MattInAustin

Dryer sheet aficionado

- Joined

- Feb 19, 2004

- Messages

- 26

First, it has been a long long time since I have posted here under a different username and even then I didn't do much. So hello again ") And apologies in advance for coming in with an incendiary topic.

And apologies in advance for coming in with an incendiary topic.

I used to be against getting a lifetime SPIA given the 4% rule seemed solid and you get to keep your money in hand for whatever comes up and enjoy a possible big upside down the road. Couldn't really see the sense of annuitizing. Plus I have always felt too young to get the longevity insurance aspect of it.

Now I am not so sure. Many of the retirement "experts" seem to feel 4% is a little risky (I am 53 yo). When I retired back in 2015 I somewhat arbitrarily decided 3.5% fixed would be 95%+ safe. I still feel that way and usually take out that much or less every year. That said, there is always something in the back of my head that says "the future could be very different than the past".

So I look at SPIA quotes and see rates are going up. I can get over 3.5% with a 4% "inflation" increase every year from an A+ insurer. Higher than average CPI, but inflation, as you all know, has been much higher for extended periods. CPI has averaged around 3.3% since 1914. From 1968-1991 CPI averaged around 6%. That was a pretty bad time to retire as well.

Now I am wondering if there might be an annual return where it makes sense to annuitize up to 25% of my portfolio to act as all or part of my fixed income? Or maybe enough to cover my base living expenses. Then, with a nice floor I could increase risk on the equity and "other assets" side which would help with the over 4% inflation risk.

At 5% with a 4% guaranteed adjustment I think I would do it.

At 4% I would be very tempted.

At 3.5% I am ambivalent.

I am curious at what SPIA return rate (if any, I know there are big downsides) folks would consider annuitizing a portion of their portfolio?

One other piece of information that is critical for me, I believe there is around a 10% chance we could have interventions in the next 20 years that would extend our healthspan and lifespan another 5-10+ years. To me that is a significant risk to drawing down a liability matching portfolio. I follow this science relatively closely and the progress in understanding and ameliorating the effects of aging are astonishing.

And apologies in advance for coming in with an incendiary topic.I used to be against getting a lifetime SPIA given the 4% rule seemed solid and you get to keep your money in hand for whatever comes up and enjoy a possible big upside down the road. Couldn't really see the sense of annuitizing. Plus I have always felt too young to get the longevity insurance aspect of it.

Now I am not so sure. Many of the retirement "experts" seem to feel 4% is a little risky (I am 53 yo). When I retired back in 2015 I somewhat arbitrarily decided 3.5% fixed would be 95%+ safe. I still feel that way and usually take out that much or less every year. That said, there is always something in the back of my head that says "the future could be very different than the past".

So I look at SPIA quotes and see rates are going up. I can get over 3.5% with a 4% "inflation" increase every year from an A+ insurer. Higher than average CPI, but inflation, as you all know, has been much higher for extended periods. CPI has averaged around 3.3% since 1914. From 1968-1991 CPI averaged around 6%. That was a pretty bad time to retire as well.

Now I am wondering if there might be an annual return where it makes sense to annuitize up to 25% of my portfolio to act as all or part of my fixed income? Or maybe enough to cover my base living expenses. Then, with a nice floor I could increase risk on the equity and "other assets" side which would help with the over 4% inflation risk.

At 5% with a 4% guaranteed adjustment I think I would do it.

At 4% I would be very tempted.

At 3.5% I am ambivalent.

I am curious at what SPIA return rate (if any, I know there are big downsides) folks would consider annuitizing a portion of their portfolio?

One other piece of information that is critical for me, I believe there is around a 10% chance we could have interventions in the next 20 years that would extend our healthspan and lifespan another 5-10+ years. To me that is a significant risk to drawing down a liability matching portfolio. I follow this science relatively closely and the progress in understanding and ameliorating the effects of aging are astonishing.

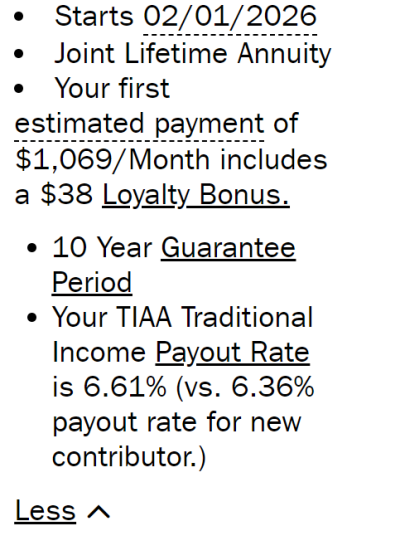

I already talked to them, and it will be for as long as I live. We don't have kids - so nobody really to leave it to except distant relatives if any.

I already talked to them, and it will be for as long as I live. We don't have kids - so nobody really to leave it to except distant relatives if any.