NW-Bound

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Jul 3, 2008

- Messages

- 35,712

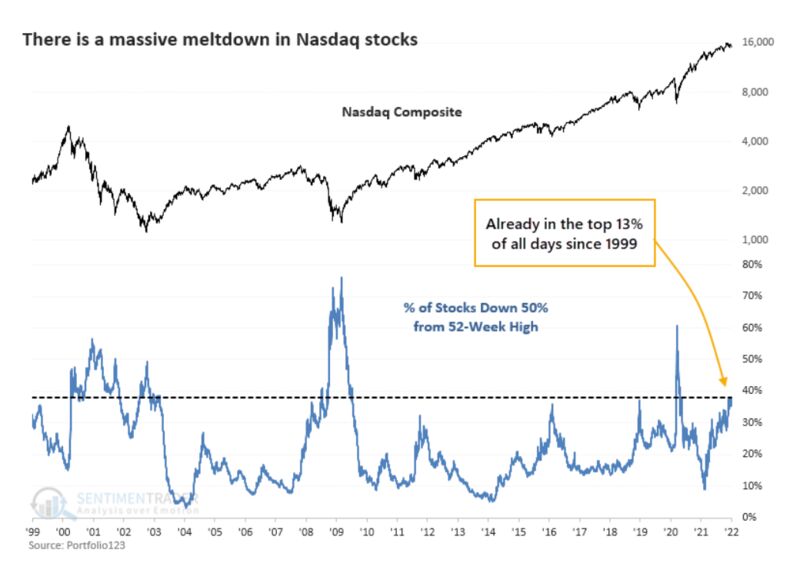

Yesterday, the Dow dropped 393, and that's -1.07%. The S&P was down -1.94%, and the Nasdaq was the worst at -3.34%.

I was working on fixing a refrigerant leak on a mini-split, and when I got done and looked at my stocks again after the market closed, saw that the market had taken a hard tumble. The cause: the Fed's released meeting minutes showed a hawkish stance that the market did not expect. Hah!

Inflation was higher than 7% and people were shrugging it off, thinking the Fed would not dare taking away the punch bowl?

The ARK ETFs by Cathie Wood took a hard hit, losing more than 7% yesterday. I don't have any of these funds but look at them often as an indicator of market froth. They went up big in 2020, and when I learned of them in early 2021 they already topped out and have been going downhill since.

I have been watching my portfplio, and try not to have high P/E stocks. Even my growth tech stocks have a P/E not higher than that of the S&P. Not every stock went down. Some of my mining and industrial metal stocks went up yesterday, as well as some defensive names. Of course, more of my stocks went down than up, and my loss was more or less commensurate with my stock AA of 70%.

It's going to be an interesting year.

I was working on fixing a refrigerant leak on a mini-split, and when I got done and looked at my stocks again after the market closed, saw that the market had taken a hard tumble. The cause: the Fed's released meeting minutes showed a hawkish stance that the market did not expect. Hah!

Inflation was higher than 7% and people were shrugging it off, thinking the Fed would not dare taking away the punch bowl?

The ARK ETFs by Cathie Wood took a hard hit, losing more than 7% yesterday. I don't have any of these funds but look at them often as an indicator of market froth. They went up big in 2020, and when I learned of them in early 2021 they already topped out and have been going downhill since.

I have been watching my portfplio, and try not to have high P/E stocks. Even my growth tech stocks have a P/E not higher than that of the S&P. Not every stock went down. Some of my mining and industrial metal stocks went up yesterday, as well as some defensive names. Of course, more of my stocks went down than up, and my loss was more or less commensurate with my stock AA of 70%.

It's going to be an interesting year.

Last edited: