steady saver

Recycles dryer sheets

- Joined

- Apr 10, 2013

- Messages

- 498

I am finding I am not sleeping most nights.

While we are still within our ability to retire according to Firecalc, we're getting closer to an uncomfortable place - DH was set to retire this summer and now we are pulling back on that. We have paper losses of almost 1/3 of our FIDO accounts (includes 401K and individual investments). What helps me sleep now and then is that we have cash to ride out 3-4 years. (Our AA is roughly 70% equities, down from 78%. I let my fear of having to pay taxes on gains in order to rebalance down to 65/35 or 60/40 get in the way. Lesson learned.)

Because of that cash cushion, I felt like we were prepared and that we could sustain a 40% drop. And we can... if I thought it was going to come back up say within the next 3 years. I am just feeling uncertain in general. I know the coronavirus isn't going to last forever but the insults to the economy world-wide seem like they could be longer term and I'm feeling naive right about now.

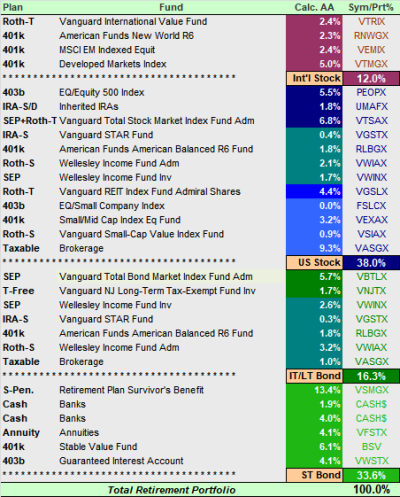

So, looking over our portfolio I see that our 401K investments are doing worse than my individual stocks which have actually done pretty good overall (I've historically enjoyed investing in individual stocks though I've not bought anything new in a few years...) Rather than sitting in this flip-flop between paralysis and just not looking at the market, I've been studying my FIDO reports and wondering what, if anything I could do/change...I set our 401K investments years ago and, I'm embarrassed to admit, I've not even looked at them in years.

Please give me your thoughts. Here's what we have:

36.10% invested in US Equity Index

25.35% in Blackrock EAFE EQ

14.77% in Midcap Equity

13.32% in US Debt Index

8.70% in FID Value K (FVLKX)

1.75% in our megacorp stock fund...this one is definitely going

We have a lot of options (346) to pick from so we're fortunate about that. Can you guide me in either general areas or even specific investments? I can look them up and see if they're available to us.

Also, we are still on automatic contributions (pre-tax). Would you continue that

or would you save that cash out for individual stock investments? Or something else?

Despite my angst, I'd like to do some investing while things are low (but not at the moment...) and if I can get our 401K investments in a better place, then I'd feel better about dipping my toes in once it seemed that we were on a a bit more stable footing and starting to trend back up.

I appreciate any suggestions that you'd be willing to share.

Many thanks.

While we are still within our ability to retire according to Firecalc, we're getting closer to an uncomfortable place - DH was set to retire this summer and now we are pulling back on that. We have paper losses of almost 1/3 of our FIDO accounts (includes 401K and individual investments). What helps me sleep now and then is that we have cash to ride out 3-4 years. (Our AA is roughly 70% equities, down from 78%. I let my fear of having to pay taxes on gains in order to rebalance down to 65/35 or 60/40 get in the way. Lesson learned.)

Because of that cash cushion, I felt like we were prepared and that we could sustain a 40% drop. And we can... if I thought it was going to come back up say within the next 3 years. I am just feeling uncertain in general. I know the coronavirus isn't going to last forever but the insults to the economy world-wide seem like they could be longer term and I'm feeling naive right about now.

So, looking over our portfolio I see that our 401K investments are doing worse than my individual stocks which have actually done pretty good overall (I've historically enjoyed investing in individual stocks though I've not bought anything new in a few years...) Rather than sitting in this flip-flop between paralysis and just not looking at the market, I've been studying my FIDO reports and wondering what, if anything I could do/change...I set our 401K investments years ago and, I'm embarrassed to admit, I've not even looked at them in years.

Please give me your thoughts. Here's what we have:

36.10% invested in US Equity Index

25.35% in Blackrock EAFE EQ

14.77% in Midcap Equity

13.32% in US Debt Index

8.70% in FID Value K (FVLKX)

1.75% in our megacorp stock fund...this one is definitely going

We have a lot of options (346) to pick from so we're fortunate about that. Can you guide me in either general areas or even specific investments? I can look them up and see if they're available to us.

Also, we are still on automatic contributions (pre-tax). Would you continue that

or would you save that cash out for individual stock investments? Or something else?

Despite my angst, I'd like to do some investing while things are low (but not at the moment...) and if I can get our 401K investments in a better place, then I'd feel better about dipping my toes in once it seemed that we were on a a bit more stable footing and starting to trend back up.

I appreciate any suggestions that you'd be willing to share.

Many thanks.

I thought I was doing the right thing.

I thought I was doing the right thing.