A long read, but worth it.

https://medicare.gov/Pubs/pdf/02110-Medicare-Medigap.guide.pdf

A good review for me... We have been on medigap since it began, around the year 2006 I think, and on medicare since 2001, when we became eligible.

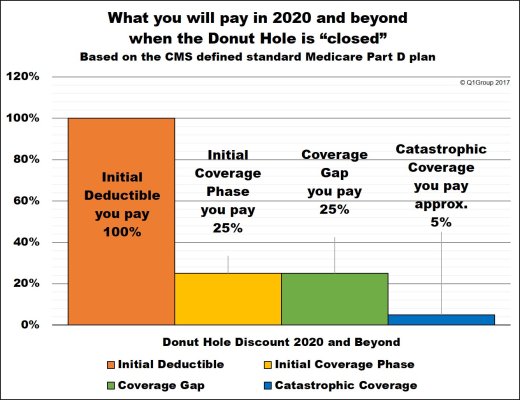

While there is no easy way to compare supplement policies one of the most important things to consider and this can be very important. Here is a current list of co-pays by drug tier for one plan.

Now, while this doesn't seem too important now,especially for those who don't take many medicines, it can become VERY important later. In many plans, some of the latest drugs are not covered in any tier. An example... The drug Xarelto costs (retail) about $521.00 for a 30 day supply, and even in the GOODRX plan $424.

The other part of this, is that the Medigap plans hold no guarantees. This year, one of my own drugs was dropped from the "approved" tier, costing me an additional $600/yr., and 2 more were changed from tier 1 to tier 2. No recourse.

Checking this out is the equivalent of taking a full year college course, though there are apparently some government websites that offer a drug cost calculator. I couldn't find them.

Would be interested in the "average" costs of medicare/medigap at different age levels.

Good luck. Not your imagination that this is a tough decision to make.