MN317

Dryer sheet aficionado

- Joined

- Mar 3, 2013

- Messages

- 26

An interesting overview of market timing.... and its many flaws.

Calling the Turns: Why Market Timing Is So Hard

Calling the Turns: Why Market Timing Is So Hard

)!

)!From that article's endnotes:

According to the SPIVA Scorecard compiled by S&P Dow Jones Indices, for periods ended December 31, 2014, 76.25% of actively managed U.S. large-cap equity funds underperformed the S&P 500 for 3 years, 88.65% for 5 years, and 82.07% for 10 years.

under performing funds though have little to do with under performing those same percentages as investors.

there are thousands of funds with little investor money out there , most are funds few even heard of. many are at the top one year and the bottom the next , but there is that core in the middle that hold most of investors money that do quite well.

when you follow the money you get a very different story.

i would guess and say 80% of investor money is in 20% of the funds . most of those mega funds have done quite well beating their benchmarks over most of the time frames.

all one has to do is follow the money and the odds of beating indexing goes up by a lot .

Fidelity beat benchmarks by $35 billion, but does anyone care? | Reuters

ERD50, you might want to use Vmvix, mid value fund, as the benchmark.

Maybe I just haven't found it but does Vanguard have an auto-rebalance option? Currently invested in the Target Retirement funds right now because all I need to do there is set up auto deposit in time with my paycheck.60/40 full auto AND keep yer dang finger off the trigger! Let those non emotional computers re balance.

Maybe I just haven't found it but does Vanguard have an auto-rebalance option? Currently invested in the Target Retirement funds right now because all I need to do there is set up auto deposit in time with my paycheck.

I haven't seen a way to auto-balance. I'd be curious about this as well. I know I should do it, but I don't think I ever have! I'm primarily in Vanguard index funds, so haven't given it much thought.

That's a straight up 60/40 split though and international allocation.You might want to check out the Vanguard Balanced Index Fund.

I was thinking more along the lines of one where you can set your customized target allocation using Admiral shares or something.Yes, and you are using it. Any of their balanced funds, including Target Retirement, is auto-rebalanced.

From that article's endnotes:

According to the SPIVA Scorecard compiled by S&P Dow Jones Indices, for periods ended December 31, 2014, 76.25% of actively managed U.S. large-cap equity funds underperformed the S&P 500 for 3 years, 88.65% for 5 years, and 82.07% for 10 years.

i would guess and say 80% of investor money is in 20% of the funds . most of those mega funds have done quite well beating their benchmarks over most of the time frames.

all one has to do is follow the money and the odds of beating indexing goes up by a lot .

Vanguard Star VGSTX also rebalances to 60/40. The underlying funds are not strict index funds, though.That's a straight up 60/40 split though and international allocation.

The only Vanguard funds I know of with auto-rebalancing and international allocation are the LifeStrategy and Target Retirement funds.

I was thinking more along the lines of one where you can set your customized target allocation using Admiral shares or something.

... Burton Malkiel presented the evidence of this in A Random Walk Down Wall Street...

...cash allocations were highest at the past market bottoms of 1970, 1974, 1982, 1987, 1990, 1994 (just before the dot-com bubble began), and 2002...

... the opposite for market tops--low cash allocations, when cash allocations should have been high in anticipation of the coming market crashes...

Just curious, does that account for the fees?

I ask because when fees are not subtracted, my Fidelity account (FA-managed) is slightly outperforming my Vanguard account (self-managed, mostly index funds). However, when the 1% Fidelity/FA fee is subtracted, the Vanguard account comes out on top.

Well that wouldn't include FA fees, but it does include mutual fund fees. Mutual fund performance stats are always after fees (expense ratios).

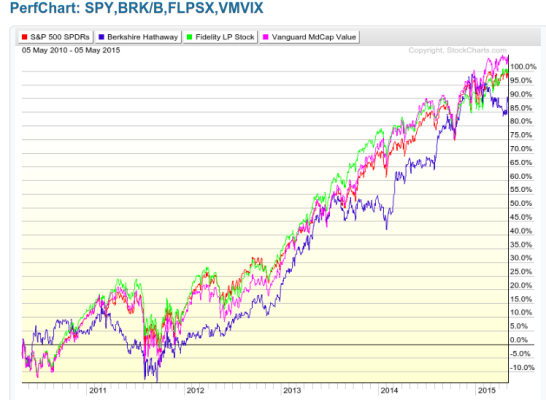

I looked at the Fidelity Low Priced Stock fund he uses as an example in that article. For the most recent 5 years, it has tracked SPY in total return almost exactly. Not sure you can trade on this advice w/o a time machine.

PerfCharts - StockCharts.com - Free Charts

-ERD50

This subject of market timing comes up every so often. People fail to recognize that MF managers' actions are driven by the masses. And so, how can a MF manager act against the masses, who are their clients.

I like to compare this to politics. Politicians are no saint, but we keep forgetting who votes them into office. Where does the root cause lie?