Are most of the people on this thread including their home as part of their Net Worth? Some have explicitly included it.

OP here. Real estate equity is not included in the $3M for me

Are most of the people on this thread including their home as part of their Net Worth? Some have explicitly included it.

OP here. Real estate equity is not included in the $3M for me

Funny thing though, even though we're in La-La-Land, comparatively, I do find I'm still easily annoyed by some trivial expenses. For instance, I have a '67 Pontiac Catalina that's about to go in the shop for its annual checkover. It only gets driven maybe 800-1000 miles per year, and its belts and hoses look good, but I don't trust them, as they're getting up in age. Well, that kind of stuff isn't so easy to track down anymore, so the mechanic said if I ordered the parts, he'd put them on. Well, just between an upper and lower radiator hoses, a spring that goes in the lower to keep it from collapsing (apparently a common thing with older cars), an alternator belt and a power steering belt (a/c doesn't work, so no need for that belt), I was looking at something like $110!

Are simple maintenance parts really that pricey these days for most cars?! I realize the typical modern car uses one serpentine belt for everything, so naturally that's going to be pricier. But still...maybe it's longer ago than I think, but I swear I can remember when all those parts combined would've only been like $20-30!

Also, I guess being low volume parts these days, that probably raises production costs. After all, Pontiac quit building its own V8s since part way through the 1981 model year!

Still, I think it's odd that I can lose $10K when the stock market goes just slightly south, yet I'm quibbling over $110 in car parts!

I'll admit that sometimes I'm in the grocery store, and something I don't normally buy might catch my eye. My first impulse might be "I can't afford it" or "that's too expensive." But sometimes I'll catch myself and be like "Okay now, that extra $1.85 isn't going to bankrupt you!"

")

Even though we live in la la land, the old LBYM habit dies hard and still rears its head now and then

Even now DW still bugs me to use a coupon when I go to Del Taco to buy a combo meal. The coupon might give me free side fries, a medium drink or a $1 off purchase price. It takes me 3 minutes to dig up the coupon, pick the one I want and get a pair of scissors to cut it out---all just to save a buck. Yet we think nothing of spending $25k to take the kids to Japan for a 2-week trip next month. So the clipping coupon thing is rather silly in the grand scheme of things.

I think the market losses are a little different though. None of us have any control over market performance from day to day, so we just mentally accept market ups and downs as par for the course.

Even though we live in la la land, the old LBYM habit dies hard and still rears its head now and then

Even now DW still bugs me to use a coupon when I go to Del Taco to buy a combo meal. The coupon might give me free side fries, a medium drink or a $1 off purchase price. It takes me 3 minutes to dig up the coupon, pick the one I want and get a pair of scissors to cut it out---all just to save a buck. Yet we think nothing of spending $25k to take the kids to Japan for a 2-week trip next month. So the clipping coupon thing is rather silly in the grand scheme of things.

I think the market losses are a little different though. None of us have any control over market performance from day to day, so we just mentally accept market ups and downs as par for the course.

Ohhh yeah!! I see our frugal ways just like yours. A very hard habit to break. LolEven though we live in la la land, the old LBYM habit dies hard and still rears its head now and then

Even now DW still bugs me to use a coupon when I go to Del Taco to buy a combo meal. The coupon might give me free side fries, a medium drink or a $1 off purchase price. It takes me 3 minutes to dig up the coupon, pick the one I want and get a pair of scissors to cut it out---all just to save a buck. Yet we think nothing of spending $25k to take the kids to Japan for a 2-week trip next month. So the clipping coupon thing is rather silly in the grand scheme of things.

I think the market losses are a little different though. None of us have any control over market performance from day to day, so we just mentally accept market ups and downs as par for the course.

Almost all of us LBYM, I started because my parents lived like that. But the difference is with a lower-middle class income and four kids they had to live like that to survive. I don't have to but I still live LBYM because it's actually more fun, mentally stimulating and challenging to live like that. It's still a thrill to get a good deal. Don't let having money take that away from you.

Curious about this thread. Curious when you hit:

1M

2M

3M

Are most of the people on this thread including their home as part of their Net Worth? Some have explicitly included it.

Absolutely i include my house and mortgage in my NW calculation. NW is a mostly cut and dry calculation. But I don’t assume my house produces/raises any cash in my retirement cash flow analysis. Which could happen if one were to sell, rent, or utilize a HELOC or reverse mortgage as examples.

Congrats. I remain confused why people exclude real estate from net worth. If I’m a renter with a million in the stock market I have a million dollar net worth. If I exchange that money from stocks to a house, did my net worth really just drop to zero?

Climbing the M's is ok as long as I don't have to work for it or cut spending. I'm not going to refrain from some BTD's just to pass another M. More money becomes less important as I get older - passing another M is not something I track or yearn for. It's all about health and happiness at this point.

Congrats. I remain confused why people exclude real estate from net worth. If I’m a renter with a million in the stock market I have a million dollar net worth. If I exchange that money from stocks to a house, did my net worth really just drop to zero?

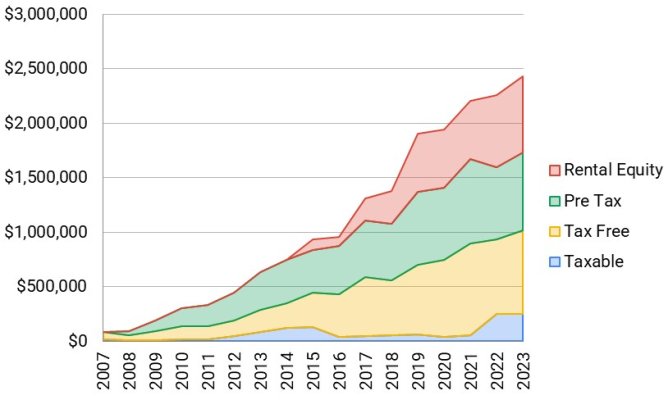

This is our net worth evolution since we both started working in 2007 after graduate school. DW retired in 2013 with the arrival of our third kid. First rental purchased in 2015 and started renting it in 2016.

Second rental purchased at the end of 2016, third at the beginning of 2017. Fourth rental purchased in 2018 and fifth in 2019.

You have done well for not that many years in the work force. Great job!!!!

I don't have anywhere near $3M, even including my house and contents, and car.

Yes, the number certainly doesn't matter as much as how that number relates to your expenses. Many people have super long happy retirements with much less.

Those were definitely NOT the best years of my life, Mom!! Yes, the number certainly doesn't matter as much as how that number relates to your expenses. Many people have super long happy retirements with much less.

This is our net worth evolution since we both started working in 2007 after graduate school. DW retired in 2013 with the arrival of our third kid. First rental purchased in 2015 and started renting it in 2016.

Second rental purchased at the end of 2016, third at the beginning of 2017. Fourth rental purchased in 2018 and fifth in 2019.