pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

^^^ That is where the eyebonds chart is useful to me because it shows the values at the end of each month by month of issue (and denomination).

Last edited:

I bonds ($10 K each purchase) were purchased on 10/25/2021 and 1/10/2022. What month this year would be the best me to get out of them and take advantage of higher rates elsewhere?

7/1/23 for the first and 10/1/23 for the second. That way, you'll capture the 6.48% rate for the full period.

You can't just look at the current interest rate, you want to have been earning that rate for 3 months since you lose 3 months of interest rate if you sell before 5 years.

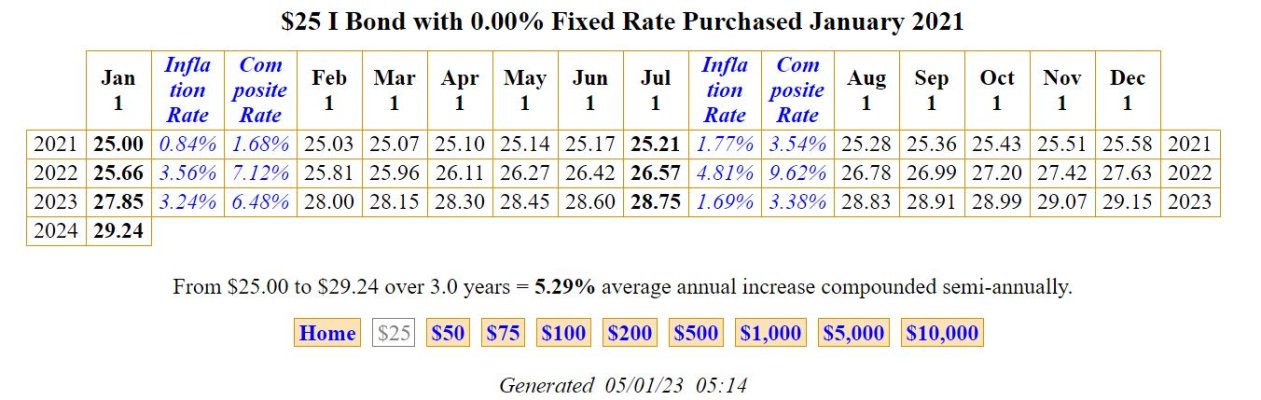

Your Jan 1 2021 purchase changes rate every 6 months from your month of purchase, so it changes in Jan and July. This means you just started earling last May's rate of 3.48, up until June you were earning the earlier November rate.

So if you want to forfeit 3 months at the lower rate, you need to wait till September.

You can't just look at the current interest rate, you want to have been earning that rate for 3 months since you lose 3 months of interest rate if you sell before 5 years.

Your Jan 1 2021 purchase changes rate every 6 months from your month of purchase, so it changes in Jan and July. This means you just started earling last May's rate of 3.48, up until June you were earning the earlier November rate.

So if you want to forfeit 3 months at the lower rate, you need to wait till September.

You will get the same price is you sell at any time in July, conversely you will get the full month interest even if you buy at the end of the month.

Only the month of the date you buy/sell matters, not the actual date during the month.

Since for banks it matters, usually compounded daily, you can get essentially an extra month (like 29 days) I retest by selling I bonds on the 1st and putting it immediately in a HYSA.

Yes.Actually, I think you need to wait until October 1. You would forfeit interest for July, August and September at the 3.38% rate that is effective July 1, 2023 for an I bond issued in Jan 2021.

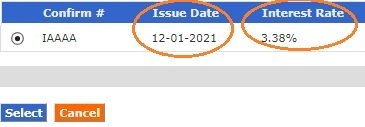

$25 I Bond January 2021

Interest is paid for the month only if you hold on the last day of the month. Interest is paid for the full amount of the first month regardless of the day during the month on which you buy the I-bond.You can sell in September and forfeit July, August and Sept intérêt because Sept is accrued on the first of the month.

No. See my earlier post.Interesting, so selling on the 2nd of the month will still have accrued for the whole month on the 1st (and in this case, could count as 1 of 3 the months forfeited). I realize the money isn't huge but still nice to know for sure how it works.

Exactly correct.Actually, I think you need to wait until October 1. You would forfeit interest for July, August and September at the 3.38% rate that is effective July 1, 2023 for an I bond issued in Jan 2021.

$25 I Bond January 2021

Interest is paid for the month only if you hold on the last day of the month. Interest is paid for the full amount of the first month regardless of the day during the month on which you buy the I-bond.

+1 I'm suprised that the fixed rate is so high. I think I'll probably swap out some 0% fixed rate I-bonds for some 0.9% fixed rate I-bonds in October... I don't mind paying the three-month penalty and locking up the money for a year to get that nice 0.9% fixed rate forever.

Is the penalty deductible on our taxes, as CD interest penalties are?

So if one wants to put the finest point on their early I-bond sale, they could put their issue into eyebonds.info and wait until the value reflected on the Treasury Direct site was beyond the latest blue rate change?Interest is paid for the month only if you hold on the last day of the month. Interest is paid for the full amount of the first month regardless of the day during the month on which you buy the I-bond.

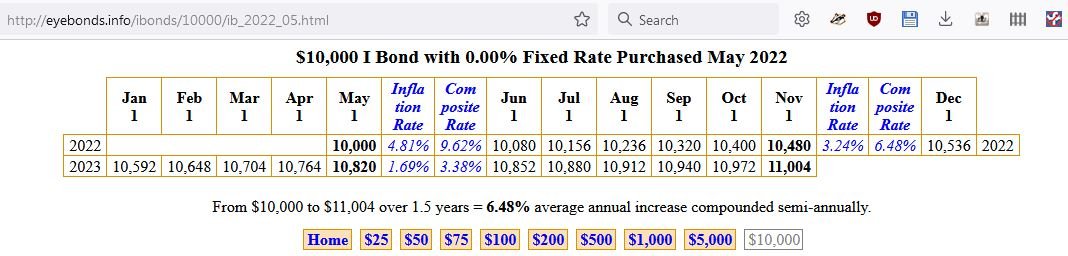

So if one wants to put the finest point on their early I-bond sale, they could put their issue into eyebonds.info and wait until the value reflected on the Treasury Direct site was beyond the latest blue rate change?

Right now, this bond is reading "$10,764" on Treasury Direct, indicating that not all the juice is out of the 6.48% yet. Once it reads "$10,852", you can sell and not leave any 6.48% on the table.

So if one wants to put the finest point on their early I-bond sale, they could put their issue into eyebonds.info and wait until the value reflected on the Treasury Direct site was beyond the latest blue rate change?

Right now, this bond is reading "$10,764" on Treasury Direct, indicating that not all the juice is out of the 6.48% yet. Once it reads "$10,852", you can sell and not leave any 6.48% on the table.

If you sell before 5 years you lose the last 3 months of interest, so you have to go 3 months beyond where it reads "$10,852" in your example.