ERD50

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

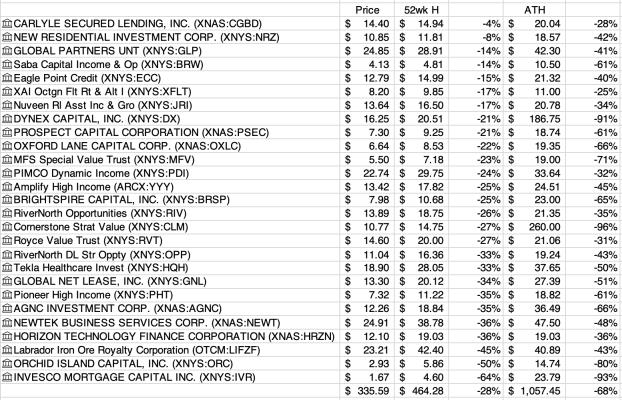

It’s important to not lose sight of the OPs request. Not looking for a “dividends vs no dividends” debate or portfolio market outperformance. OP is looking for a “fairly safe” way to generate dividend income to help cover monthly expenses.

Sorry, my last post crossed with yours.

IMO, it's fair to point out that the 'fairly safe' way of generating income might not be by focusing on div payers at all. I don't think we should ignore that the question itself may be flawed.

I can think of all sorts of cases where someone asks the best way to do a job with xyz, and the correct, informative, helpful, constructive answer is - "Don't -xyz is not the correct tool for that job". Or at least, explain why it's not the best tool, or the reasons why the OP thinks it is a good tool may be flawed.

To ignore that just seem like putting your head in the sand. I'd rather try to help people with the overall problem, not focus on some possibly misguided detail,

-ERD50