People use the same tired arguments about deflation that we've all heard before, but it's not always bad, especially when inflation has been running so high for years:Deflation is not merely going back to lower prices. Deflation is dangerous, especially long term deflation, because it builds up the expectation that prices are going to continue to decrease, therefore people don't spend money and then the economy dramatically slows down. Why buy a car if the prices have been going down for the past 8 months? Just wait another couple of months and they will be even less expensive.

Now project that attitude out across a wide spectrum of goods and services. Pretty soon companies aren't selling very much stuff, profits decline, cash flow withers, so they have to lay off people. Unemployed people don't buy much stuff either. It's a vicious cycle that feeds on itself, paralyzing the economy.

https://www.investopedia.com/articles/markets/111715/can-deflation-be-good.asp

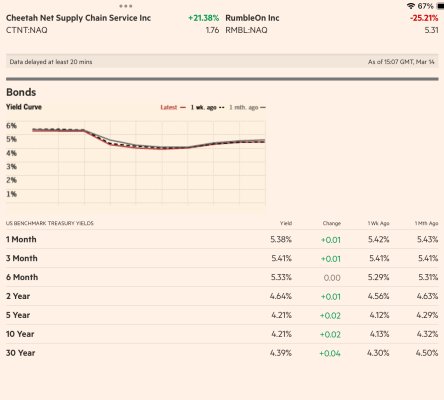

") Is it 1yr, 2yrs or 10yrs....

Is it 1yr, 2yrs or 10yrs....