wanaberetiree

Full time employment: Posting here.

- Joined

- Apr 20, 2010

- Messages

- 718

[FONT="]Please note, the Schwab site still reads that you can take SS early, then repay the amount received to re-set at a high amount. This is no longer the case, do NOT plan on this option.[/FONT]

from Schwab site

If you previously elected to receive early Social Security benefits at a reduced rate, you have the option of paying back to the government what you've already received. You could then restart benefits at a later date to take advantage of a higher payout. This option is limited to one year's worth of benefits.

If you are receiving Social Security Retirement benefits and you change your mind about when they should start, you may be able to withdraw your Social Security claim and re-apply at a future date.

However, if you change your mind 12 months or more after you became entitled to retirement benefits, you cannot withdraw your application.

Note: You are limited to one withdrawal per lifetime.

Early or Late Retirement

I was planning on waiting until 70 to collect SS. Looking at my spread sheet I will probably start at 69 and four months and begin collecting in December of the year I turn 69. I chose December due to this statement on that URL page listed above: (I will seek clarification before reaching 69)

"If you retire before age 70, some of your delayed retirement credits will not be applied until the January after you start benefits. "

Bottom line, it would take until my early ninety's before making a one percent difference in collected funds. (~12K)

I would rather collect 30k up front at 69 and give up 12k at 90.

Agree with you on the COLA adjustment. Using your assumptions (6% earned, 2% COLA), I get that 66 beats 62 if I live to 81 1/4 and 70 beats 66 if I live to 86 1/2. Are you getting similar results?

I'm getting 66 beating 62 around age 76, but the same age you got for 70 beating 66. I'll be monitoring it as I go; if the market tanks, for example, I may take SS earlier so that the investments can recover.

Something these generic articles don't mention is the quirks of benefits.

- spouse collects spousal benefits from FRA until 70... clearly it pays to wait till 70 in that age because the spousal benefit is free money.

EDIT: I just ran my Numbers in the Social Security Calculator and for taking my SS at age 69 1/2 (In December of the year I turn 69), it would only take about 6 years to 'Break-Even', by Delaying to Age 70. This would be around age 76. I'd like to see your numbers on how you arrived at only ~12K by Age 90.... We're off by a mile somewhere.

I'll at least wait until 66, but after that it's going to be a year to year thing depending on the market.

I’ll give it a shot, whichever way is right I plan on waiting until 70ish instead of 62 or 66 to claim as I prefer a higher annuity amount. Looking at the calculations made me go hmmm, why not start collecting a little early.

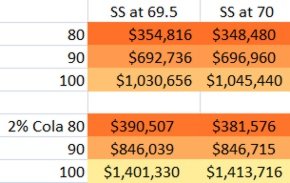

The SS Delayed Retirement Credits Calculator provided the percentage of PIA. 69.5 1.28 & 70 1.32 were used.

The example uses a PIA of $2200

Excel’s Future Value function: =FV(rate,nper,pmt) 69.5 =FV(0.02,10.5,-33792) 70 =FV(0.02,10,-34848)

Rate used 0 and .02 for cola; nper 69.5 used 10.5 years , 70 used 10 years etc.; pmt 69.5 -33792, 70 used -34848

I’ll give it a shot, whichever way is right I plan on waiting until 70ish instead of 62 or 66 to claim as I prefer a higher annuity amount. Looking at the calculations made me go hmmm, why not start collecting a little early.

The SS Delayed Retirement Credits Calculator provided the percentage of PIA. 69.5 1.28 & 70 1.32 were used.

The example uses a PIA of $2200

Excel’s Future Value function: =FV(rate,nper,pmt) 69.5 =FV(0.02,10.5,-33792) 70 =FV(0.02,10,-34848)

Rate used 0 and .02 for cola; nper 69.5 used 10.5 years , 70 used 10 years etc.; pmt 69.5 -33792, 70 used -34848

That's a lot of numbers. But, have you ran the Social Security Calculator with your exact figures? I did with mine and I 'break-even' in about 6 years or age 76 by delaying from 69 1/2 to age 70.

So, I think there is something wrong with your formula. Use the Calculator downloaded from the S.S. Website for a more accurate Picture.

That's a bet I'm taking!

Don’t think we need a calculator to sort this out. A difference of 6 months in starting social security, #2 pencil math should handle it.

Yearly draw at 70 is 34,848 and at 69.5 is 33,792 for a difference of 1056.

You get a half year head start at 69.5 33,792/2 = 16,896 take away 1056 every year until you get even.

16896/1056= 16 which puts break even out to 85 not 76

Feel free to use your PIA * 1.28 and !.32 to check.

Edit to add: decided to go ahead and plug 85 in Excel:

When I saw that quote on the SS site a red flag went up. My preference is to do the figuring myself, but in this case they make the rules. I appreciate the hint on how to see it implemented by using their calculator, even if I was slow on the uptake. ThanksThe Social Security Calculator. (The detailed one, with a record of all earnings) gives me a "Delayed increment Factor" of 1.20 for age 69 1/2. Not 1.28. ----

So, this is because as you stated in your first post.- "If you retire before age 70, some of your delayed retirement credits will not be applied until the January after you start benefits. " So, The Calculator was using 1.20 instead of 1.28

Social Security Detailed Calculator

[(1.28*6)/(1.32-1.28)/12]+70 = 85 & 364 days[(1.28*6)/(1.32-1.28)/12]+70 = 86