You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Whatcha gonna do if ACA goes away?

- Thread starter norisk

- Start date

- Status

- Not open for further replies.

I predict this thread to quickly devolve and be shut down.

That said, I'm not worried about it. I think the probability is very low of that happening and if it does, I think many of the provisions of ACA will continue under a new name. It's established and counted on by enough voters that nothing too extreme will occur.

However, if it went away tomorrow I'd adapt just as I would to any other unlikely contingencies. I budget for the full amount without PTC and likely would be able to find a policy I could afford in the private marketplace. Biggest issue would be potential preexisting issues but I'm currently pretty healthy and don't think any of my diagnoses would cause me too much trouble.

I've always had a HDHP and always paid out of pocket so other than negotiated rates and my annual physical, I've not gotten anything out of my premiums so absent catastrophic I've been self-insured in a sense already.

That said, I'm not worried about it. I think the probability is very low of that happening and if it does, I think many of the provisions of ACA will continue under a new name. It's established and counted on by enough voters that nothing too extreme will occur.

However, if it went away tomorrow I'd adapt just as I would to any other unlikely contingencies. I budget for the full amount without PTC and likely would be able to find a policy I could afford in the private marketplace. Biggest issue would be potential preexisting issues but I'm currently pretty healthy and don't think any of my diagnoses would cause me too much trouble.

I've always had a HDHP and always paid out of pocket so other than negotiated rates and my annual physical, I've not gotten anything out of my premiums so absent catastrophic I've been self-insured in a sense already.

I predict this thread to quickly devolve and be shut down.

That said, I'm not worried about it. I think the probability is very low of that happening and if it does, I think many of the provisions of ACA will continue under a new name. It's established and counted on by enough voters that nothing too extreme will occur.

However, if it went away tomorrow I'd adapt just as I would to any other unlikely contingencies. I budget for the full amount without PTC and likely would be able to find a policy I could afford in the private marketplace. Biggest issue would be potential preexisting issues but I'm currently pretty healthy and don't think any of my diagnoses would cause me too much trouble.

I've always had a HDHP and always paid out of pocket so other than negotiated rates and my annual physical, I've not gotten anything out of my premiums so absent catastrophic I've been self-insured in a sense already.

Agreed, I would budget for paying my own way. There is no magic 'government' money, we only have each other to pay the bills. Any tax credits would be gravy.

This topic seems to lurk in the background and then reappear every couple of years.

Here are some of the past discussions of the exact same question.

ACA longevity https://www.early-retirement.org/forums/f38/aca-longevity-115065.html

Who is worrying about the ACA going away? https://www.early-retirement.org/forums/f38/who-is-worrying-about-aca-going-away-105754.html

A reminder to all to please avoid partisan political discussions.

Here are some of the past discussions of the exact same question.

ACA longevity https://www.early-retirement.org/forums/f38/aca-longevity-115065.html

Who is worrying about the ACA going away? https://www.early-retirement.org/forums/f38/who-is-worrying-about-aca-going-away-105754.html

A reminder to all to please avoid partisan political discussions.

- Joined

- Nov 17, 2015

- Messages

- 13,980

There are some things you can either:

Over over plan - save an extra couple million bucks

Stay working forever and never retire because there's always something amirite?

Leave the country

Or you can just deal with the reasonable expectations, and plan/budget for those, retire with a 3.5% SWR and a decent ACA plan, and be not spend the rest of your days worrying about zombie apocalypses, WW3, and any number of things that could or could not happen.

Over over plan - save an extra couple million bucks

Stay working forever and never retire because there's always something amirite?

Leave the country

Or you can just deal with the reasonable expectations, and plan/budget for those, retire with a 3.5% SWR and a decent ACA plan, and be not spend the rest of your days worrying about zombie apocalypses, WW3, and any number of things that could or could not happen.

VanWinkle

Thinks s/he gets paid by the post

Anything that gets passed that is now expected rarely goes away. Good or bad, that is the way it is. I used the ACA for 4 years until Medicare and I am sure it will be there for others for many years to come.

The ACA has many aspects, so it’s important to define what exactly one means with “goes away”. The parts that have the greatest impact on us are

- guaranteed access to comprehensive health care insurance

- premium assistance to help pay the cost

- essential health benefits that ensure policies meet standards of coverage

- a tiered system to allow “apples to apples” comparisons of coverage, premiums and cost sharing.

If someone is concerned about changes in the ACA, it seems to me the most important measure one can take is to make have enough money to pay the full unsubsidized cost of insurance plus maximum cost sharing.

- guaranteed access to comprehensive health care insurance

- premium assistance to help pay the cost

- essential health benefits that ensure policies meet standards of coverage

- a tiered system to allow “apples to apples” comparisons of coverage, premiums and cost sharing.

If someone is concerned about changes in the ACA, it seems to me the most important measure one can take is to make have enough money to pay the full unsubsidized cost of insurance plus maximum cost sharing.

- Joined

- Apr 14, 2006

- Messages

- 23,104

Here's what I would do if I were concerned about the fate of the ACA, First, I would pick out a plan that would be acceptable for coverage and co-pays. Then I would price out the premiums without any subsidies and make provision in my spending plan for that additional spending. If this required more portfolio to support that additional spending at a safe withdrawal rate, then I would work longer until I had a bigger portfolio. I can't think of any shortcuts.

The Cosmic Avenger

Thinks s/he gets paid by the post

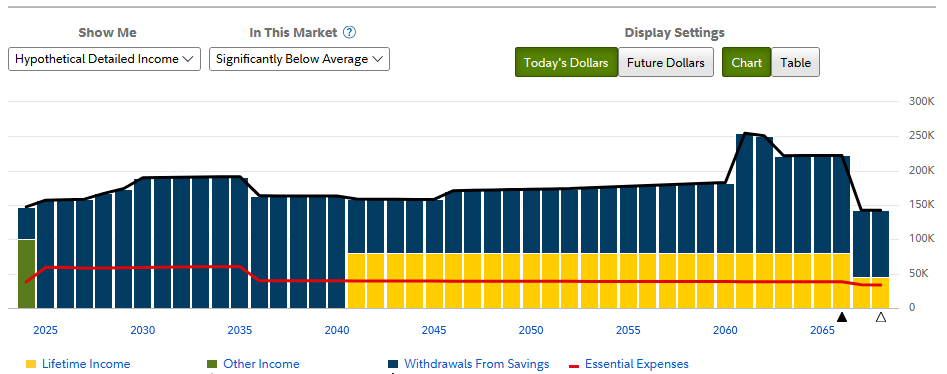

I would just cut back on travel and eating out and such. LBYM should be a skill that you don't lose even if you are out of practice. ") The red line below is the total of my essential expenses, which includes health care on the ACA market (without subsidies), which is why you see it go up when we retire, then back down at 65. I keep saying that flexibility is critical to me, and this is why. I'm not stuck on a specific number, I just kept adding travel $$$ as our score increased. And if we get tired of travel, we might build a year-round cabin on some lakefront family land.

The red line below is the total of my essential expenses, which includes health care on the ACA market (without subsidies), which is why you see it go up when we retire, then back down at 65. I keep saying that flexibility is critical to me, and this is why. I'm not stuck on a specific number, I just kept adding travel $$$ as our score increased. And if we get tired of travel, we might build a year-round cabin on some lakefront family land.

The red line below is the total of my essential expenses, which includes health care on the ACA market (without subsidies), which is why you see it go up when we retire, then back down at 65. I keep saying that flexibility is critical to me, and this is why. I'm not stuck on a specific number, I just kept adding travel $$$ as our score increased. And if we get tired of travel, we might build a year-round cabin on some lakefront family land.Attachments

athena53

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- May 11, 2014

- Messages

- 7,383

<snip>

That said, I'm not worried about it. I think the probability is very low of that happening and if it does, I think many of the provisions of ACA will continue under a new name. It's established and counted on by enough voters that nothing too extreme will occur.

I agree. Too many people depend on it. I was paying the sticker price (no subsidies) and I'm not sure what the market for coverage would have looked like without it. Too many people would end up uninsured.

Fermion

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

I actually don't think the insurance companies would want it to go away now.

Reason is pre existing conditions. Right now, they pretty much have to cover anyone for preexisting conditions at the start of each new period (or I guess special enrollment exceptions). I think this is offset by the requirement that you must have insurance (so the pool is large enough).

Also, some of the required coverage is not needed by everyone (pregnancy and mental health and drug abuse) but is included in most (all?) policies.

If ACA went away but the above is kept, it seems problematic.

Reason is pre existing conditions. Right now, they pretty much have to cover anyone for preexisting conditions at the start of each new period (or I guess special enrollment exceptions). I think this is offset by the requirement that you must have insurance (so the pool is large enough).

Also, some of the required coverage is not needed by everyone (pregnancy and mental health and drug abuse) but is included in most (all?) policies.

If ACA went away but the above is kept, it seems problematic.

The ACA has hung on by a thread historically, so I think it's probably 50/50 that it will last another 5 years, but I believe we are safe at least through the end of 2025 for the ACA.

I certainly hope it lasts because I've got a long way to go to Medicare and don't want to spend over $100,000 extra on health care coverage, but I realize there's no guarantee and me worrying about it won't do any good.

I certainly hope it lasts because I've got a long way to go to Medicare and don't want to spend over $100,000 extra on health care coverage, but I realize there's no guarantee and me worrying about it won't do any good.

"Just pay" will be out of the reach for many people, and they may have many more years than a "few" until Medicare, which is pretty expensive as well when you factor in the different parts, pieces, supplement, and deductibles, and much worse if you haven't met the 40 quarters of paying FICA taxes to get free part A. I'll also note that the ACA includes Expanded Medicaid for the lowest income people.Since Medicare is not too far off just pay full price for a few years until Medicare.

Invoke Plan B, fly out of country for a multi year vacation.

Another option is to go back to work, preferably a job with a decent health care coverage benefit.

Last edited:

ShokWaveRider

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

We utilized the ACA for 10 years until we qualified for Medicare. It was a godsend, saved us literally thousands. I feel sorry for folks who are forced to get healthcare on the open market if it goes away. The "Just Pay" recommendation is not practical for most who utilize it. The emergency room is a lot cheaper for them.

It would suck for a lot of people but the question is what would I do. Probably join Alan in the UK for a bit since I'm a dual national."Just pay" will be out of the reach for many people, and they may have many more years than a "few" until Medicare, which is pretty expensive as well when you factor in the different parts, pieces, supplement, and deductibles, and much worse if you haven't met the 40 quarters of paying FICA taxes to get free part A.

Another option is to go back to work, preferably a job with a decent health care coverage benefit.

I see. That's not an option for me. I would probably have to cut my discretionary spending allowance by 50% for several years to pay the higher costs. I'm not sure how likely going back to work is for me at this point, especially if the recession finally hits by the time the ACA might go away.It would suck for a lot of people but the question is what would I do. Probably join Alan in the UK for a bit since I'm a dual national.

Since Medicare is not too far off just pay full price for a few years until Medicare.

Invoke Plan B, fly out of country for a multi year vacation.

OP is talking 10 years between ER and Medicare so I understand his concerns as we were aged 55 and 54 when we retired. If I didn’t have access to my ex-employer retiree plans or there was a good chance of them being withdrawn, the decision to retire would have been a much harder choice. As it happened the employer did remove all their subsidies for retirees after a year or 2 so it quickly became very expensive.

Fermion

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

I didn't notice the OP's age but we are that same age range now even though we have been retired for 8 years already.

Honestly, when it first came out it was a worry, but I think it has become sticky and unlikely to just "go away" instantly.

It could change. They might try to do some asset based means testing, although that is a bit messy to implement.

Just think about the pre-existing conditions thing I mentioned. To entirely pull away the ACA means the requirement to insure pre-existing conditions has be withdrawn as well. If you don't do this, the numbers are not going to work for the insurance industry. (BTW, who do you think has a quite large lobby?)

If you got rid of the ACA but kept the requirement to insure people with pre-existing condtions, then a LOT of people would just wait to get insurance until something really bad happens (cancer diagnosis, major surgery needed, etc.). Yes, some would fall through the cracks, needing services before insurance could be obtained, but I think many of the very expensive treatments that happen over years would be forced on the insurance companies.

It is a world of mess if you get rid of the ACA and leave in the requirement that everyone HAS to have insurance. I don't think that is possible.

Honestly, when it first came out it was a worry, but I think it has become sticky and unlikely to just "go away" instantly.

It could change. They might try to do some asset based means testing, although that is a bit messy to implement.

Just think about the pre-existing conditions thing I mentioned. To entirely pull away the ACA means the requirement to insure pre-existing conditions has be withdrawn as well. If you don't do this, the numbers are not going to work for the insurance industry. (BTW, who do you think has a quite large lobby?)

If you got rid of the ACA but kept the requirement to insure people with pre-existing condtions, then a LOT of people would just wait to get insurance until something really bad happens (cancer diagnosis, major surgery needed, etc.). Yes, some would fall through the cracks, needing services before insurance could be obtained, but I think many of the very expensive treatments that happen over years would be forced on the insurance companies.

It is a world of mess if you get rid of the ACA and leave in the requirement that everyone HAS to have insurance. I don't think that is possible.

mpeirce

Thinks s/he gets paid by the post

What if ACA goes away?

Status quo for me.

I've stayed on my HSA/High deductible pre-ACA plan since the ACA came into being.

Fermion

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Status quo for me.

I've stayed on my HSA/High deductible pre-ACA plan since the ACA came into being.

Do you feel like the ACA has increased, decreased, or had little effect on the amount you pay for your pre-ACA high deductible plan? Do those plans allow for exceptions for ACA required coverages like drug treatment and mental health?

N02L84ER

Thinks s/he gets paid by the post

DH retired 8 years before ACA became law. I also retired before ACA became available. We simply planned to pay 100% of our insurance costs before we retired.

Marc

Recycles dryer sheets

It would be nice if ACA switched from income based premiums to wealth based premiums.

- Joined

- Nov 17, 2015

- Messages

- 13,980

DH retired 8 years before ACA became law. I also retired before ACA became available. We simply planned to pay 100% of our insurance costs before we retired.

Well we were "simply planning" when we started our serious ER planning, and that was just before the ACA became law, so we had an idea of a policy and price.

But....years later, would we even still qualify for insurance that the providers are willing to sell? Would the conditions, though relatively minor, we've tacked on in the last dozen or so years make it a bit more difficult? "We don't cover that/you" isn't something money can easily solve...at least not a very great deal of it.

"Oh...now you have High BP? Now you take a Statin? Er...you had a lump removed, and a pre-cancerous skin thing?" Any number of things might have crept up in the past years that weren't issues pre-2012 or so. And that can get denied as pre-existing.

Can't always just shop for a policy once you've become undesirable to insurers. Can't just go back to work and get coverage in your late 50's when you've been out of the job market for a decade.

So, yeah, these are some of the many reasons I don't see it getting canned. There are 24+ million of us, on ACA-covered plans alone, and another how-many millions of 18-26 year olds on their parents insurance who would no longer be covered.

Could subsidies be slashed? Sure, then it's just money. But the whole thing? My bet is that each year it stays makes it less and less likely to go.

- Status

- Not open for further replies.

Similar threads

- Replies

- 115

- Views

- 5K

- Replies

- 7

- Views

- 437