Al18

Full time employment: Posting here.

Reported last month, Warren Buffet is pouring money into Japan and plans to increase stake up to 9.9% of holdings https://www.cnn.com/2023/06/19/investing/warren-buffett-japan-stock-market/index.html

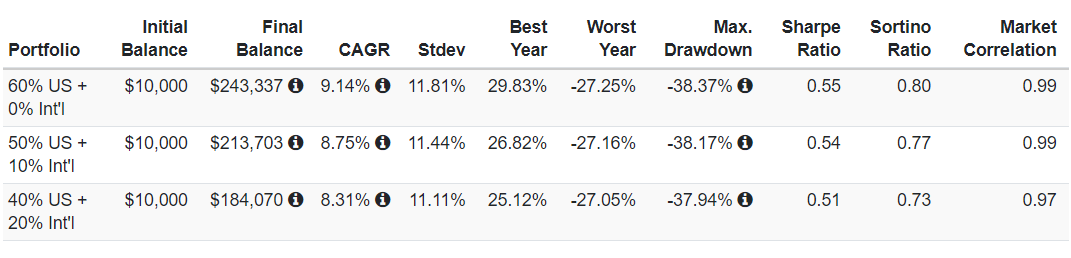

OK, I've been investing over 35 years both with an advisor and on my own I've been told to keep a percentage of my equities in International funds, around 25%. I have.

Looking back these funds haven't kept even close to US funds, let alone the SP 500. 10 year average is 5.05% for Vanguard International, others I hold are worse.

These International funds have been a boat anchor in my overall portfolio. Hindsight is clear, I should have stayed all US.

How long of a time frame do you give a sector to catch up ?

I no longer believe in diversification for the sake of being diversified. Heck, its darn hard to beat a portfolio that is 100% SP index over any period of time. 1 year, 10 years or 30 years. I don't see the need for International funds, other than the fact you can buy them cheap. You can buy them cheap because the don't increase in value much over time. You can buy them cheap next year too if you want.

Am I missing something? I tell everyone younger than me to pass on International or anything fancy, just buy the SP 500 index and go back to work.

Rant over.

") Indirectly.

Indirectly.

Never bet against the US.

I'm one more who has been out of international stocks for over 20 years agreeing with others that US companies have plenty of exposure to international business. Bogle and Buffet say they're not needed, that's good enough for me.

| Int'l Stock | |

| 2007 | 22.5% |

| 2008 | 14.5% |

| 2009 | 20.7% |

| 2010 | 19.9% |

| 2011 | 18.9% |

| 2012 | 21.1% |

| 2013 | 20.3% |

| 2014 | 17.9% |

| 2015 | 17.0% |

| 2016 | 17.7% |

| 2017 | 17.8% |

| 2018 | 16.2% |

| 2019 | 13.4% |

| 2020 | 10.8% |

| 2021 | 5.0% |

| 2022 | 8.9% |

I have been out of international funds for about 12 years now. My reasoning at the time and I believe those reasons will hold true in the future:I agree that international has lagged for many years. I got out of international probably 10 years ago if not longer. No regrets. Because I hold S&P and market index funds, by nature it has passive international exposure due to global companies. That is sufficient international exposure for me and my diversification.

I don't believe we are going to see the same intensity of US-centric growth

I’m not selling…. certainly not advising but, I just attended a round table of Schwab “experts” and they’re projecting that international stocks will outperform US stocks in the near future. Different valuation levels and different headwinds.

One thing to consider is that the actual total returns of some international funds is not properly represented simply by looking at the growth in etf prices as many of them tend to have larger dividends, which can make a large difference over time.