almost there

Thinks s/he gets paid by the post

- Joined

- Sep 24, 2008

- Messages

- 1,023

Interesting. It was that or another 26-week T-Bill which I already have plenty of, so basically a wash. It will be interesting. Interest rates have not come down as quickly as most people expected.I bought one last year when they were offering a slightly higher rate 5.45% and amazingly it's survived 2 calls and matures next month.

No doubt the bankers are quaking in their boots at the thought that more and more of us are wise to the ways of getting more interest at no additional risk. The poor devils.I don't think a loss of 28 cents will get their attention.")

Funny how the basic 5% savings/passbook account is now considered Magic?

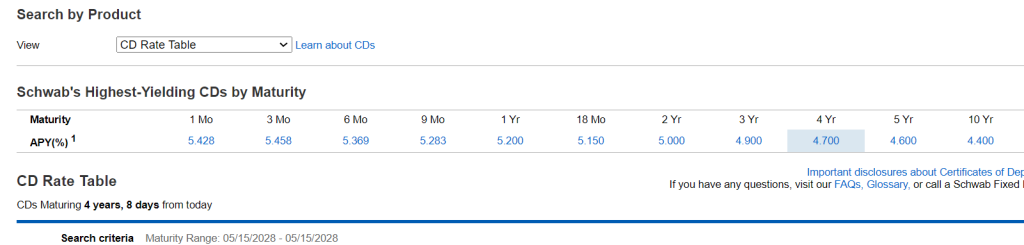

Yesterday moved a bunch from 5.16% MM to cd's. 2yr 5%, 3yr 4.9% 4yr 4.7% and 5 yr 4.6%.

Writing is on the wall.

Am 99.9% sure of it. Normal rates are possibly a thing of the past.

Artificially low rates could be the new normal.

As the average person believes rates are high right now.

Hope I am wrong though. The last couple months were a gift I didn't see coming.

Would not be surprised to see 3% 5 yr CD's in 2025. But who knows.

I guess. My best mortgage rate was 7 1/2%. Got it down from 13 1/2%. Over the years. Then paid it off around 2000.I wouldn't complain. At least mortgages would be cheaper.

Which will simply inflate the price of housing even further. But, that is really off topic and worth a thread of its own.I wouldn't complain. At least mortgages would be cheaper.

This looks like a good deal, especially if rates end up dropping in the near future.Schwab is showing a 3-year, non-callable CD (semi-annual payer) with a 4.9% APY #61768E3S0 Morgan Stanley Private Bank

I just bought a 4.90% non callable for three years at Schwab. In 2027 I am light fixed income as need to fill it a bit to even things out. I may not live beyond 5 years so 2029 is my outside limit.^^^^^

I'm planning on buying another one today. Decisions, decisions.I maybe buy a longer term CD this time.

I'm looking at the same rates/timeframes too. I'm like you, my investment time horizon is no longer measured in many decades. But more like 5 to 10 years, 15 on the outside.I just bought a 4.90% non callable for three years at Schwab. In 2027 I am light fixed income as need to fill it a bit to even things out. I may not live beyond 5 years so 2029 is my outside limit.