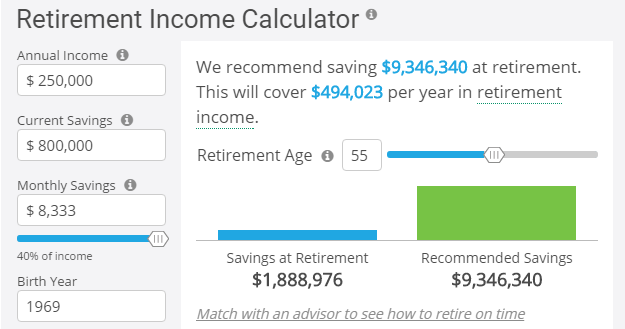

Did anyone try calculator that is on the bottom of the article linked in op? I did not expect much and filled out just for fun but results made me pause for a minute or 2 It said that I need $9,724,502

I suspect that the majority of members in this forum will die with substantial fortunes, in spite of the comments many of us have made about wanting our final check to bounce on our way to the funeral.

I think it's a combination of several things:

1) We enjoy accumulating wealth, and resist seeing it being spent and watching the balance decline after so many years of seeing it grow.

2) We overanalyze the SWR rules in spite of the studies demonstrating that 4% easily survived over many years of stock market booms and busts. We think 3% is the new 4%, and then we reduce the 3% to 2.5% just to be safe.

3) We are so worried about needing end of life care that we are willing to sacrifice enjoying the money today just in case we need extensive care down the road.

4) We have become so accustomed to LBYM that even though we have plenty of money we can't bring ourselves to spend it.

+1

1-3 captures my outlook, the other concern leading me to a low initial withdrawal rate is fear of inflation. Hope to overcome my fear and spend enough to have adventures to fun destinations while we are still young and healthy. Recognize that the things I fear may never materialize, but age will definitely takes its toll.

I suspect that the majority of members in this forum will die with substantial fortunes, in spite of the comments many of us have made about wanting our final check to bounce on our way to the funeral.

I think it's a combination of several things:

1) We enjoy accumulating wealth, and resist seeing it being spent and watching the balance decline after so many years of seeing it grow.

2) We overanalyze the SWR rules in spite of the studies demonstrating that 4% easily survived over many years of stock market booms and busts. We think 3% is the new 4%, and then we reduce the 3% to 2.5% just to be safe.

3) We are so worried about needing end of life care that we are willing to sacrifice enjoying the money today just in case we need extensive care down the road.

4) We have become so accustomed to LBYM that even though we have plenty of money we can't bring ourselves to spend it.

Ready, did you have any idea what you were starting with your post?

I am:

1) Yes

2) Big yes on this one. I started the first year RE spending target (this year) at 100% of prior spending. With modest pension (no SS yet) I was only at 1.5% WR. I have raised the budget to what feels like a posh level, and it is still 1.9% WR. Guess we may try flying business class.

I suspect that the majority of members in this forum will die with substantial fortunes, in spite of the comments many of us have made about wanting our final check to bounce on our way to the funeral.

I think it's a combination of several things:

1) We enjoy accumulating wealth, and resist seeing it being spent and watching the balance decline after so many years of seeing it grow.

2) We overanalyze the SWR rules in spite of the studies demonstrating that 4% easily survived over many years of stock market booms and busts. We think 3% is the new 4%, and then we reduce the 3% to 2.5% just to be safe.

3) We are so worried about needing end of life care that we are willing to sacrifice enjoying the money today just in case we need extensive care down the road.

4) We have become so accustomed to LBYM that even though we have plenty of money we can't bring ourselves to spend it.

I suspect that the majority of members in this forum will die with substantial fortunes, in spite of the comments many of us have made about wanting our final check to bounce on our way to the funeral.

I think it's a combination of several things:

1) We enjoy accumulating wealth, and resist seeing it being spent and watching the balance decline after so many years of seeing it grow.

2) We overanalyze the SWR rules in spite of the studies demonstrating that 4% easily survived over many years of stock market booms and busts. We think 3% is the new 4%, and then we reduce the 3% to 2.5% just to be safe.

3) We are so worried about needing end of life care that we are willing to sacrifice enjoying the money today just in case we need extensive care down the road.

4) We have become so accustomed to LBYM that even though we have plenty of money we can't bring ourselves to spend it.

Like others I agree, but honestly I think your four points can truly be distilled into one: a healthy dose of FEAR for the unknown is the root cause for continued LBYM.

Did anyone try calculator that is on the bottom of the article linked in op? I did not expect much and filled out just for fun but results made me pause for a minute or 2 It said that I need $9,724,502

I'm already retired, so I put in 0s for income and savings, it would not let me put in current age and forced me to add 1 year, result was it assumed about 3% increase in savings and then said I could withdraw 5.2%.

I bet you have a high income so it assumes you need more after retirement.

I'm already retired, so I put in 0s for income and savings, it would not let me put in current age and forced me to add 1 year, result was it assumed about 3% increase in savings and then said I could withdraw 5.2%.

I bet you have a high income so it assumes you need more after retirement.

Yes we have relatively high combined income but numbers still do not make any sense If our income $250k and we save 40% of it - why it is stating that we need $9 mil+ and almost $0.5 mil (!!!) income? Are they trying to scare hell out of me that I would contact their adviser?

1) We enjoy accumulating wealth, and resist seeing it being spent and watching the balance decline after so many years of seeing it grow.

We're trying, but we travel as much as we care to, and splurging at restaurants entails calories we don't need! Trading in a 2 or 5 yo car with 15 or 35k miles just seems...um....dumb? May move to beach but family locations being unknown makes that dubious at this point.

I thought the other day about starting a thread with a similar theme. At 60 we were happy at 2.3% WR. Gradually got it to 3 when 64. At 65 got a $800 a month raise courtesy of Medicare. At 66 we just started on DW SS and me taking based on hers (saving my higher for 70), another 1300 even after they took out for Medicare. So it got me to thinking about how we got here and where we're going at this rate?

Went back and found the Fidelity RIP planner output I did when retired at 60. It showed that now (which yes is worst case) we would have ~2/3 of what we started with using their method. Nope. We now have 1-1/3 of what we had 6 years ago. We take out monthly from the portfolio 3% and every month it just accumulates in our credit union account. Finally returned a BiG chunk just because it seemed dumb not to and we'll be more than able to cover the trips we've got coming from monthly draw coming up. If we HAD done 4% the difference in where we are today wouldn't have been that great, heck, simplistically it'd be about a 6% difference in the total.

I think that you can fixate on these calculators and forget that they generally focus on worst case avoidance. Well guess what? Each year you avoid worst case maybe you should adjust if you care to. Heck, if you can adjust up you can certainly readjust down if need be later when things go south. Or just relax and forget about worrying so much about it. Just learn to enjoy your good fortune...and for God's sake enjoy your good health while ya got it. THAT certainly won't last forever.

As someone said, first world problems. I'm OK with it.

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Joined

Feb 19, 2013

Messages

9,358

There are many homeless people where we live. We will go into the city for a foodie benefit with all you can eat food sampling and wine tasting and then pass by homeless people sleeping in the BART station. Or we will pass by wine bars in the trendy South of Market area packed with millennials with homeless people out on the street outside.

We plan to live pretty well on a low withdrawal rate - nice house, good value cars and go out often. I don't think it is a tragedy to be careful with our money and have a nice sum leftover to leave it to our adult kids, especially since housing is pretty crazy here, and charities that help people who have nothing.

Glad to see the last post mention charity. I turn 54 and retired over 2 months ago. My wife will join me on my ER adventure on Memorial Day weekend when she leaves her job. While we're still figuring out a monthly spending and withdrawal rhythm, we're probably going to come in something around 3%, maybe a bit less. We're traveling more than ever, eating out more, giving more substantially. But we're frugal by nature, and are actively getting rid of physical possessions as we look forward to downsizing to a smaller home in the next couple of years. We just don't need more stuff, no matter our asset levels. We value experiences much more highly.

What I'm hoping is that, once I get in my mid to late 60s (and get ready for SS at age 70), I'll have a much more accurate idea of how we're looking for the rest of our lives. I have no desire to spend every dollar we have, and even less desire to give the bulk of our assets to our kids. What would give me great joy is to establish a foundation or scholarship fund that wouldn't change the world, but might change a few people's lives for the better on an ongoing basis, even after my wife and I have passed.

While I no doubt give more concern about our assets and spending than I need to, focusing on these areas will, in the long run, give us the option of doing something great and lasting with our investments.

I did not expect much and filled out just for fun but results made me pause for a minute or 2

I did not expect much and filled out just for fun but results made me pause for a minute or 2