Taxes were somewhat of a grey area for me up until recently. My spreadsheet contains cells for $ withdrawal (based upon a withdrawal % chosen from a drop-down), $ total income (to account for pension and social security (if chosen to include those items, again from a drop-down) and federal taxes (state/local taxes are my next project). I created an Excel VBA function to calculate federal taxes based on the withdrawal (from investments) and regular income (i.e., pension/ss). [Edit begin] I then put the calculated tax in the main spreadsheet, calculate fixed expenses based on this tax amount (i.e., fixed expenses known beforehand + taxes), and any discretionary money left over (total income - fixed expenses).[Edit end] If anyone finds it helpful, I include the code below. It's not perfect, as it assumes all of the investment withdrawal are either qualified dividends and/or long-term capital gains from taxable accounts. But it brings me close. I'm sure it can be easily modified to calculate taxes on withdrawals from tax sheltered accounts. I just figured, I can probably draw from taxable accounts until RMDs, at which time DW and I will be collecting social security. The function also assumes you're filing married filing jointly, but again, that's just a matter of changing the values in the tax reference sheet. Finally, the function assumes you're taking the standard deduction as a married couple filing jointly.

The calculation of tax uses another sheet that I use as reference with tax brackets. Basically:

Income Floor (In my spreadsheet, column E)

Income Ceiling (In my spreadsheet, column F)

Bracket Amt (ceiling - floor) (In my spreadsheet, column G)

Regular income tax rate (In my spreadsheet, column H)

Short-term capital gains rate (In my spreadsheet, column I)

Long-term capital gains rate (In my spreadsheet, column J)

Here is the VBA function with comments. I hope someone finds it useful. If you find problems with it, I'd appreciate it if you let me/us know.

Code:

' Takes withdrawal amount and total income amount as params

Private Function CalcTaxes(cWithdrawal As Currency, cTotalIncome As Currency) As Currency

Dim cRegularIncome As Currency

Dim cInvestmentIncome As Currency

Dim taxBracketCell As Range

Dim cBracketAmtTot As Currency

Dim cTaxAmt As Currency

Dim nTaxBracketRow As Integer

Dim cStandardDeduction As Currency

' Add fixed property tax, which is contained in a reference sheet

cTaxAmt = Sheet7.Range("PROPERTY_TAX").Value

' Get regular income and apply standard deduction contained in a reference sheet

cRegularIncome = cTotalIncome - cWithdrawal

cStandardDeduction = MaxVal(Sheet7.Range("STANDARD_DEDUCTION") - cRegularIncome, 0)

cRegularIncome = MaxVal(cRegularIncome - Sheet7.Range("STANDARD_DEDUCTION"), 0)

' Calculate tax on regular income

cBracketAmtTot = 0

nTaxBracketRow = 2

' Iterate through the tax bracket sheet. Column G corresponds to Bracket Amt

For Each taxBracketCell In Sheet6.Range("G3:G11")

If cRegularIncome < cBracketAmtTot Then Exit For

nTaxBracketRow = taxBracketCell.Cells.Row

cTaxAmt = cTaxAmt + (MinVal(cRegularIncome - cBracketAmtTot, taxBracketCell.Value) * Sheet6.Range("H" & nTaxBracketRow))

cBracketAmtTot = cBracketAmtTot + taxBracketCell.Value

Next taxBracketCell

' Apply any remaining standard deduction to investment income

cInvestmentIncome = cWithdrawal - cStandardDeduction

' Calculate tax on investment income

If cRegularIncome < cBracketAmtTot Then

cTaxAmt = cTaxAmt + (MinVal(cBracketAmtTot - cRegularIncome, cInvestmentIncome) * Sheet6.Range("J" & nTaxBracketRow))

End If

nTaxBracketRow = nTaxBracketRow + 1

' Iterate through the tax bracket sheet. Column G corresponds to Bracket Amt

For Each taxBracketCell In Sheet6.Range("G" & nTaxBracketRow & ":G11")

If cRegularIncome + cInvestmentIncome < cBracketAmtTot Then Exit For

cTaxAmt = cTaxAmt + (MinVal(cRegularIncome + cInvestmentIncome - cBracketAmtTot, taxBracketCell.Value) * Sheet6.Range("J" & taxBracketCell.Cells.Row))

cBracketAmtTot = cBracketAmtTot + taxBracketCell.Value

Next taxBracketCell

' Return calculated tax

CalcTaxes = cTaxAmt

End Function

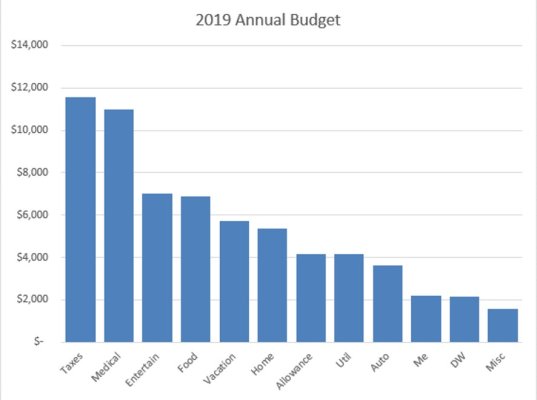

plus I didn't realize how much higher dental expenses would be at age 65 compared with age 45. Luckily I had enough of a "fudge factor" to cover these expenses.

plus I didn't realize how much higher dental expenses would be at age 65 compared with age 45. Luckily I had enough of a "fudge factor" to cover these expenses.