njhowie

Thinks s/he gets paid by the post

- Joined

- Mar 11, 2012

- Messages

- 3,931

What a move. I was buying 8-10 year duration munis just 6-7 weeks ago in the mid 4% range.

Amazing, isn't it? Will be interesting to see where we are come year end.

What a move. I was buying 8-10 year duration munis just 6-7 weeks ago in the mid 4% range.

Is it somewhat cyclical wrt when in the month it is? If bonds come due on the first and everyone trying to reinvest, maybe wait a few days?

I was getting weekly notices from Fido on new issue munis for my home state and one neighboring state. They were all lousy deals selling at a premium on the offer. NJhowie convinced me to avoid initial offers but I would still look at them except very few are being offered. The last one was a zero coupon offer at a huge premium. No thanks.

How does a zero get priced at a premium? They are discounted at purchase and rise back to par. That’s how they work.

I mis remembered…. You are correct. The discounted initial offer price estimate put the yield at 5% for a 30 year bond. It was all the other munis that were priced at a premium on the initial offer and the yields were 1-2%.

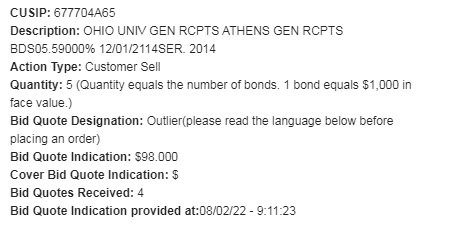

677704A65 - one of the 100 year bonds

bought on 7/8 for 95.204 (plus 0.1 mark up)

sold today for 105.75 (minus 0.1 mark down)

Not bad for 1 month hold.

Were you planning to sell when it hit a target price all along?

Very interesting times in the bond market. Pockets of opportunity and pockets of crap all at the same time.

Fidelity is once again having their $100 bonus offer for opening an account and depositing $50 in it. This is available for new or existing customers who have not previously done the offer.

Last year I was able to do this for DW, but mine was screwed up in the process. I just signed up for it again for myself, and it looks like it will work this time.

Since I now control mom's accounts, I'll do one for her as well.

https://www.fidelity.com/go/starter-pack

Got our $100 in each of the new accounts this morning.

The offer is still ongoing - there is no end date specified on any of the pages or terms and conditions. So it could go on another day, or another few months. It's easy/free money - deposit $50, get $100 - no hoops to jump through.

I have been trying to consolidate, but I'm wondering if this is a good account to open just so I can use their tools to gain info about bonds . . .

A free 200% for almost no effort is worth it. If you get additional benefit, all the better.

As jazz has mentioned a couple times, if you just want to browse around the bond area, you can create a guest account without having a real Fidelity account.

I am waiting to see if I can get 5-10 year muni durations at the same yields as back in June for my taxable account. Right now they are still well below that. I have been picking up lower investment grade corporates over 6% at and around the 5 year mark for my IRA.