Floridatennisplayer

Recycles dryer sheets

- Joined

- May 3, 2014

- Messages

- 485

Glad I put 400k in a Single premium annuity a few years ago.......at least that’s 400K I don’t have to worry about! Maybe I should have gone higher.

Yes, I'm a bit high in equities, I'm thinking about lowering it by 5%.

But not now.

Just wait a few days. The market will lower it for you.

Asset allocation is severely personal IMO.

I really don’t worry about using Dec 31 and Jan 2 as my dates. Jan 2 is often an up market day and part of a Santa Claus rally, but most years I am not buying stock on that day but if anything selling. I use the Dec 31 value in my withdrawal calculation, and then rebalance as needed on Jan 2.As far as timing for rebalancing.... some thoughts......

One needs to have this defined in their IPS. My own says rebalancing within +/-5% of my target AA is allowed at my own descretion throughout the year. If the market moves beyond those bounds I have to rebalance immediately. I also insist that rebalancing happen atleast once per year at a time of my choosing.

I caution folks not set late December or early January as their default time to rebalance. The reason is I believe selling or buying can be exacerbated by electronic trading and auto rebalance at end of year and beginning of year and one doesn’t want to be on the wrong end of that. Better to use these times at your discretion rather than as a mandatory time to do so.

Just my opinion...

I probably should have built age into my AA from the beginning, but did not. Instead, I went from a 100:0 (equities:fixed) AA during accumulation phase, to a 45:55 AA during my entire retirement. I slowly switched over from 100:0 to 45:55 during last few years before I retired and had it in place before the 2008-2009 recession hit.

I have found this 45:55 AA was something I could stick with like glue throughout the terrifying days of that recession. Consequently I feel that AA was very well tested during those times and worked for me. So, I think I will just hang on to it throughout whatever is to come.

Actually I was unusually lucky, in that the economy provided a test of my "stick-to-it-iveness" or lack of same during 2008-2009, just before I retired in late 2009. I think I was more of a seasoned investor coming out of the recession than I was going into it.

Anyway, the answer to the question "Reevaluating your AA?" is pretty much no, although I have thought of going to 110-age and thus tying it to my age, but probably will not do that.

I think that is slow enough that I won't feel like a DMT. Also my actual AA today is (41.6) : (58.4) so all I will have to do is less rebalancing during the first week in January, when I always rebalance.

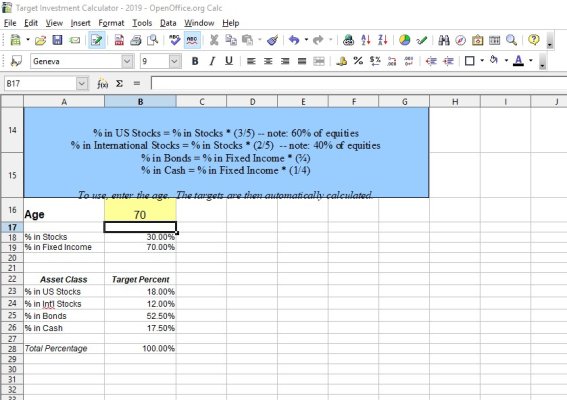

After thinking about it for a week and a half, I have decided to go to 110-age. I am 70 now, so I'll make the shift over a three year period:

age | date | Target AA | 110 Minus Age

70 | 12/30/2018 | 45:55 | 110 - 70 = 40

70 | 1/1/2019) | 42:58 | 110 - 70 = 40

71 | 1/1/2020) | 40:60 | 110 - 71 = 39

72 | 1/1/2021) | 38:62 | 110 - 72 = 38

I think that is slow enough that I won't feel like a DMT. Also my actual AA today is (41.6) : (58.4) so all I will have to do is less rebalancing during the first week in January, when I always rebalance.

.

. : and decided to just include the cash reserve. By doing so makes my spreadsheet flow a lot easier. .

: and decided to just include the cash reserve. By doing so makes my spreadsheet flow a lot easier. .Well, I sort of reallocating my AA for 2019 already.

I say sort of because since retiring,I wasn't counting my cash reserve as part of my AA so reallocated according to that. But then every year working through my spreadsheets that I go through start of every year to reallocate I struggle. So I said "Scr*w it!"

The good news is now I have some extra cash to dump into the market to get to my simpler target AA

It's hard to know what to do with cash sometimes! I used my leftover cash from 2018 as my annual withdrawal (for 2019 this time). Essentially, leaving it in the bank has the same effect as returning it to Vanguard and then withdrawing it again, a 3.84% WR based on my lower 12/31/2018 portfolio value. In 2018 I did not spend enough. I do plan to improve on my Blow That Dough initiative, and hopefully having it right here at hand will help with that endeavor this time; but realistically much of its function will be as a cash buffer for unexpected big expenses.

Almost makes me want to have the roof replaced before the Giant Market Crash that might or might not happen soon. But, my roof isn't leaking at all and it is maybe 10-15 years old, so that would be a bit premature.

I did my reallocation to 42:58 yesterday morning. When I logged in to Vanguard a couple of hours ago, they still didn't have the revised number of shares of each mutual fund so that I could doublecheck my computations. Grrr. I thought that when I switched to brokerage accounts, these things would show up more quickly but I was mistaken.

.+1. Exactly how you said it. I hadn't needed to rebalance last year as my DCA into Large Cap and smaller DCA into Mid Cap set me straight all year long. If the market rebounds I will re balance when that 5% threshold triggers it.As far as timing for rebalancing.... some thoughts......

One needs to have this defined in their IPS. My own says rebalancing within +/-5% of my target AA is allowed at my own descretion throughout the year. If the market moves beyond those bounds I have to rebalance immediately. I also insist that rebalancing happen atleast once per year at a time of my choosing.

I caution folks not set late December or early January as their default time to rebalance. The reason is I believe selling or buying can be exacerbated by electronic trading and auto rebalance at end of year and beginning of year and one doesn’t want to be on the wrong end of that. Better to use these times at your discretion rather than as a mandatory time to do so.

Just my opinion...

Well, I sort of reallocating my AA for 2019 already.

I say sort of because since retiring,I wasn't counting my cash reserve as part of my AA so reallocated according to that. But then every year working through my spreadsheets that I go through start of every year to reallocate I struggle. So I said "Scr*w it!"

The good news is now I have some extra cash to dump into the market to get to my simpler target AA

.