Why don't we stick to PPACA, healthcare and how to deal with it, and leave that other stuff for another discussion. ")

Why don't we stick to PPACA, healthcare and how to deal with it, and leave that other stuff for another discussion.

You would think so. I assume you have a policy that required medical underwriting, so it seems likely that the risk pool you are in is probably more healthy than the one in the exchange will be. On the other hand, there is no subsidy for your policy, so Anthem may not be able to price it below the subsidized rate.

BTW, Anthem is part of Well Point (WLP).

Thanks FIRE'D. Yes, had to go thru underwriting. Keep in mind that since there will be no underwriting due to automatic acceptance for any of them, the health status of all the pools may change.

Heck, I don't even know if they will have "pools" within the levels. Anyone have any idea how the classifications will work within the levels or is everyone pooled together at the level they apply for?

We don't qualify for a subsidy, have no way to get below that cutoff so it's a non-event for us or perhaps I should say an expensive event.

Just tried this calculator from Covered California..and the rates are significantly lower than the other calculators. So now I'm a bit confused.

http://www.coveredca.com/calculating_the_cost.html

Heck, I don't even know if they will have "pools" within the levels. Anyone have any idea how the classifications will work within the levels or is everyone pooled together at the level they apply for?

How are they getting the health insurance now, are they uninsured, or their current employer will drop health insurance without increase in compensation after Jan 2014?I'm not worried about loosing my health care at the moment. I am worried about the "cost of premiums" for what I consider low to high middle America. I don't see how a couple making $70,000 per household can easily afford an $18,000 net of tax expense on the exchanges if that is their only choice.

...........

The calculators show us on Medicaid under that scenario. That is pretty odd there is no asset test...........

So if we sell our house and live off the proceeds for a number of years, and we either stop our business income or what we earn gets dispersed between business expenses and retirement contributions, then our taxable income might be pretty low in future years.

The calculators show us on Medicaid under that scenario. That is pretty odd there is no asset test.

What is it like to be on Medicaid? Is that something most doctors and hospitals accept? Is it Medicaid or no subsidy at all for us if our taxable income is low enough?

Section 62(a) is the IRS regulation describing the "above the line" deductions that are calculated before AGI is figured, i.e. those seen on the first page of form 1040. The full list is found here:Internal Revenue Code, §36B(d)(2),

‘‘(d) TERMS RELATING TO INCOME AND FAMILIES.—For purposes

of this section—

‘‘(2) HOUSEHOLD INCOME.—

‘‘(B) MODIFIED GROSS INCOME.—The term ‘modified

gross income’ means gross income—

‘‘(i) decreased by the amount of any deduction

allowable under paragraph (1), (3), (4), or (10) of section

62(a),

‘‘(ii) increased by the amount of interest received

or accrued during the taxable year which is exempt

from tax imposed by this chapter, and

‘‘(iii) determined without regard to sections 911,

931, and 933.

How are they getting the health insurance now, are they uninsured, or their current employer will drop health insurance without increase in compensation after Jan 2014?

The rules require issuers to treat all of their non-grandfathered business in the individual market and the small group market, respectively, as a single risk pool.

PHS Act section 2701 only allows non-grandfathered health insurance issuers in the individual and small group markets to vary premiums based on the following factors beginning in 2014: (1) whether the plan or coverage applies to an individual or family; (2) geographic rating area; (3) age, limited to a variation of 3:1 for adults; and (4) tobacco use, limited to a variation of 1.5:1.

PHS Act section 2701 only allows non-grandfathered health insurance issuers in the individual and small group markets to vary premiums based on the following factors beginning in 2014: (1) whether the plan or coverage applies to an individual or family; (2) geographic rating area; (3) age, limited to a variation of 3:1 for adults; and (4) tobacco use, limited to a variation of 1.5:1.

can anyone explain the no. 3 and 4 scenarios as how they would apply to premiums? sorry if I am in this is the wrong place for this question.

Age and Smoker Factors

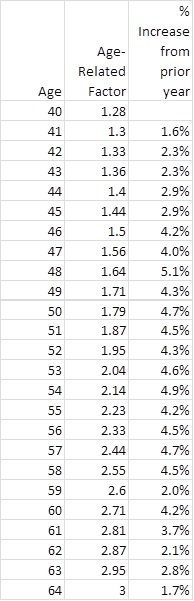

Exhibit 12

Age Age Related Smoker

20 0.64 1.00

21 1.00 1.20

22 1.00 1.20

23 1.00 1.20

24 1.00 1.20

25 1.00 1.20

26 1.02 1.20

27 1.05 1.20

28 1.09 1.20

29 1.12 1.20

30 1.14 1.20

31 1.16 1.20

32 1.18 1.20

33 1.20 1.20

34 1.21 1.20

35 1.22 1.20

36 1.23 1.20

37 1.24 1.20

38 1.25 1.20

39 1.26 1.20

40 1.28 1.20

41 1.30 1.20

42 1.33 1.20

43 1.36 1.20

44 1.40 1.20

45 1.44 1.20

46 1.50 1.20

47 1.56 1.20

48 1.64 1.20

49 1.71 1.20

50 1.79 1.20

51 1.87 1.20

52 1.95 1.20

53 2.04 1.20

54 2.14 1.20

55 2.23 1.20

56 2.33 1.20

57 2.44 1.20

58 2.55 1.20

59 2.60 1.20

60 2.71 1.20

61 2.81 1.20

62 2.87 1.20

63 2.95 1.20

64+ 3.00 1.20

We currently are on my wifes group plan from her former job but pay the full premium, $1200 a month. Would we still be able to purchase on the exchanges?

I see on the calculators that they ask if you have insurance thru work.

More here: http://www.dol.gov/ebsa/newsroom/tr13-02.html[FONT="]There may be other coverage options for you and your family. When key parts of the health care law take effect, you’ll be able to buy coverage through the Health Insurance Marketplace. In the Marketplace, you could be eligible for a new kind of tax credit that lowers your monthly premiums right away, and you can see what your premium, deductibles, and out-of-pocket costs will be before you make a decision to enroll. Being eligible for COBRA does not limit your eligibility for coverage for a tax credit through the Marketplace. [/FONT]

In Michigan there is definitely an assets test. I'd check further for you state.

We are not on cobra. Just allowed to stay on the group plan as long as we pay the full amount of the policy.

Careful on that assumption of business expenses, DLDS. The Modified Adjusted Gross Income calculation may trip you up.

This article may be helpful in your situation. It describes what a grandfathered plans is, and why it may be an apples-to-oranges comparison to an exchange policy.

Should you skip Obamacare and keep your old plan? | Reuters

Not quite apples to apples, but increase in price by nearly half for something close. Not "affordable" for everyone, but if you can get the subsidy, that pain can be avoided. I just don't envy the guys that get their grandfathered plans closed-out and so are forced into the marketplace and also have MAGI above 400% FPL. Sad day for those guys.Despite the enchancements, plenty of people will look at the new benefits under PPACA and think, "Thanks, but no thanks." Their current policy, grandfathered in, may satisfy their needs and include their doctors in its networks — at a manageable price.

Indeed, many will find it's cheaper to keep their current coverage. Looking at plans in effect today, the online insurance broker eHealthInsurance found that premiums were 47 percent higher and deductibles were 27 percent lower than for individual plans that will incorporate all of PPACA's new rules.

Carrie McLean, consumer health insurance specialist for eHealthInsurance, notes it is not a direct apples-to-apples comparison because many existing plans don't meet basic requirements that all plans will follow as of next January. Also, members who buy coverage through health exchanges may qualify for government subsidies to ease costs.

Nonetheless, average monthly premiums for individuals in plans without the newly required benefits — the closest equivalent to grandfathered plans — were $190 versus $279. Average deductibles for individuals were $2,257 versus $3,079.

Does anybody know what the reporter means by enrollment "running through" March 2014? Then what?As Obamacare’s main provision requiring all U.S. citizens to have health insurance takes effect Jan. 1, enrollment via exchanges is scheduled to start in October and run through March.

I am trying to plan against an uncertain work / ER schedule in 2014 and beyond. I may or may not need to purchase insurance through my state exchange in 2014.

This line in an otherwise unremarkable article caught my eye.

Obama set to kick off enrollment blitz amid jitters over health plan - Health Exchange - MarketWatch

Does anybody know what the reporter means by enrollment "running through" March 2014? Then what?

Is the plan for the exchanges to have an annual enrollment period similar to employer plans, or Medicare? If so, what will be the qualifying events that allow one to sign up for an exchange policy outside that period?