OP

OP

REWahoo

Give me a museum and I'll fill it. (Picasso) Give

Wuss.My WR so far:

2010 0.0% - unexpected bonus from 2009 work

2011 1.14%

2012 1.33%

2013 2.16% - projected

Wuss.My WR so far:

2010 0.0% - unexpected bonus from 2009 work

2011 1.14%

2012 1.33%

2013 2.16% - projected

I've just come to the end of my 3rd year, and my situation is non-COLA pensions supplying 70% of target spending on year 1.

My WR so far:

2010 0.0% - unexpected bonus from 2009 work

2011 1.14%

2012 1.33%

2013 2.16% - projected

I've just come to the end of my 3rd year, and my situation is non-COLA pensions supplying 70% of target spending on year 1.

My WR so far:

2010 0.0% - unexpected bonus from 2009 work

2011 1.14%

2012 1.33%

2013 2.16% - projected

I use the ending balance of each year for the next year. IOW, I'm planning on taking 3.5% from my portfolio balance (on Dec 21st, 2012) for expenses in 2013.2012 was the first full calendar year that I was withdrawing from my portfolio. Expressed as a percentage of the value of my holdings at the beginning of the year, my WR was 2.65%.

AA is at about 60/35/5

For my projected WR for 2013, do I express that as a percentage of the portfolio value at the beginning of 2013 or at the beginning of my ER?

bbbamI said:I use the ending balance of each year for the next year. IOW, I'm planning on taking 3.5% from my portfolio balance (on Dec 21st, 2012) for expenses in 2013.

For my projected WR for 2013, do I express that as a percentage of the portfolio value at the beginning of 2013 or at the beginning of my ER?

As noted in my update, all of my annual rates are expressed as a percentage of my initial portfolio value when I retired. This is based on the methodology used in the classic Trinity 4% SWR study, which made no mention of using anything other than the initial portfolio value in the calculation.For my projected WR for 2013, do I express that as a percentage of the portfolio value at the beginning of 2013 or at the beginning of my ER?

The devil is in the details.

Oh, and to provide a direct response to "So, what were all of you doin'?": Changing my underwear. Frequently.

So what's your safe Depends rate (SDR)?... leads one to ask if buying Depend diapers would be cheaper than throwing out soiled underwear.

2. Have you seen Raddr's update of his hapless hypothetical Y2K ER?

Raddr's Early Retirement and Financial Strategy Board • View topic - Hypothetical Y2K retiree update

A fun thread from the past...

Sure is. For example, the following reply ....

... leads one to ask if buying Depend diapers would be cheaper than throwing out soiled underwear. And then how much the cost would have to be before it's worth one's time to add it as a Quicken expense category.

We will try harder this year, with cruises to and from the UK, a cruise to Norway and Iceland, a month in Ireland, 2 weeks in France, a week in Spain, 4 weeks in Cornwall, Kent and Yorkshire and several more weeks visiting relatives in England.Wuss.

Alan,

A good way to handle your WR calculation when a blue bird like your unexpected bonus occurs would be to just add the bonus amount to your portfolio value and calculate the WR based on that. It's a bit misleading (for your own planning) to say the WR was 0.0%

I'm impressed. Will not show this to DW.We will try harder this year, with cruises to and from the UK, a cruise to Norway and Iceland, a month in Ireland, 2 weeks in France, a week in Spain, 4 weeks in Cornwall, Kent and Yorkshire and several more weeks visiting relatives in England.

...

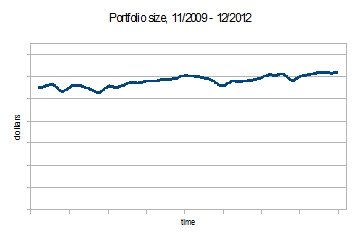

Withdrawals shown as % of initial portfolio or % of respective year portfolio?Here is my latest picture: