pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

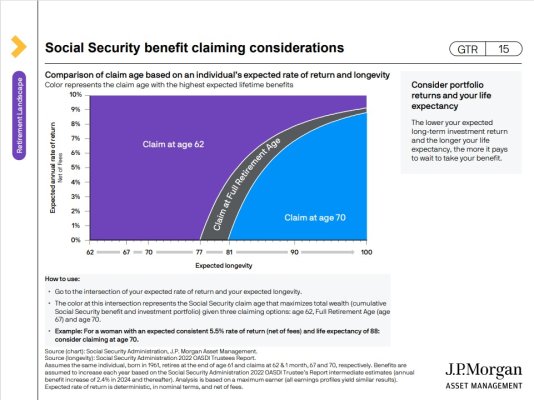

So that really mean half can expect to live shorter and half can expect to live longer? So half never make it to the breakeven point of 82. Just something to consider as one considers when to start SS.

That's a pretty bold and I'd say perhaps invalid statement. While not a forum member, or maybe he was, but Jimmy Buffet was very affluent with a NW of over a BILLION $$$, yet he passed unfortunately at 76.

Other celebrities who passed and had significant bankroll, thereby most being more affluent than those on this forum include Raquel Welch (82), Paul Reubens (71).

I mention the celebrities as they are well known, but personally had friends in the past couple years who passed at 65 (months after retiring), 75 and 77. They each had more substantial bankroll than me. But money may help, but when it's your time, it's your time and money can't stop death. So "average" just means that, there are still a large number of who will fall well short of that golden age.

We can agree to disagree on this, but you can't rely on anecdotal information. From Bard:

Do people with above average income or wealth live longer? If so, how much longer and why?

Yes, people with above average income or wealth do live longer. In the United States, the richest American men live 15 years longer than the poorest men, while the richest American women live 10 years longer than the poorest women. The gaps between the rich and the poor are growing rapidly over time.

There are a number of reasons for this. People with higher incomes have access to better health care, including preventive care and early diagnosis of diseases. They also have more nutritious food, less stress, and more opportunities for physical activity. In addition, they are less likely to smoke or drink alcohol excessively.

A study published in the journal "The Lancet" found that people in the richest countries in the world have an average life expectancy of 82 years, while people in the poorest countries have an average life expectancy of 60 years. This difference is largely due to income inequality.

There are a number of things that can be done to reduce the income inequality gap and improve the health of people at all income levels. These include providing universal health care, improving access to nutritious food, and reducing stress.

Here are some specific ways that income can affect life expectancy:

It is important to note that the relationship between income and life expectancy is not simple. There are many other factors that can affect life expectancy, such as genetics, lifestyle choices, and access to health care. However, income is a significant factor, and it is clear that people with higher incomes tend to live longer.

- Access to health care: People with higher incomes are more likely to have health insurance and to be able to afford to see a doctor when they are sick. This can lead to earlier diagnosis and treatment of diseases, which can improve outcomes and prolong life.

- Nutrition: People with higher incomes are more likely to have access to nutritious food, which is essential for good health. Poor nutrition can lead to a number of health problems, including obesity, heart disease, and cancer, which can shorten life expectancy.

- Stress: People with higher incomes are less likely to experience stress, which is a major risk factor for many diseases. Stress can damage the body's immune system and make it more vulnerable to illness.

- Physical activity: People with higher incomes are more likely to be able to afford to participate in physical activities, which are important for maintaining good health. Physical activity can help to prevent obesity, heart disease, and other chronic diseases.

Last edited: