Concerns about ACA going away?

I have been on the fence about retiring for about 2 years now. I might have pulled the trigger late last year but to my surprise my company agreed to let me work remotely as long as I return occasionally. My short term plan is to visit different areas of interest in 4-week stretches to see if I would want to retire in one of those places, then return to my current location for a week before heading out again. I won’t sell my condo since I’ll be returning occasionally; if and when I find the right location then I’ll sell and move. These trips are expensive, especially while maintaining a residence, I figured I should keep working to subsidize the cost.

I just found out that my boss is leaving and, while I can still do the remote work thing, I worry about who will take over. I do not want to be stuck with a rotten boss, I’ve had that before too many times and I won’t go through it again. While I think I should still try to get through to November so I can get some additional vested stock grants (probably and extra $16K worth…not a ton of money but it’s mine), I think it will be time for a change.

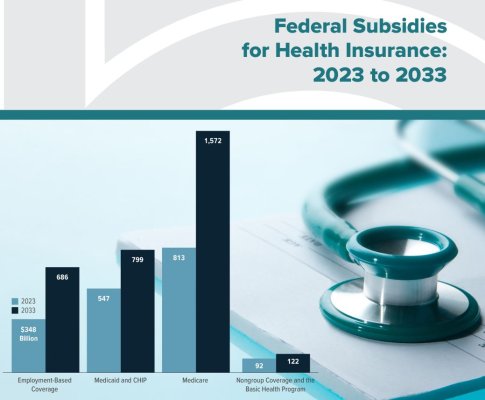

The reason this post is in the Health forum: other than the cost of my visits to other cities, my big concern is health insurance. I know there is ACA, not ideal but I’ll take it.

[mod edit]

For those of you who rely on ACA, how worried are you about it possibly going away in 2025 or 2026? What would you do for coverage? If you were me - single, still working, age 53/almost 54 - would a possible ACA repeal keep you from retiring?

While it’s fair to say that I’m a worrier and that I should just retire already (my last asset review, two weeks ago, was a net worth of $4.85M, which includes a condo that I estimate would net $500K after closing costs; it doesn’t take into account my taxes which could be high this year), the fear of not having good health insurance worries me. I had a health scare early this year, which has reinforced my concerns about not having good insurance.

Thoughts are welcome, thanks.

")