So when one hits 62 y.o., then if there is a 2% COLA increase for the year, I assume that only the next year estimate increases by the COLA.

Taking it further, I assume that the estimated 5 years out number, the COLA only applies to the first year and any further estimate increases are due to the "natural" 6 to 8% increases.

Correct?

Yes, sort of. All increases (or decreases from estimates) are used to calculate your PIA (primary insurance amount) which is the amount you get at your FRA. So any COLA cascades to all the other age calculations, since everything is based on your PIA. SS assumes no future COLAs when estimating your PIA, but does incorporate all previous COLAs.

Before age 62, as the average national wage increases each year, all previous years credited earnings are increased by an index multiplier tied to the ratio of 2 calendar years earlier and 40 years earlier. This index changes the bend points based on that increase. The effect is an increase in the maximum average indexed monthly wage, and an increase in ones SS PIA benefit. After that, there is a further increase once the COLA is applied (if there is one). After that, if you are still employed and paying in to SS at a rate that replaces one of your earlier indexed years, there is a further increase, because your indexed monthly average wage had to be recalculated. Remember that all increases are used for calculating your FRA amount.

As you said, Filing at 62 is an amount based off your FRA amount, roughly 6%/yr, (0.5%/mo) and all increases post FRA are based on 8% of your FRA amount. All COLAs are applied to your FRA, which is then used to calculate your actual benefit based on when you filed.

Once you have 35 maximum years earning credits, the additional years of earnings have very little effect, with most increases coming from COLA and indexed earnings. Once you hit 62, your bend points are then fixed, so all subsequent increases to PIA are only COLA, per year, compounded, and replacement of lower years with current years. If you already have 35 max, after 62, the PIA really only changes based on COLAs until you file.

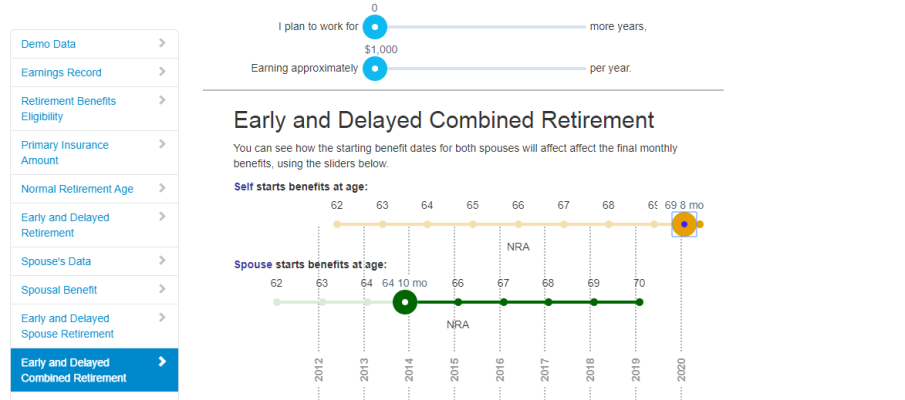

") Yep, an 11 year delay is long enough for me........

Yep, an 11 year delay is long enough for me........