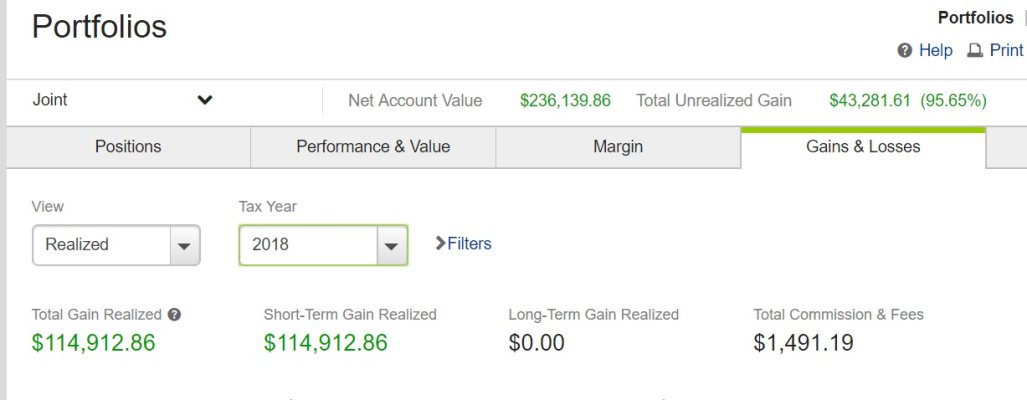

I just found it interesting to see an acceleration of performance (i.e. my balance growing faster) over the past month or two vs the first part of the year and see that as an encouraging sign.