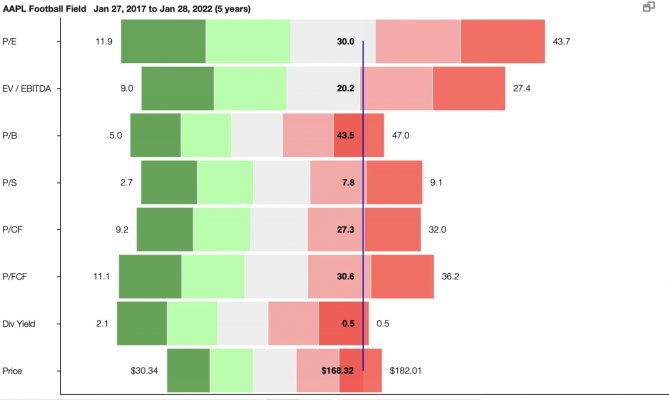

I don't know what to say...closed at almost $134.18 today (536.72, pre-split). It is now a way outsized portion of my portfolio (as far as how much of of one's portfolio should be in one stock). Any rationale part my brain is drowned out by the greedier part, LOL. We haven't even got to the new phone releases coming up...