I am going to be very specific about who I would like to respond to this question. If you are excluded, please do not feel left out as your plan is simply different from mine. So here goes!

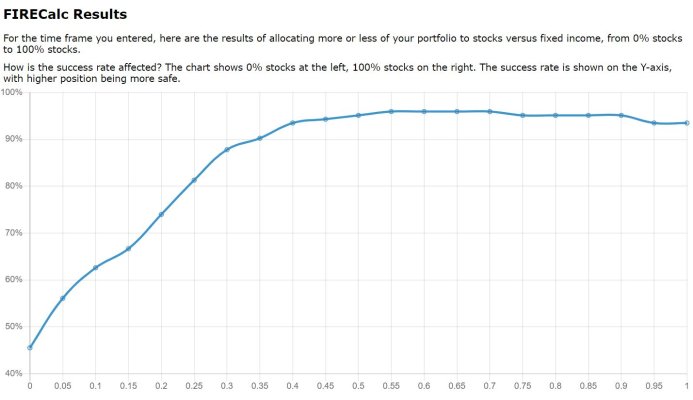

If you do not mind sharing, what is your asset allocation s/b if you do not have any other source of income other than current or future social security and financial assets ie. your s/b/c portfolio? Please do not respond if you have income producing real estate, a pension, or any income source beyond SS and your portfolio.

To avoid getting too much into the weeds, I am combining the bond and cash components into one category. I also get that funding levels can have a tremendous impact on willingness/need to take on risk so it is hard to account for that fact with a simple question and therefore I will ignore the behavior. For bonds, IF you have taken dollars from your portfolio to create an income stream, then I still consider that bonds and cash. One could argue that taking financial assets to buy rental property should be included in 'bonds,' but I would rather not.

The most obvious assumption is that you did not retire until your financial assets met a minimum acceptable level.

My data:

We are 57/54, 50/50 asset allocation, and only have SS.

If you do not mind sharing, what is your asset allocation s/b if you do not have any other source of income other than current or future social security and financial assets ie. your s/b/c portfolio? Please do not respond if you have income producing real estate, a pension, or any income source beyond SS and your portfolio.

To avoid getting too much into the weeds, I am combining the bond and cash components into one category. I also get that funding levels can have a tremendous impact on willingness/need to take on risk so it is hard to account for that fact with a simple question and therefore I will ignore the behavior. For bonds, IF you have taken dollars from your portfolio to create an income stream, then I still consider that bonds and cash. One could argue that taking financial assets to buy rental property should be included in 'bonds,' but I would rather not.

The most obvious assumption is that you did not retire until your financial assets met a minimum acceptable level.

My data:

We are 57/54, 50/50 asset allocation, and only have SS.