It's easy to find folks who will benefit financially from the ACA who are for the ACA. It's a bit harder to find folks who will be ACA financial losers pushing as hard for it!

It actually isn't. I spent yesterday morning with many such folks at church. At least half, probably closer to two-thirds, of our congregation is certifiably affluent, "income above the cliff". Yet support for ACA is almost ubiquitous - perhaps even more so among those who won't benefit from it as compared to those who would. Very often we focus at church on matters that clarify the reason why so many people, who wouldn't benefit so much from the act of supporting such poverty relief efforts, do so anyway.

No, but personal situations aside we should all be able (now or when the thing is put into place) to see if it really decreased medical costs overall (e.g. as a % of GDP). The other major metric will be access to care: compared to what we had, and compared to other options.

The "system" we had was a wasteful, patchwork mess. There's no going back to that--even if we wanted to. And we'll dump this new system, too, if a majority of people believe we can do better.

This new system is a necessary first step. ACA will make the costs of health care far more visible to folks, until now shielded from the effect of the high cost of health care on those who are less affluent. With those costs now no longer swept under the rug, I think Americans as a group will be ready to start addressing the high costs in a more comprehensive way.

For me, the most logical approach would be to allow an agency to negotiate rates for health care, pharmaceuticals and medical devices, for the entire nation. Effectively, let Medicare, the military, and the Federal government as a civilian employer, all negotiate rates, and then mandate "me too" provisions for any ACA-compliant plan that wishes to benefit from the lower costs that any of those negotiation efforts yield.

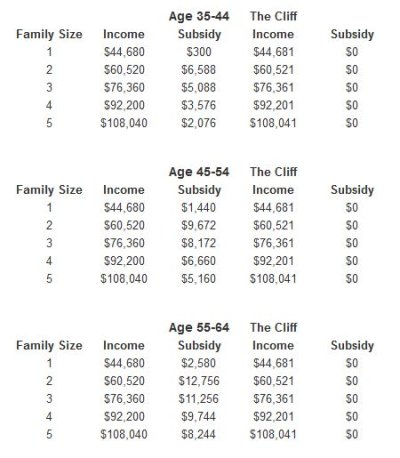

One last note: Claims that there is a "subsidy cliff" are greatly exaggerated. For the vast majority of people with income over 400% FPL, it's like claiming that there is an income tax "cliff". This kind of over-emotionalized and erroneous language is a misunderstanding, at best, a deliberate deception at worst. The subsidy is capped in a graduated manner, as follows: (Note the numbers highlighted in red.)

Up to 133% FPL

2% of income

133 - 150% FPL

3 - 4% of income

150 - 200% FPL

4 - 6.3% of income

200 - 250% FPL

6.3 - 8.05% of income

250 - 300% FPL

8.05 - 9.5% of income

350 -

400% FPL

9.5% of income

You'd have to spend over $35k (9.5% of 400% FPL) on individual health insurance for that boundary to even come into play. We have the best individual health insurance offerings in the country, here in the Commonwealth, according to a US News analysis, and not surprisingly the most expensive in the nation as well. I just did up a rate-quote for a 60 year old, male smoker, and still got a rate of under $6k (

LINK) - that's without subsidy, straight-up, cash-on-the-barrel. If you want to add the out-of-pocket maximum to the rate, fine: Still only $11k. I couldn't make the rate get close to $35k, even heaping on loads of premium services.

Furthermore, there is an out-of-pocket spending limit that includes everyone, not just those under 400% FPL:

100 - 200% FPL

1/3 HSA limit ($1,983/individual; $3,967/family)

200 - 300% FPL

1/2 HSA limit ($2,975/individual; $5,950/family)

300 - 400% FPL

2/3 HSA ($3,967/individual; $7,933/family)

Above 400% FPL

100% HSA limit ($5,950/individual; $11,500/family)

I hold an MS degree in mathematics, so yes I would prefer all such arrangements by the government to be algebraic functions where you plug the input in and every difference of 1.0 in the input gets churned through the formulas and results in a chance in the result. However, that's not the way most Americans want things. Step-function tables are preferred to formulas for that reason. That doesn't make anything into a "cliff".

")