REWahoo

Give me a museum and I'll fill it. (Picasso) Give

Question: "Am I crazy?"

Answer: "I'm not sure, but you do exhibit a number of interesting symptoms".")

Answer: "I'm not sure, but you do exhibit a number of interesting symptoms".

Can someone tell me why it is 100% certain that the dividend will decline with time. ... I will be the first to admit I don't have "the answer" but this seemed as plausible as many others out there

It's not 100% certain that the dividend will decline with time.It isn't.

People are looking at odds.

Who is more at risk of loosing everything, the investor with one stock (or bond) or the investor with 100?

What you are doing very well may work out great for you. But you also have a much better chance of getting hit harder than you would if you were diversified.

In short, you are not investing, you are gambling.

We don't know the future, but we know what's worked in the past. Not your blink-of-the-eye fads of the last 20 years, but the last century or so. Past may not be prologue but some defensive techniques have worked well in all market conditions. One of those defensive techniques has been diversification. Another defensive technique has been annuitizing a portion of your income. A third defensive technique has been educating yourself, and a fourth has been staying open to constructive criticism.So in summary then...nobody really knows do they. I certainly am not ignorant, and I am not trolling here either. I simply wanted to get the pluses and minuses. I think most people have been taught some basic tenants about equities and buy and hold etc. and have chosen to stick with that.

Good luck with that... feel free to come on back after you've done some reading.Well then...I guess I should bow to all of the experts and take my leave

snip...

I see no reason for never drawing down the principal. The key is just to have enough money so that you won't outlive your savings. Why die with tons of money in the bank just because it is technically one's principal? I think you have to do a 50+ year spreadsheet under different inflation scenarios and coupon rates to see what I mean. Under high inflation the principal balance becomes huge.

1974 50/50 ala Ben Graham's Defensive Investor, 1980 60/40 da policy or traditional pension porfolio, 2006 Target Retirement 2015. Retired at 49 1993 and yes I did own a small % of high yield corporate for a while to boost cash income while nursing my IRA past age 59 1/2.

I don't think you can equate NAV price with default rates on the held bonds.Yes, this is a crazy plan. Here's why.

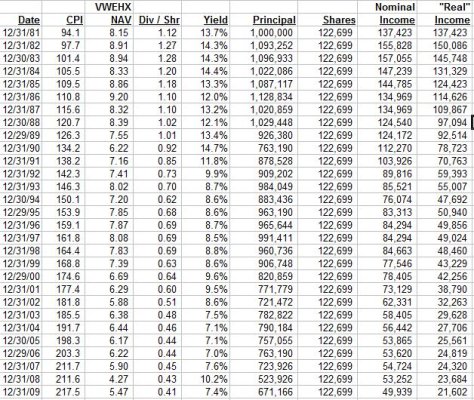

1) Part of the current yield on a high yield bond goes to compensate for their very high default rate. You can probably expect to lose a couple of percentage points per year averaged over the course of a business cycle in a HY bond fund to defaults. If you're spending the cash flow, you're essentially consuming the portion of your principal lost to defaults. You can see this pretty clearly in a long-term price chart of VWEHX. The fund started at an NAV of $10 in 1979 and is now down to $5.48 (a loss of nearly 2% per year compounded). So in 30 years the principal balance has shrunk by 45%. You can expect something similar over the next 30 years. And assuming a constant yield over the next 30 years, your cash flow will decline along with your principal.

The chart shows the Nav OVER THE LAST 20 YEARS to vary between 6 and 8 dollars a share.

Can someone tell me why it is 100% certain that the dividend will decline with time. Silverton 39 motor yacht.

I don't think you can equate NAV price with default rates on the held bonds.

Just like you can't equate the price of gold with the amount gold available.

More likely it has to do with the interest rates at the time being in the

stratosphere (prime rate was around 20%).

TJ

You may have just ruined this guy's chance for getting a Darwin Award. Well, for now.I did.

The reason is that the stated yield of a bond fund assumes that all of the bonds mature according to schedule at par. This is not true of a high yield fund. Bonds default and receive less than par recovery in bankruptcy. This gradually erodes your original principal.

But if the proof of the pudding is in the eating, then you are in for some very slim gruel. Here's what your income stream would have looked like had you invested $1MM in the Vanguard HY fund in 1981 and never sold a share . . . .

Yes there is going to be noise year to year but the overall trend for 30 years running is down. And it trends down for a very good reason. Assume you have a portfolio of 10 bonds each with $1,000 face value and an NAV of $10. If one of those bonds defaults and recovers 50 cents on the dollar your NAV goes down to $9.50. That process is going to happen repeatedly. Remember that most HY bonds are issued at par. Someone is buying those par bonds. And a meaningful fraction of those bonds will never pay par back, which means guaranteed principal loss for the market. That loss is presumably compensated for through coupon payments but if you spend all of your coupons, you'll slowly deplete your principal.

This is the price chart for VG HY bond fund. And as you point out, yields were declining during this entire time (which should cause bond prices to go up)

I did.

The reason is that the stated yield of a bond fund assumes that all of the bonds mature according to schedule at par. This is not true of a high yield fund. Bonds default and receive less than par recovery in bankruptcy. This gradually erodes your original principal.

But if the proof of the pudding is in the eating, then you are in for some very slim gruel. Here's what your income stream would have looked like had you invested $1MM in the Vanguard HY fund in 1981 and never sold a share . . . .

Also, remember your inflation probably will be different than the one used for TIPS.. it might not be enough to worry about, but I doubt it will be the same..

You still did not address the fact that you would have to save more to get the starting income you want.. that could be more than a decade of savings (maybe two)... not someone who wants to RE...

The method I have found that works quite well on a fixed income is to take only 45% of the yield as the starting basis of the income, to account for inflation. In the instance you printed with 1 million in investment one would take just 61,480 (6% of the total investment in this case) and reinvest the remainder in the fund.

Had that been done in the case you posted with the same inflation numbers and assuming reinvesting on 12/31 of the next year 2009 he would have ended with 668,365 shares and income of $274,030 with an inflation adjusted need of $142,936.

The interesting thing about this is the value of the portfolio in the end would be up 50% inflation adjusted and you would be nowhere near a failure and you would have supported a 6% withdrawl for 30+ years easily.

Now at present prices this means only pulling 3.37% of the total portfolio out each year. And a high yield fund certainly is very risky to do this with in my opinion, but not as risky with a 45% withdrawl as you may think.

Now at present prices this means only pulling 3.37% of the total portfolio out each year.

I do not see where he ever states he was trying to avoid a 2MM portfolio,

I imagine it is in efficient tax wise but what size portfolio is necessary to draw 72 k annually for 30 years...2.1M.

So in summary then...nobody really knows do they. I certainly am not ignorant, and I am not trolling here either. I simply wanted to get the pluses and minuses. I think most people have been taught some basic tenants about equities and buy and hold etc. and have chosen to stick with that.

Great response and great spreadsheet YrsToGo !

JG used to put great store by his GM junk bonds. Wonder how that's working for him these days.I agree... someone took the time to show the results... and the fault of the original post... but he said he is gone anyhow, so he will find out in a few years....

I can't say too much bad about the OP his returns have beaten mine in the last 10 years.

Making concentrated bets can pay off (my portfolio's average rate of return has been 9.57% over the last 10 years and maybe half of those gains can be attributed to a single stock) but it can also end in disaster.