jetpack

Recycles dryer sheets

- Joined

- Aug 2, 2013

- Messages

- 437

I'm in PA, looks like my rate is going up 20%. I thought the rates were suppose to be going down in my state?

I'm in PA, looks like my rate is going up 20%. I thought the rates were suppose to be going down in my state?

+1Shop around. You will likely do a lot better, and now there is no penalty to doing so aside from the time it takes to do so.

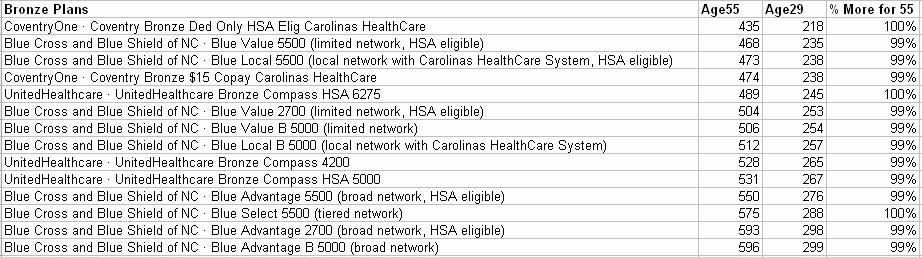

This is a great suggestion! I will do it now.When I looked at it briefly over the weekend, I had to put my age in as 29 to get any catastrophic pricing, since the standard rule is under 30 only. So despite there being tons of exemptions, they set up the website without all of the proper info.

So, to get an estimate, you have to enter your age as 29, see what the approximate ratio is between the catastrophic and bronze plans, then input your real age to see what the same bronze plan is at your real age, and then apply your ratio to get a SWAG on what the catastrophic plan might be roughly. Granted, it's a very big SWAG, but a reasonable guesstimate without any other info.

Great way to think about it. You are wise!I will try to get as much info as possible before selecting, but nothing short of driving 200 miles to find a provider and the medical facility is not an open air tent, I will go cheapest route possible. With insurance, ultimately you are paying for someone else's health issues or someone is paying for yours. As long as I am paying for others (and hopefully that will continue for an extended period) I will attempt to pay as little as possible in premiums.

Catastrophic plans are only available to those under 30 years old or with a special hardship exemption.

For example, if the health coverage options available to you would cost more than 8 percent of your income or if your insurance plan was canceled because it didn't meet the law's new standards, you may ask for a hardship exemption to apply for catastrophic coverage.

Read more: Is An Obamacare Catastrophic Plan For You? | Bankrate.com

Follow us: @Bankrate on Twitter | Bankrate on Facebook

Politics--will the SCOTUS gut the ACA? Will Congress try to repeal it (of course the POTUS will veto). What would you do?

Let me know what you think. Thanks for any and all opinions.

Using the proportional pricing swag suggested by MooreBonds I have come to the conclusion that the catastrophic policies are not much better.This is a great suggestion! I will do it now.

Two of the more common exemptions are 1) if your 2013 pre-ACA plan was cancelled and 2) if the lowest cost bronze plan available to you exceeds 8% of your MAGI (assuming your employer does not provide health insurance).

Using the proportional pricing swag suggested by MooreBonds I have come to the conclusion that the catastrophic policies are not much better.

Shop around. You will likely do a lot better, and now there is no penalty to doing so aside from the time it takes to do so.

I'm on the healthserpa.com site. The LOWEST plan listed is 20% higher than I was paying this year. There is NO shopping around.

Preliminary look at our Idaho ACA Blue cross plan for next year is about $75 more than last year and our subsidy goes down by about $25 based on the same income. So our cost will nearly double from $115 last year to $215 or so next year. Nearly a 100% increase in our cost. This does not sound right but I can't see where my figures are wrong. Any one else having such a high increase?

Sent from my iPhone using Early Retirement Forum

Without a subsidy ours could be $1000/month. I would calculate your % increase based on the unsubsidized plan.

Sent from my iPhone using Early Retirement Forum

So, if anyone figures out how a married couple can get individual policies with the subsidy, please post about it. We are considering an HSA plan, would like to get individual policies even if it means going with 2 different insurers.